While it has been recently scaled back to about US$1.7 trillion from the US$2 trillion originally proposed, “The American Jobs Plan” is an ambitious and sweeping piece of legislation, which aims to not only repair and revamp the nation’s ailing infrastructure, but also to fight climate change and racial injustice, create quality jobs, boost the nation’s housing stock, widen broadband access, and even improve care for the elderly and disabled.

While the United States is one of the wealthiest countries in the world, its infrastructure is poor. The American Society of Civil Engineers gives US infrastructure a grade of C-, and notes that there is a water main break every two minutes, 43% of public roads are in poor or mediocre condition and 42% of bridges are more than 50 years old.1 Even our nation’s airports, schools and wastewater treatment plants rank only a D+, while public transit receives a barely passing D- grade.2 It’s clear that infrastructure upgrades are long overdue.

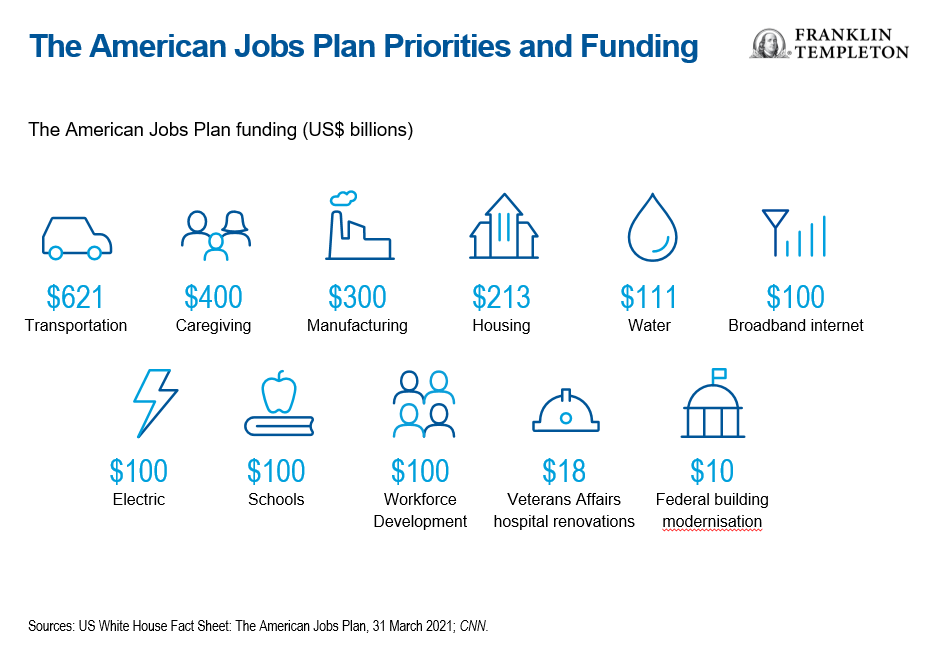

Plan Priorities and Funding

Biden’s Plan includes a broad array of initiatives, with the following goals3:

- Fix highways, rebuild bridges, upgrade ports, airports and transit systems.

- Build, preserve, and retrofit more than two million homes and commercial buildings, modernise our nation’s schools and child care facilities, and upgrade veterans’ hospitals and federal buildings.

- Deliver clean drinking water, a renewed electric grid, and high-speed broadband to all Americans.

- Solidify the infrastructure of our care economy by creating jobs and raising wages and benefits for essential home care workers.

- Revitalise manufacturing, secure US supply chains, invest in research and development (R&D), and train Americans for the jobs of the future.

- Create good-quality jobs that pay prevailing wages in safe and healthy workplaces, while ensuring workers have a free and fair choice to organise, join a union, and bargain collectively with their employers.

Funding includes: US$621 billion for transportation, US$400 billion for caregiving, US$300 billion for manufacturing, US$213 billion for housing, US$111 billion for water, US$100 billion for broadband internet, US$100 billion for electric, US$100 billion for schools, US$100 billion for workforce development, US$18 billion for Veterans Affairs hospital renovations, and $10 billion for federal building modernisation.

A Taxing Issue

Of course, someone has to pay for all these efforts. The ‘Made in America Tax Plan’ overhauls the tax system to help fund these initiatives, proposing to ‘fix the corporate tax code so that it incentivises job creation and investment’ in the United States, stops ‘unfair and wasteful profit shifting to tax havens’, and ‘ensures that large corporations are paying their fair share’.4 Here’s an outline of the plan:

1. Corporate tax hike: Biden would raise the corporate income tax rate to 28%, up from 21%. The rate had been as high as 35% before former President Donald Trump and congressional Republicans cut taxes in 2017.

2. Global minimum tax: The proposal would increase the minimum tax on US corporations to 21% and calculate it on a country-by-country basis to deter companies from sheltering profits in international tax havens.

3. Tax on book income: The president would levy a 15% minimum tax on the income the largest corporations report to investors, known as book income, as opposed to the income reported to the Internal Revenue Service.

4. Corporate inversions: Biden would make it harder for US companies to acquire or merge with a foreign business to avoid paying US taxes by claiming to be a foreign company. And, he wants to encourage other countries to adopt strong minimum taxes on corporations, including by denying certain deductions to foreign companies based in countries without such a tax.

5. Reduce foreign country loopholes:

- President Biden is proposing to encourage other countries to adopt strong minimum taxes on corporations, just like the United States, so that foreign corporations aren’t advantaged and foreign countries can’t try to get a competitive edge by serving as tax havens.

- As noted, Biden is proposing to make it harder for US corporations to acquire or merge with a foreign company to avoid US taxes by claiming to be a foreign company.

- Biden is proposing to provide a tax credit to support onshoring jobs as well as to eliminate a loophole for intellectual property that encourages offshoring jobs and investing in effective R&D incentives.

The question is whether Democrats can actually get these plans through Congress. If they can’t get 10 Republican senators on board, they will have to try to pass to the infrastructure bill through budget reconciliation, which would not require any Republicans to back the plan in a chamber split 50-50 by party.

Coming off the US$1.9 trillion pandemic stimulus bill, spending hawks have raised concerns. Tax increases could send companies overseas, and the administration’s economists have expressed concern that a gap between spending and revenue would widen the federal deficit by such a large degree that it could risk triggering a spike in interest rates, which could in turn cause federal debt payments to skyrocket. There could also be a repeal of the cap on state and local tax deductions.

Outside of funding, the Plan aims to:

Empower Workers: Call on Congress to ensure all workers have a free and fair choice to join a union by passing the Protecting the Right to Organise (PRO) Act, and guarantee union and bargaining rights for public service workers.

Create good jobs: Tie federal funding to jobs with strong labour protections so federal investments support good jobs and pathways to the middle class.

Protect workers: Call for increased penalties when employers violate workplace safety and health rules.

What Does This Mean for the Muni Market?

We expect that the muni market will play a role in implementation of these infrastructure programmes if passed. State and local governments or agencies finance about 78% of infrastructure in the United States, according to an October 2018 report by the Congressional Budget Office. As a result, we expect that much of the federal aid could filter through the muni bond market. This could increase the supply of tax exempt and/or taxable debt.

Direct pay bonds are also currently being considered as a course of finance. Build America Bonds, an example of direct pay bonds used during President Barack Obama’s era, were deemed to be a success, and many are open to the possibility that they could play a role again in future infrastructure initiatives. Others believe this to be a disguised state bailout for areas already flush with cash from the recent stimulus funds. That said, no formal decisions have been made.

Matching an increase in supply could be an increase in demand for muni bonds from investors. With tax increases on Biden’s radar screen, tax-exempt muni bonds could become a more popular option for investors trying to manage their tax liability.

Finally, infrastructure projects are often considered jobs bills given the number of people required to build the infrastructure. This means more money going into state and local governments through tax revenues and potential for economic growth. Coming on the heels of other federal stimulus aid, we remain bullish on municipal credit and market fundamentals.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Because municipal bonds are sensitive to interest rate movements, a municipal bond portfolio’s yield and value will fluctuate with market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the portfolio’s value may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

______________________

1. Source: American Civil Engineers, “2021 Report Card for America’s Infrastructure.”

2. Ibid.

3. Source: WhiteHouse.gov

4. Ibid.