Key takeaways:

- We knew that California would announce a budget deficit.

- California’s credit ratings incorporate the tax volatility it faces, so as long as the state employs a diverse approach to addressing any deficits, we don’t expect any ratings actions at this time.

- A slowdown in US economic activity is likely to impact most states and some could see budget deficits as costs rise at the same time.

- States and many muni credits go into this period of slower or negative growth with very strong balance sheets and reserve funds.

For those who watch state budgets closely, January marks the official beginning of “budget season” with California Governor Gavin Newsom’s release of his preliminary budget for fiscal year 2024 (FY24). With the sheer size of California’s budget and its highly volatile tax revenue structure, among other things, the California budget release gives us a peek into some of the challenges or opportunities that the larger US states will have as we move closer to June 2023 budget adoptions.

It was no surprise that Newsom announced a budget deficit. First, the state has been reporting monthly underperformance of revenues since the summer. Second, the state is highly dependent on capital gains and personal income tax revenue, which are weakening due to stock market weakness and wage growth slowing. And finally, the state had been seeing unprecedented revenue growth post-pandemic and we know that this would not continue indefinitely, especially given the Federal Reserve’s increases in interest rates and inflationary pressures.

The questions for muni credit experts included:

- What is driving the volatility?

- Will the announcement of California’s budget deficit lead to a downgrade?

- Could this deficit announcement result in drawn out budget battles that hurt credit?

- Can the deficit be eliminated?

- Is this a trend that we are likely to see in other states?

Let’s take each of these questions.

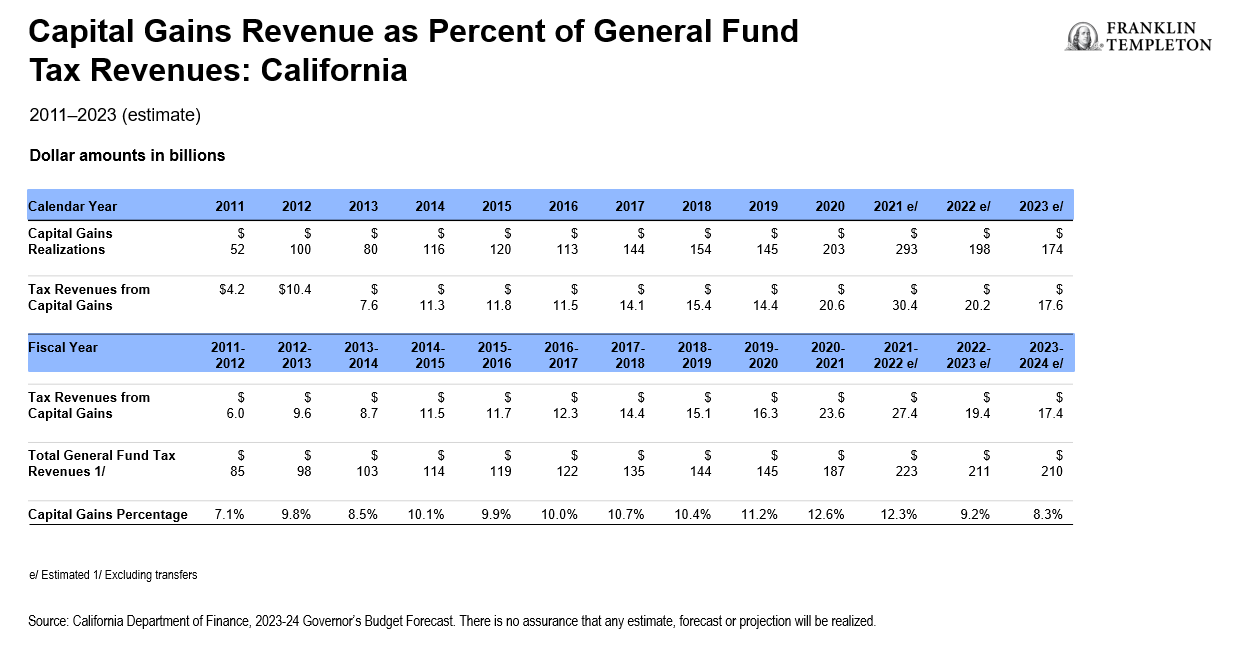

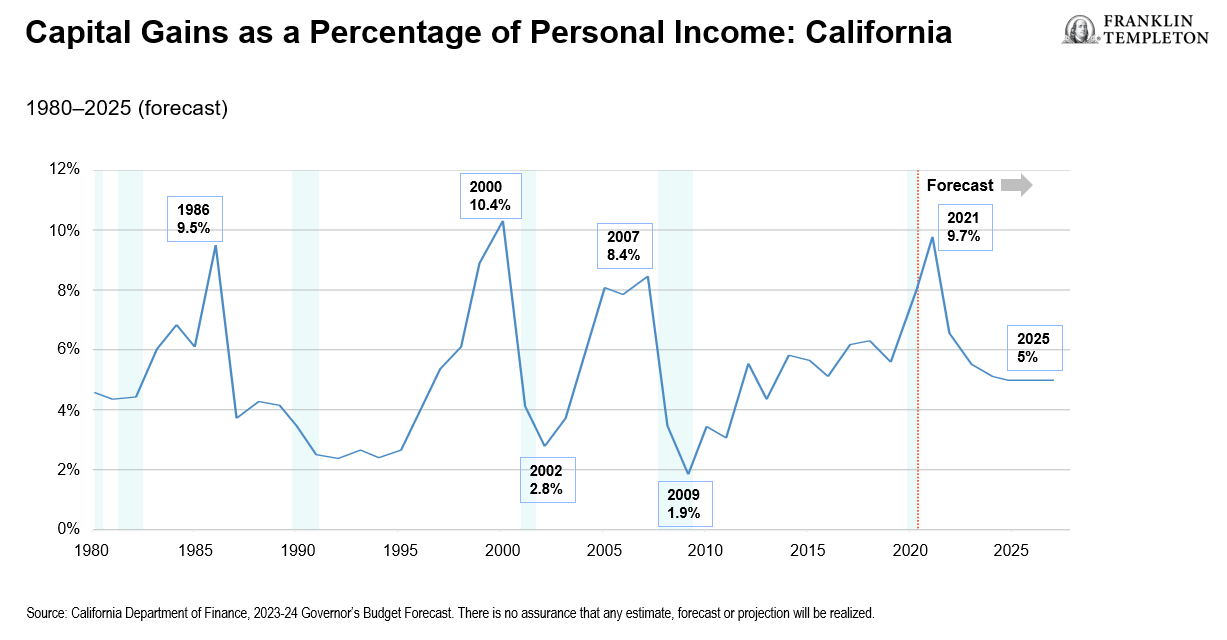

- What is driving the volatility? The state’s general fund is highly reliant on income taxes and in particular, capital gains taxes. The state also has a number of taxes levied on higher income people who tend to have more volatile incomes. So, when investment markets perform well, the state tends to see sharp increases in tax revenue. But when investment markets perform poorly, we see declines, like in 2022. The two charts below illustrate the volatility of capital gains taxes.1

- Will the announcement of California’s budget deficit lead to a downgrade? At this point, our answer is no. First, this is a very early look into the governor’s projections and priorities; there are still four months until the next budget release and five months until adoption deadlines. Second, the state has very high levels of reserves and many tools in its toolbelt to close this budget gap. And three, we feel that so long as the state bases the budget on realistic assumptions and closes the deficit in an appropriate way, the rating is likely stable for now.

- Could this deficit announcement result in a drawn-out budget battle that hurts credit? While various members of the government will have their own estimates and priorities, we expect that the fact that the same party leads both the executive and legislative branches of government will enable a smooth path. Major priorities are likely to be similar, it is just the details that will need to be agreed upon. Second, the state enters this challenge with very robust reserves and many tools in its budget- deficit toolbelt. And third, there is ample time for the governor and legislature to look at potential solutions and get others on board.

- Can the deficit be eliminated? The short answer is yes, and a balanced budget is a requirement. The state has less power over technology sector layoffs and economic underpinnings, but as mentioned above, reserves are large and there are lots of tools to address the deficit. Over the next few months as the economic picture becomes a bit more clear, the governor will be socializing his ideas among legislators and other stakeholders. There are tough decisions ahead for the governor and legislature, but the tools available should make the question not “if” but “how.”

- Is this a trend we are likely to see in other states? Only a few states have released their preliminary budgets at this point, but we think that California will be more of an outlier this year rather than part of a trend. California’s budget is highly reliant on income taxes, and capital gains taxes in particular. This makes revenues very volatile, and we can see large shifts depending on how financial markets (i.e., capital gains) perform. This isn’t a surprise and the fact that the state’s revenue stream is so volatile (both to the positive and negative) is factored into the state’s rating. It’s one of the key reasons that we think the state should have higher reserves than others. If economic conditions weaken and remain weak, we could see other states reveal deficits, but that remains to be seen.

In summary, California definitely has its challenges, but we think it has the tools to deal with them in a way that should not impact its credit rating this year. Ongoing economic weakness could certainly make next year far more difficult.

Which state is next? New York State has the first fiscal year end (March 31) so we will soon have additional insight into their budget. New York City has released its $102.7 billion FY24 preliminary budget which projects increased revenue assumptions of $1.7 billion for FY23 and another $738 million for FY24, but year-over-year revenues are expected to decline by $3.7 billion or -3.5%, which brings a year-over-year revenue change that is flat.

Michigan, which has a September 30 fiscal year, updated FY22 revenue assumptions by +$1.5 billion due to outperformance of sales and income taxes. While FY23 revenues are expected to be lower than FY22, estimates have been revised higher.

All eyes are on Illinois, which should release its FY24 budget in a few weeks. A November mid-year update estimated that the current fiscal year could see a new positive surplus of $1.689 billion. Tax revenues are expected to grow $3.7 billion, about $1.3 billion of which would be used to make an additional transfer to the Rainy Day Fund.

We will be watching these developments closely and are optimistic most states can weather changing economic conditions. We have an extensive research team which highlights our ability to be nimble and can pivot quickly if we uncover any cause for concern.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Because municipal bonds are sensitive to interest rate movements, a municipal bond portfolio’s yield and value will fluctuate with market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the portfolio’s value may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

__________________

1. Source: Governor’s Budget Summary, State of California, 2023-2024.