“It seems to be common sense that if you are going to search for these unusually good bargains, you wouldn’t just search the United States … why not search everywhere? That’s what we’ve been doing for forty years. We search anywhere in the world.” Sir John Templeton, 1979

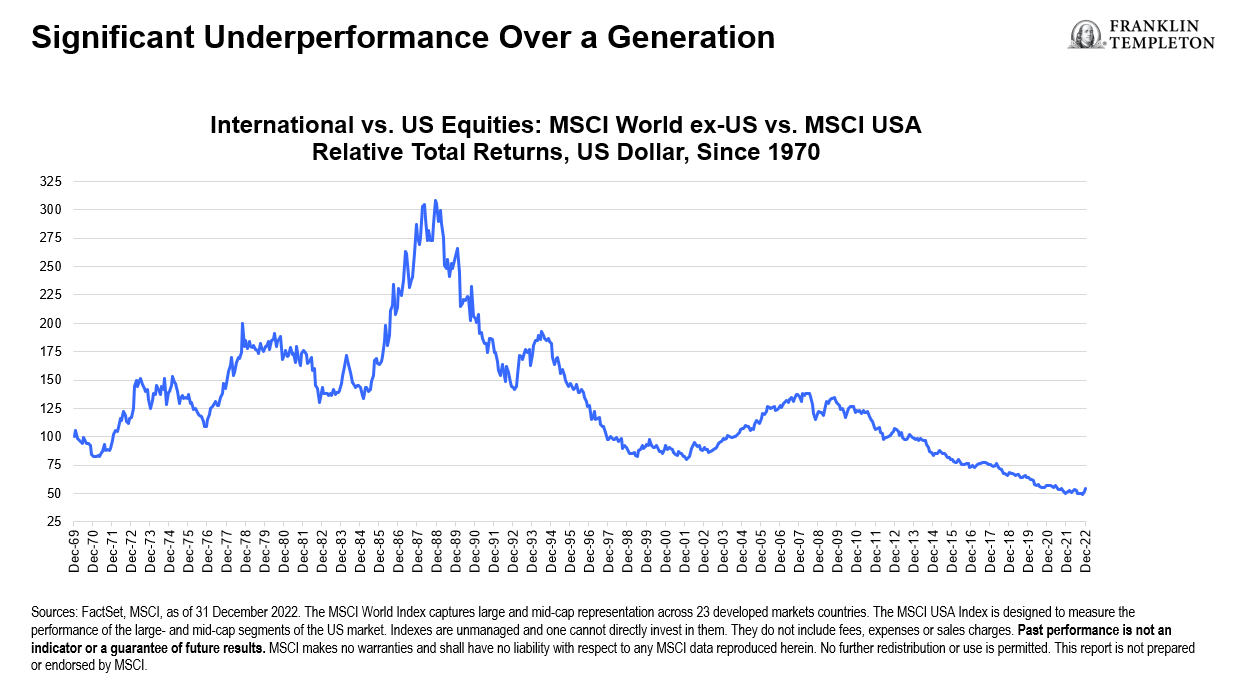

The post-global financial crisis (GFC) dominance of US equities has been completely unprecedented.

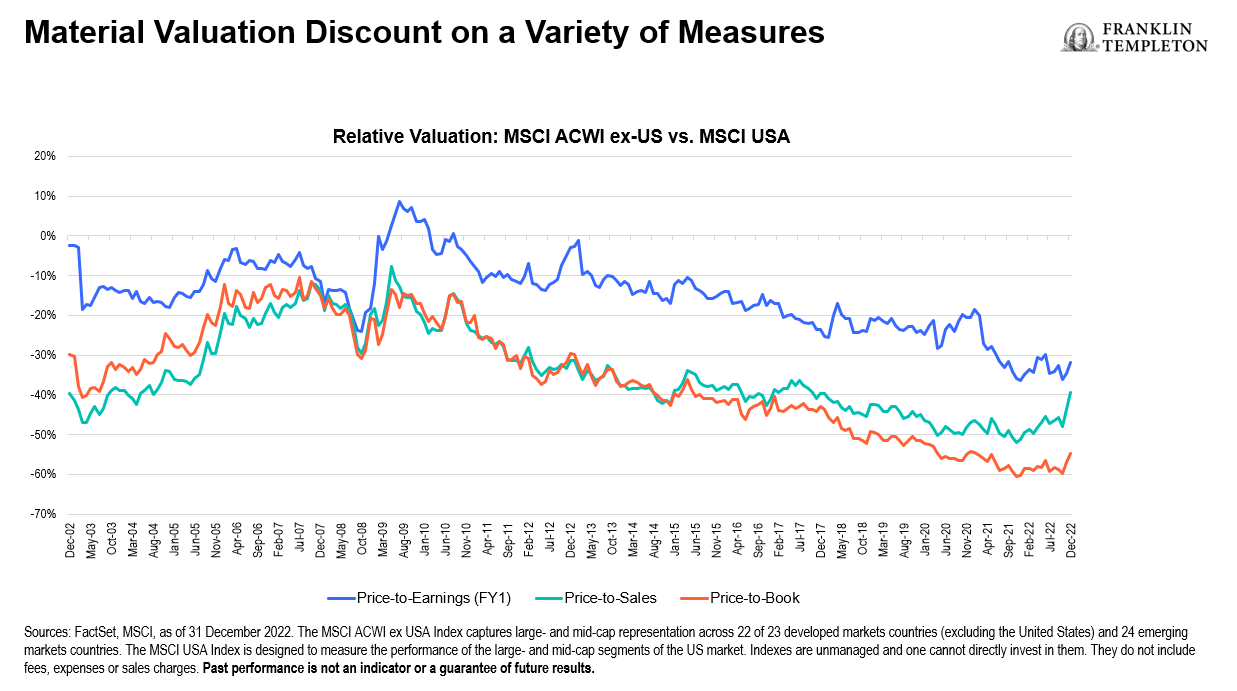

Across numerous valuation metrics, international equities are near the cheapest relative to US equities they have been in roughly two decades.

There are many reasons why US equities have so dramatically outperformed, but the core explanation has to do with monetary policy. In response to the GFC—and then to the European sovereign debt crisis in 2011, the “taper tantrum” in 2013, “Volmageddon” in 2018, and the COVID-19 crisis in 2020 (to name a few recent episodes)—central bankers flooded the financial system with liquidity by pinning down interest rates and entering bond markets with the equivalent of a blank check.

Globally, debt has soared by over US$100 trillion since the GFC. The US Federal Reserve (Fed) led the way in both size and timing, and the subsequent liquidity wave disproportionately buoyed US markets. Growth-oriented businesses in consumer and technology industries that comprise much of the US market capitalization were the main beneficiaries.

But that was then. Today, we are experiencing the exact opposite of the conditions that formerly supported US growth stocks. Interest rates are rising to contain generationally high inflation that the years of aforementioned easy money had sparked. Western central banks have gone from providing liquidity to withdrawing liquidity. Economic growth is slowing as COVID-era stimulus programs roll off and companies and consumers alike contend with materially higher costs of capital. And asset bubbles everywhere—from cryptocurrencies to real estate to profitless tech companies—are quickly deflating.

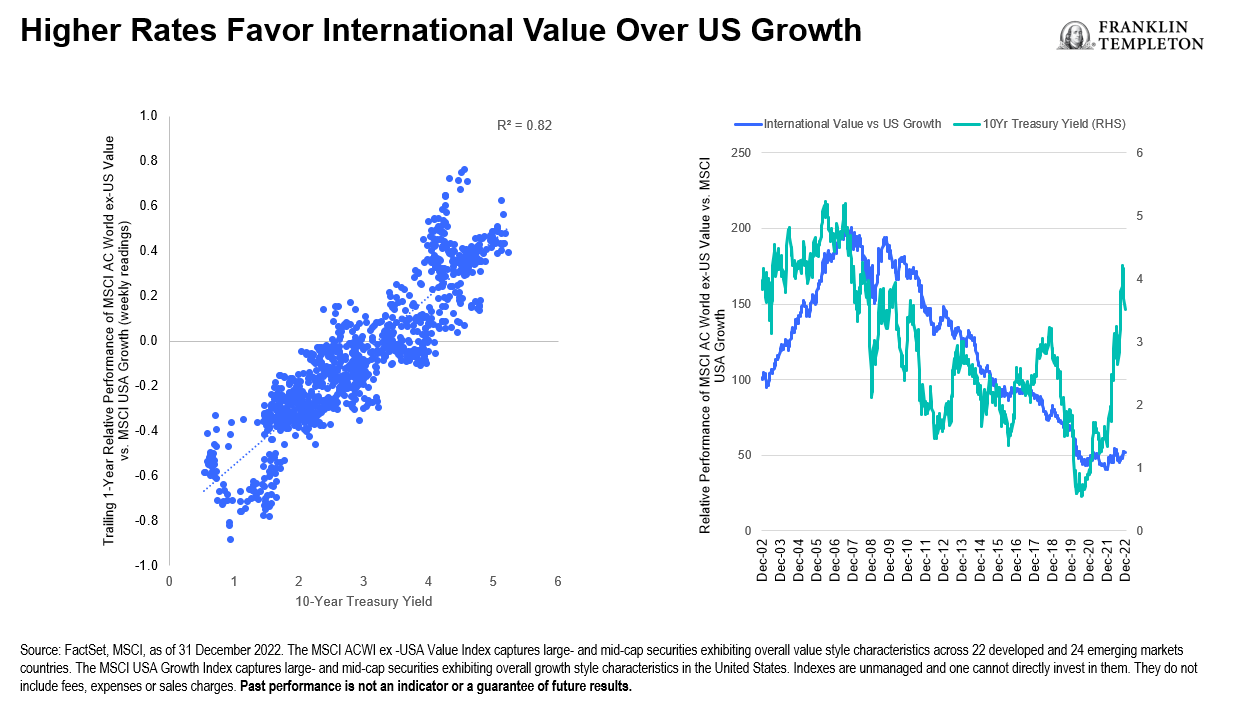

Fed Chair Jerome Powell has prioritized inflation containment as the central bank’s top policy priority, and at a November 2022 press conference, indicated that the Fed still has “some ways to go” to fight inflation. While the pace of interest rate hikes looks to taper off in the quarters to come, Powell’s messaging suggests that rates will remain elevated and policy restrictive for the foreseeable future. As Exhibit 3 shows, this creates an environment that significantly favors international value strategies over the US growth strategies that led the last cycle. That’s not only because of the way that different discount rates impact the valuation of future cash flows (low rates ascribe more value to the longer-dated cash flows associated with growth stocks, while high rates put a premium on the present-day cash flows associated with value stocks). It’s also because higher interest rates make fundamentals more important.

Increasingly, there will no longer be a free lunch for companies that can’t earn above their cost of capital or service their debt at higher interest rates. The unfashionable discipline of fundamental analysis is again becoming the key framework for successful investors, replacing the paradigms of narrative formation and growth extrapolation that fueled the bull market of the previous cycle.

The US dollar: From headwind to tailwind?

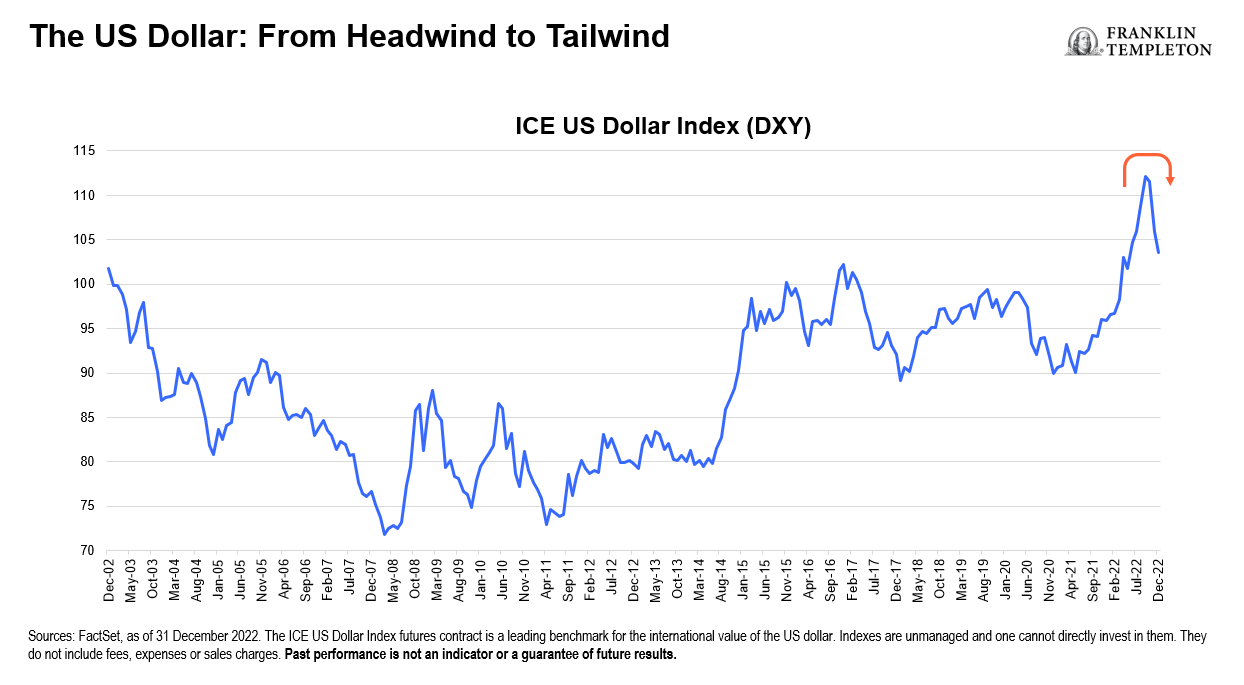

Not only can US investors buy international stocks at unusually cheap valuations, but they can use a strong currency to do it. While international equity valuations stand near 20-year lows, the US dollar is trading close to a 20-year high. But the dollar—one of the most crowded long trades for the better part of two years—now looks vulnerable. In late 2022, net speculative positioning was near all-time highs, technical indicators showed the dollar to be historically overbought, and the dollar’s premium to its long-term average real effective exchange rate (REER) was at record levels.

So, what could bring down king dollar? Fundamentals, for one. Interest rate differentials, relative economic strength (as measured by indicators like the purchasing manager’s index) and comparative current account positions have all supported the dollar but are now reaching extended levels that we believe are likely to mean revert over time. We have seen the dollar begin to roll over in late 2022/early 2023 and expect there will be more to come.

Additional catalysts for a potential dollar decline include:

- A pause in rate hikes or eventual Fed policy pivot that lowers forward interest-rate expectations

- Slower growth in the United States

- Conflict resolution in Europe that supports the euro and reduces US dollar safe-haven demand

We have long advocated investors use the strong dollar to buy discounted assets abroad. We believe this remains a good time to build positions, as an eventual downturn in the dollar is typically associated with the strong performance of ex-US assets.

Conclusion

There is plenty to think about as 2023 begins to unfold. Does recent strength represent a sustainable rebound, or just a bear market rally? When will inflation come down and how high will interest rates go? How will escalating geopolitical conflicts evolve? While we don’t have all the answers, we do believe it is an interesting time to be deploying capital to cheap international markets.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors or general market conditions. Value securities may not increase in price as anticipated or may decline further in value. Investments in foreign securities involve special risks including currency fluctuations, economic instability, and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.