Key takeaways:

- Despite negative headlines surrounding the UK economy, it is showing signs of resilience as consumers continue to draw down on excess savings and the job market remains healthy.

- UK companies show strong balance sheets and their stocks offer compelling valuations.

- UK equities are attractive to many international investors as the British pound remains historically low.

- We prefer stocks of high-quality, dividend-paying UK companies that we believe can provide resilient and growing income streams.

UK economy exhibits resilience

Global economies, and indeed equity markets, began to struggle last year as rising inflation and interest rates led to worries about recessions and market volatility. In the United Kingdom, consumer confidence and retail sales fell precipitously in the autumn of 2022.

This was around the same time that the short-lived Liz Truss administration introduced its disastrous mini-budget that caused chaotic movements in UK asset prices. Although the negative sentiment towards UK assets and its currency reached its nadir in September-October, there continue to be a lot of negative media headlines about the UK economy, stock market and political backdrop. Many international investors remain reluctant to consider UK assets.

In our view, when the market sentiment became very bearish in late 2022, we found a number of opportunities. We believe that if investors hold the line and keep positions in UK stocks and sectors that are tied to the domestic economy, consumer confidence and retail spending, then there are value opportunities as conditions improve.

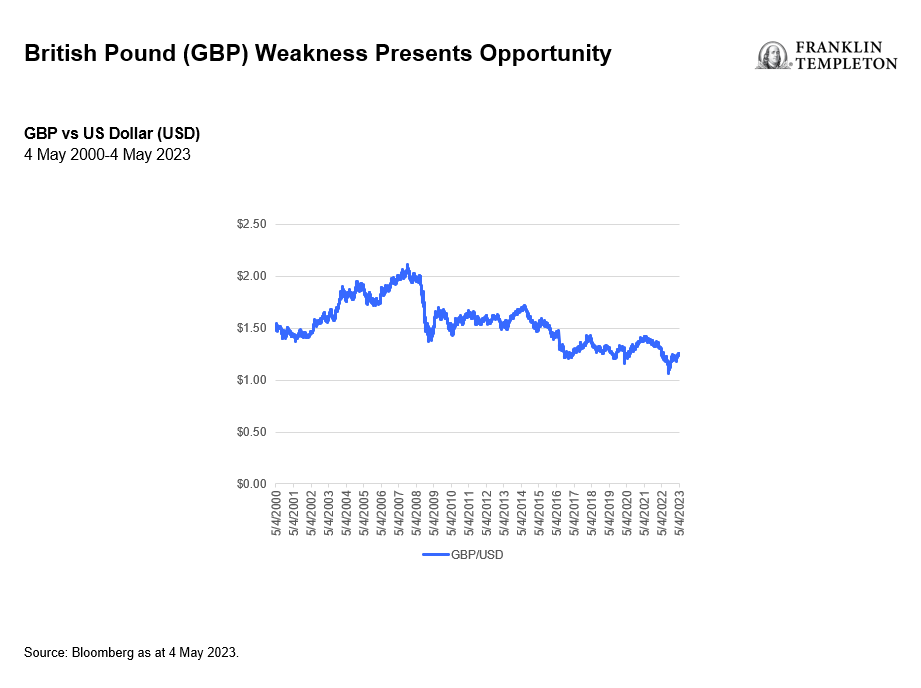

Additionally, even though the outlook for 2023-2024 remains challenging, the outturn for the UK economy is defying the gloomier predictions and is proving more resilient than first feared. As a consequence, UK stock prices have been recovering and the British pound has improved as well. The movement of the UK’s currency is a good gauge of sentiment towards the country.

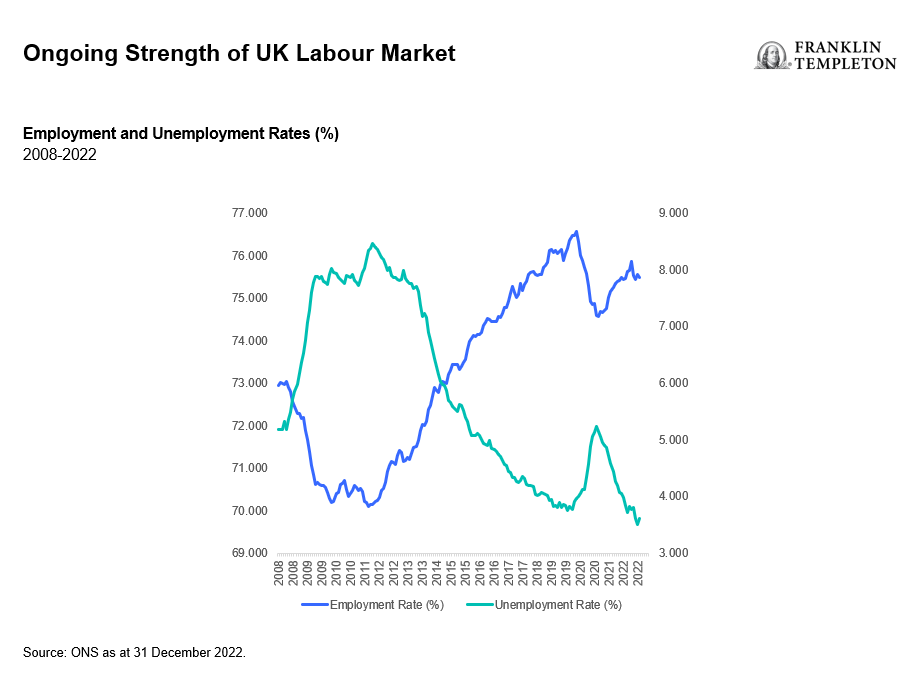

The principal reason that the economy is performing better than expectations relates to the ongoing strength of the labour market, with unemployment at historic lows, while at the same time job vacancies remain elevated as employers struggle to fill vacancies.

Another factor to consider relates to the excess savings built up during the pandemic, providing a spending cushion and helping households manage their way through a higher inflation environment.

UK equities remain attractive

In our analysis, there are several reasons why UK stocks are attractive. First, corporate balance sheets largely appear to be in good health, despite the uncertain economic outlook. This has not always been the case during periods of economic weakness.

Looking across market sectors, aside from financials stocks, corporate debt is at very manageable levels. This means that corporations are in a good position to absorb rising finance costs—as interest rates increase—without upsetting their financial metrics. In our opinion, it would seem there would be little need for distressed rights issues or emergency equity raises, activities that we might have seen in previous economic downturns.

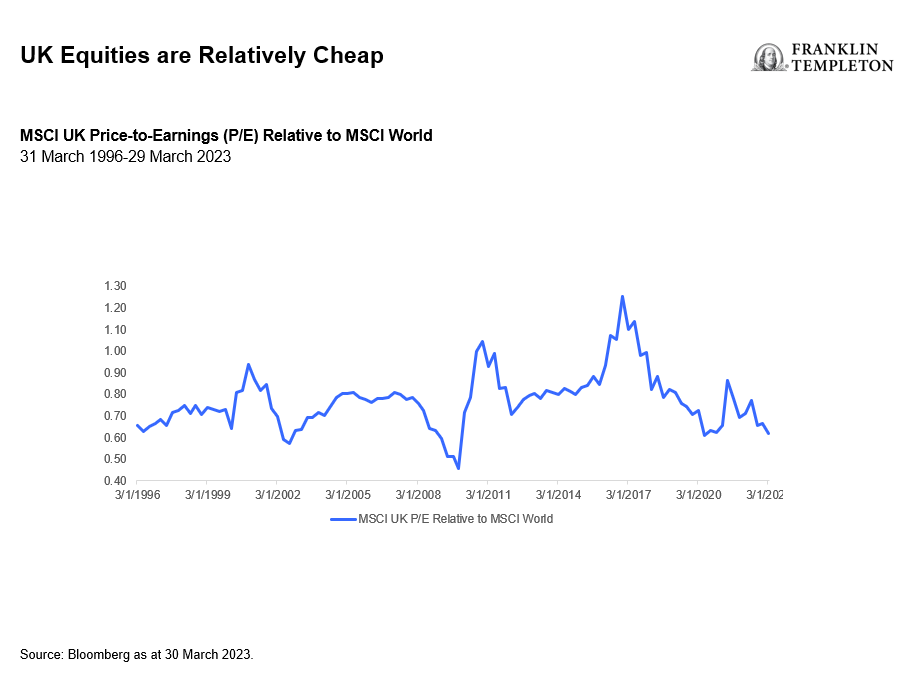

Second is that the UK equity market looks attractive to us on an historical basis with a price-to-earnings (P/E) ratio of around 11x.1 In our analysis, the valuation of the UK equity market also looks more attractive versus its international peers, with the MSCI UK Index 12-month forward P/E at the bottom of its historic range relative to that of the MSCI World Index.2

Third, while the British pound has gone a long way from moving towards parity with the US dollar as market commentators talked about last year, it is still at the bottom of its historic range. This situation reinforces the attractiveness of UK assets to international buyers, in addition to the aforementioned attractive valuations.

We have seen ongoing mergers and acquisitions taking place as international trade buyers, private equity and venture capitalists have continued to acquire UK assets. We believe this trend will continue through 2024.

The banking sector has recently been in the spotlight amidst turmoil in the US banking sector tied to the collapse of Silicon Valley Bank, amongst others. However, the UK banking industry is structured very differently from that of the United States—the latter being composed of several thousand regional banks subjected to relatively ‘light-touch’ regulation.

That said, we believe the US banking crisis will likely lead to more regulatory scrutiny and tighter lending standards in both countries, which will likely affect credit creation and ultimately impact economic growth. We are mindful that any regulatory intervention or political pressure to change the banks’ actions could undermine the positive macro factors that have arisen this year.

In the past 15 years or so, with interest rates near zero, it was difficult for banks to make any meaningful net interest margin between deposit rates and lending rates—the backbone of industry profits. Against such a backdrop, it is unsurprising that banks’ share prices flatlined and were not compelling investment opportunities from our point of view. If, as seems likely, we are at the beginning of a higher interest-rate environment, the prospects for the industry have changed. This has led us to cautiously reconsider the dividend-paying attractions of some of the names in this space.

Focusing on opportunities

Based on all of the abovementioned reasons, we believe that now is a good time to maintain and even add exposure to UK equities. In the current environment, we will continue to take a consistent approach to investing and remain focused on valuation.

We prefer the stocks of high-quality, dividend-paying UK companies that we believe can provide resilient and growing income streams. In our analysis, UK equities offer an attractive yield premium versus other developed markets.

Lastly, we believe UK companies—which derive a large portion of their revenues from overseas—are well-positioned to benefit from an eventual turnaround in the global economy.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested.

Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Smaller and newer companies can be particularly sensitive to changing economic conditions. Their growth prospects are less certain than those of larger, more established companies, and they can be volatile.

Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: Berenberg, “Signs for Optimism,” 12 July 2022.

2. Sources: Datastream, JPMorgan, Bloomberg Finance L.P. as of 5 September 2022. There is no assurance that any estimate, forecast or projection will be realized. Indices are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.