Based on its historical growth and income characteristics, commercial real estate (private real estate) represents a significant allocation for many institutions and family offices. According to the 2022 Institutional Real Estate Monitor,1 real estate represents an 11% global allocation in institutional portfolios, and according to the UBS Global Family Office Report,2 real estate represents a 13% allocation in family office portfolios. In recent years, private real estate has been more accessible to high-net-worth investors due to product innovation, as well as the willingness of institutional-quality managers to bring products to the market.

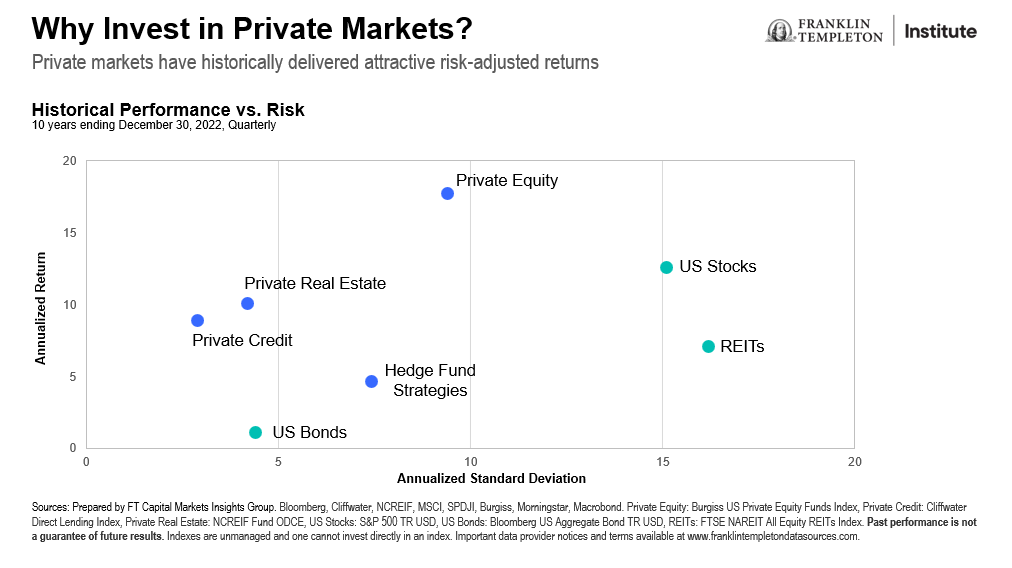

Last year, we were reminded of the limitations of the 60/40 portfolio3 and the need for an expanded toolbox to meet client goals. Consequently, advisors and investors have sought alternative sources of growth and income, and an effective way to dampen volatility and hedge inflation. As the data below illustrate, real estate has historically delivered attractive risk-adjusted returns relative to stocks, bonds and publicly traded real estate investment trusts (REITs).

Private real estate has historically delivered higher income than most traditional fixed income options4 and publicly traded REITs. Private real estate managers also can increase rents in rising inflationary environments.

The current market environment

After interest rates rose dramatically throughout 2022 and the early part of 2023, some have suggested that this would provide headwinds for real estate. Coupled with the tighter credit conditions in the post-Silicon Valley Bank (SVB) environment, and the fact that office and retail sectors were still struggling with occupancy levels, there were concerns about risks across the overall private real estate market.

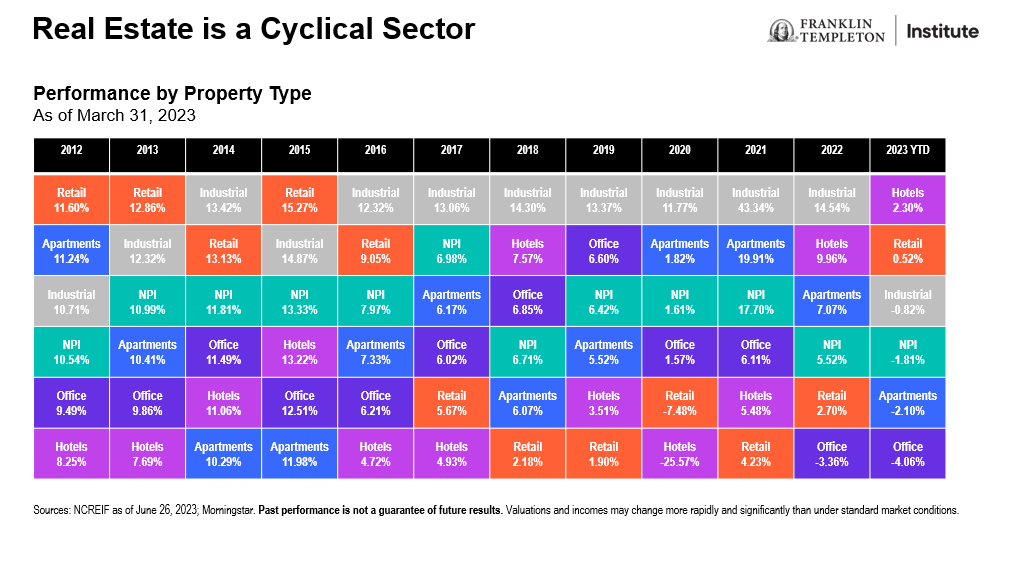

As the data below show, the office sector was struggling before the COVID-19 pandemic and will likely struggle for the foreseeable future. However, private real estate represents a diverse set of sectors, which are responding to a changing US economy. While offices have struggled over the last several years, the industrials property sector has been a growing sector of the market, driven by Amazon fulfillment centers and other industrial-use facilities.

Real estate valuations are ultimately about supply and demand. While there might currently be an oversupply of office and retail space, there is a shortage of industrial and multifamily real estate. We believe that the changing economy is driving growth in industrials, which represents a long-term secular trend. Millennials are entering their peak earning years, and consumers will continue to buy online, which leads to increased demand for fulfillment centers across America. E-commerce sales are forecast to grow at 5-10% annually,5 continuing to gain market share from brick-and-mortar retail stores.

Multifamily housing represents another bright spot with pent up demand and an overall housing shortage (3-5 million units by some estimates).6 We have experienced strong job growth and a migration from high-tax states (New York, New Jersey, Connecticut and California) to low-tax states (Florida, Texas, North Carolina and Tennessee), which is where we see many opportunities in multifamily housing.

With a growing remote workforce and flex schedules, the office building segment will continue to face challenges in evolving to meet today’s needs. Vacancy rates are elevated, sentiment is negative and lending conditions are tight. Certain markets may regain their prior occupancy levels, while others may need to revert their office space into a more modern and scalable solution.

Not all real estate is created equal—and not all sectors will provide the same results in the future. We believe advisors and investors should consider hiring an experienced manager who can allocate capital based on the attractiveness of the various sectors and underlying investments. To learn more, please visit https://www.franklintempleton.com/investments/capabilities/alternatives and alternativesbyft.com.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Equity securities are subject to price fluctuation and possible loss of principal. Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Alternative strategies may be exposed to potentially significant fluctuations in value.

Real estate investment trusts (REITs) are closely linked to the performance of the real estate markets. REITs are subject to illiquidity, credit and interest-rate risks, and risks associated with small- and mid-cap investments.

Privately held companies present certain challenges and involve incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

__________

1. Source: Institutional Real Estate Allocations Monitor, 2022.

2. Source: 2023 UBS Global Family Office Report.

3. Source: MarketWatch, “60/40 portfolio—dead or alive?” January 11, 2023.

4. Source: Bloomberg. Private real estate is represented by the NFI-ODCE Index. Stocks are represented by the S&P 500. Bonds are represented by the Bloomberg US Aggregate Bond Index. Publicly Traded REITs are represented by the FTSE NAREIT All Equity REITs Index. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

5. Sources: Moody’s Analytics, CBRE-EA, Clarion Partners Investment Research, April 2023. There is no assurance that any estimate, forecast or projection will be realized.

6. Source: Clarion Partners, June 2023.