In a recent roundtable, Mutual Series’ Chief Investment Officer Christian Correa and Portfolio Manager Mandana Hormozi discussed their recent trip to Japan and what they see ahead for the local market, and economy. Here are their key takeaways.

- Inflation is having a positive effect on the business environment in Japan, with many companies able to differentiate their products beyond low prices.

- At the same time, the country is taking a dynamic view toward businesses, and companies are more willing to talk about future growth and how they can change to improve returns on capital.

- Companies are more able to take risks now than they have in the past to push on potential growth drivers.

An edited transcript of their conversation follows.

You both just got back from a trip to Japan. There’s been a lot of talk about the opportunities in Japan of late, and the market has been relatively strong. The economy appears stronger than it has been in a while, and the country’s businesses look to be in the middle of major changes in how they approach corporate governance and shareholder returns. Tell me a bit about what you encountered while you were travelling there.

Mandana: What I was most surprised about was the dynamism in the market. I wasn’t expecting that. And the big change seemed to be inflation—everybody was talking about inflation, whether it was the companies or consumers we came across. Obviously, the rates of inflation are very different between Japan and the United States, but unlike in the United States, in Japan companies seemed to be happy about it because it has allowed for differentiation in goods and services beyond just pricing, and consumers were accepting the price increases. So, a company can try to differentiate on another factor beyond just price, which has been a big market driver for 20+ years, such as quality, innovation, etc.

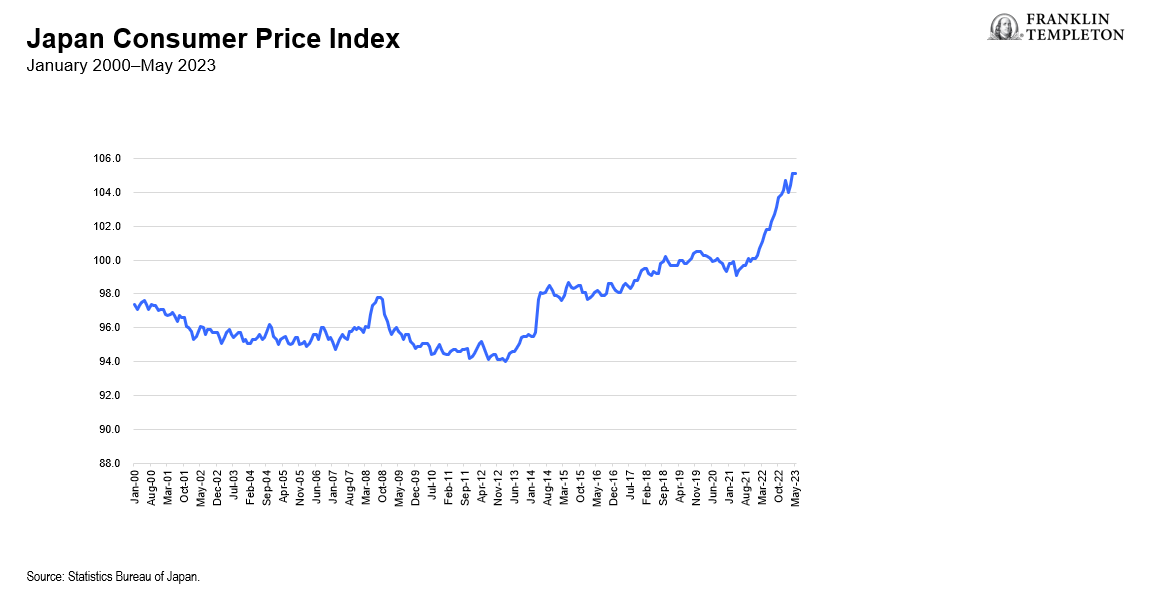

Exhibit 1: Japanese Consumer Prices Are Finally Rising (right click on chart to enlarge)

And then the Tokyo Stock Exchange’s changes and their impact on companies was also a surprise to me, as they look to push companies to take steps to raise their book values above one to remain listed on the exchange. With many companies trading below book value, this is expected to boost returns over time. Obviously, there isn’t an enforcement mechanism identified yet, but companies seem to have been taking it quite seriously and taking steps to get above book value, which is the baseline target.

The other thing I noticed was that everyone kept saying, “In Japan, things take a long time.” The culture is slow to embrace change, and it was a reminder that (former) Prime Minister Shinzo Abe started this corporate governance reform process over a decade ago. It’s not necessarily that this time is different, but evolution takes a long time, and we’re starting to see some of the impact of changes that were initiated under prior regimes.

Christian, anything to add?

Christian: Japanese corporates for a long time had a reputation for being shareholder-insensitive and having an insular corporate culture in a capital markets sense. There was a view that the Japanese market was big enough, and it didn’t need outside investors. There was also a view that its stakeholder capitalism model was the right model, and other views were not appreciated. I was pleasantly surprised at the openness to ideas that I think in the past had been dismissed.

So, I now see a more dynamic view toward businesses and a willingness to talk about growth paths, which are easier to talk about generally. But also, there is a realization of where things might need to change, and maybe a business needs to be shut down or not invested in. There is greater responsiveness to the returns on capital and not just prioritizing other stakeholders. When we were in Japan, we consistently saw management teams that were open and willing to engage in English. From a shareholder perspective, that has certainly not been the case in the past.

Along those same lines, what are some of the catalysts Japanese businesses are undertaking?

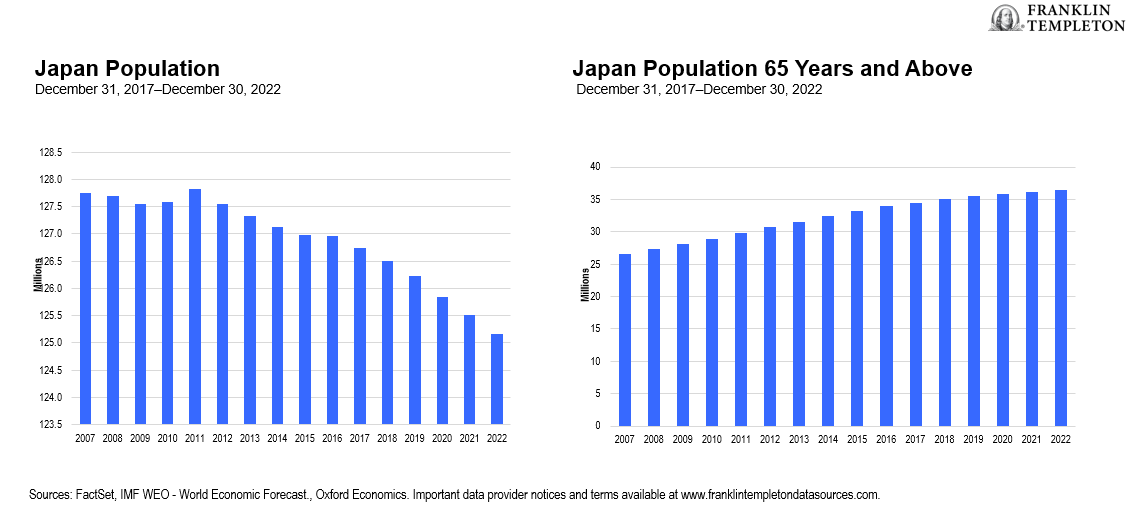

Christian: I think the overarching catalyst is a societal understanding that demographics have changed slowly and then quickly. Japan is an aging society where the ability to add more labor is not going to be available.

In order to fund the government, social insurance payments, and health care, the Japanese economy needs to increase the returns on its capital base. And that shows up in things like the inflation that Manda was talking about; a little bit of the dynamism in the economy being necessary to facilitate returns. The Tokyo Stock Exchange’s push to identify underperforming companies and then shame them into behaving better is another example. An underlying need for the Japanese economy to be able to provide for its people is driving these efforts.

Exhibit 2: The Japanese Population Is Shrinking and Aging, Quickly (right click on chart to enlarge)

Just thinking back, Michael Price had said similar things about Europe back when he ran Franklin Mutual Series in the 1980s and 1990s. Companies weren’t run well, they weren’t shareholder- friendly, and he saw an opportunity to go in there and shake things up. Do you see a similar environment in Japan? And following on, do you see opportunities for Mutual Series to be more actively engaged in Japan?

Christian: We definitely see more opportunities to be actively engaged. However, engagement requires a certain sensitivity to the market you are operating in. When Michael Price wanted to invest more in Europe years ago, he brought in people from the region with expertise to help facilitate that. Now, we don’t have any plans to pursue a similar approach, but we do have a cultural sensitivity in terms of trying to be constructive partners with the Japanese companies we are investing in.

Mandana: Active engagement is our strategy, as opposed to activism. And I think that approach has been constructive. Companies have been more able to take the risk now than they have in the past to push on potential growth drivers for their businesses. The opportunity is there.

As we’ve seen before, Japan has burned investors in the past expecting big changes. What makes you confident that this is real?

Christian: I think the most important thing is that you have multiple agents of change all pushing in the same direction, which has not been the case in the past. The government is pushing, the stock exchange is pushing, shareholders are pushing, and inflation is creating the opportunity for dynamism. And then, when combined with valuations that are materially different than they were 10 or 20 years ago, there is an opportunity.

Mandana: I think you also have a layer of management at some of these companies that is a little younger than in the past. There is a younger group of management that’s willing to shake it up.

Christian: Maybe younger people have grown up during the deflation years and with a more global perspective than a prior generation of management that grew up during the boom times and had a very Japan-centric view of the world. There was a whole generation of management whose identities were forged in the 1980s when Japan was viewed as the preeminent economy in the world. That ended when the bubble ended.

How does the potential for a stronger yen inform your thinking about Japanese stocks?

Christian: In the big picture, like everything, we try to ignore the short-term movements and focus on the bigger picture. The bigger picture is that Japanese exporters have become much more competitive because the yen has depreciated over the past decade, so it’s a boon to Japanese corporate activity.

Let’s talk a bit about the potential investment opportunities. Where are we looking for opportunities on an industry basis?

Christian: We’re looking broadly. There are certain industries that are better represented in the Japanese economy. The banks and trading companies are financial actors, and their success or failure depends on a mixture of local market and non-Japanese markets. And they may present interesting opportunities.

A domestically focused company, like a retailer or a consumer goods company, can also be interesting. The Japanese market is not growing. We talked about it earlier, but demographics mean retailers are not going to be selling more shoes in Japan 10 years from now than they are today. So, if you’re a consumer-oriented company, you need to have some path forward, whether it’s “I’m going to sell my beer outside of Japan” or “I’m going to take my successful retail format and use it in a different market.”

What we’re looking for as investors are inexpensive companies, undervalued companies, where we see these kinds of dynamic opportunities, along with management teams that are willing to engage with us and work to try to seize those opportunities.

Mandana: Some of the points we’ve made about the broader Japanese market and the macroeconomic opportunity apply to pretty much any company in Japan.

Along those lines, China has been a big focus for a lot of exporters. Is there any concern around what’s going on there, geopolitically, or economically?

Mandana: I would think of it as two views. Clearly, from a macro perspective, a slower-growing Chinese economy is going to have a broad global impact, and Japan is a significant exporter to China.

Geopolitically, Japan could be a beneficiary as people look to diversify supply chains. As wages have risen in China, the huge wage gap that existed 30 years ago for Japan relative to China and some of its other neighbors has narrowed quite a bit. And Japan has a highly educated population. Labor mobility has been an issue for Japan for a long time, if there is any impetus to increase it, then Japan could be one of the beneficiaries of manufacturers looking to diversify outside of China. Investors are also looking at geopolitics and looking to diversify outside of China, and Japan is clearly a beneficiary of that trend, too.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

To the extent a strategy invests in companies in a specific country or region, it may experience greater volatility than a strategy that is more broadly diversified geographically.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.