In the last several years, we have experienced the longest equity bull market in history, a global pandemic and the highest level of inflation since the 1980s. And since March 2022, the US Federal Reserve (Fed) has raised interest rates 525 basis points (5.25%). Throughout this period, we have seen a natural rotation of leading and lagging asset classes as we’ve moved from one economic regime to the next.

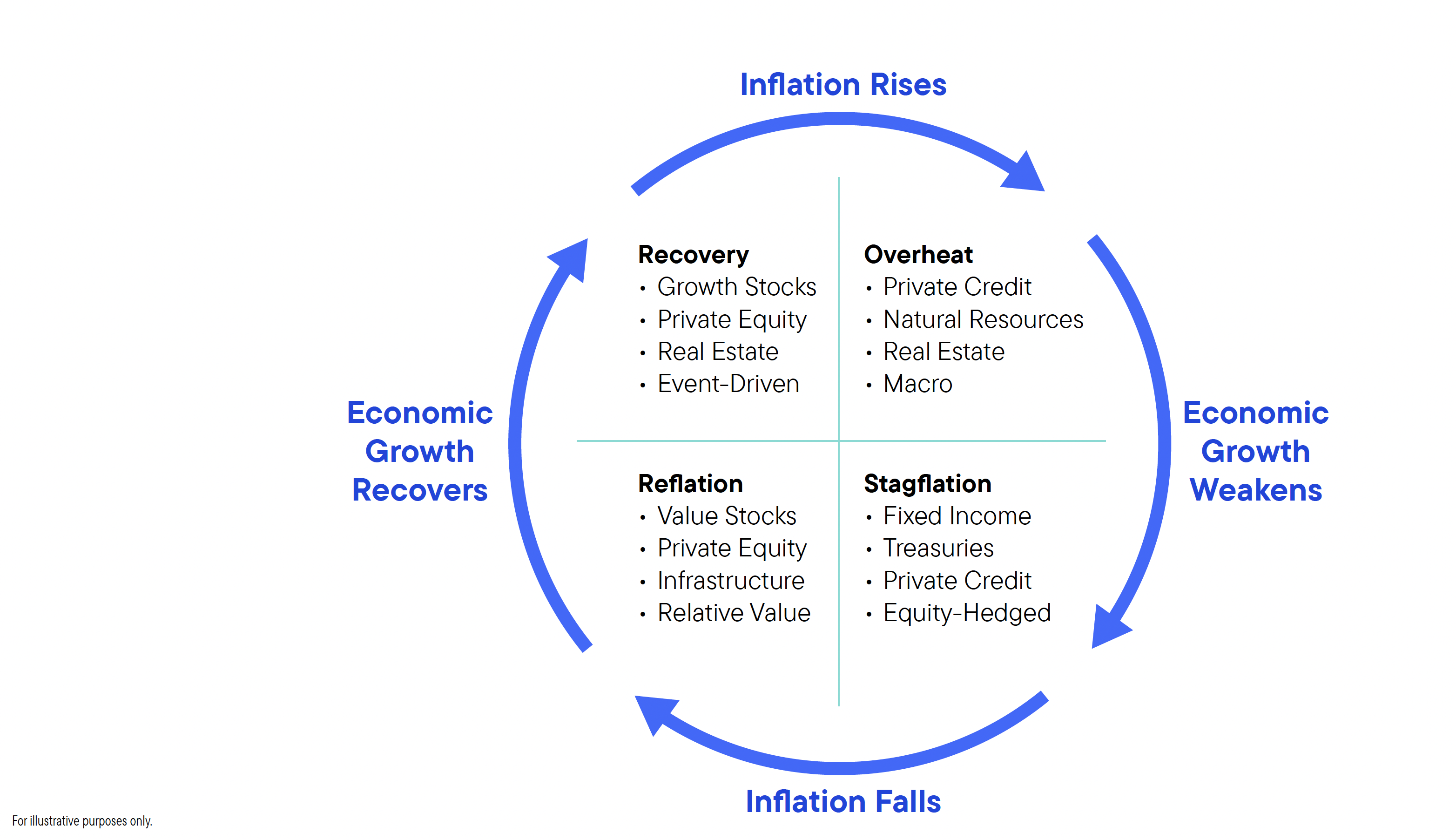

We recognize the difficulty in trying to time the market—but also accept that certain environments reward assets classes while punishing others, only to reverse course as we move through economic and market cycles. As the exhibit below illustrates, economic cycles follow a path of inflation rising, economic growth weakening, inflation falling and economic growth recovering—and there are certain asset classes that thrive as we move through these cycles.

For example, as the economy recovers, private equity and growth stocks do better; and as economic growth weakens, fixed income and private credit do better. Intuitively, we can all agree that equities outperform in “risk-on” environments, and fixed income does better in “risk-off” environments. However, there are often mixed signals, where some indicators are positive, while others are negative.

Regime-based analysis

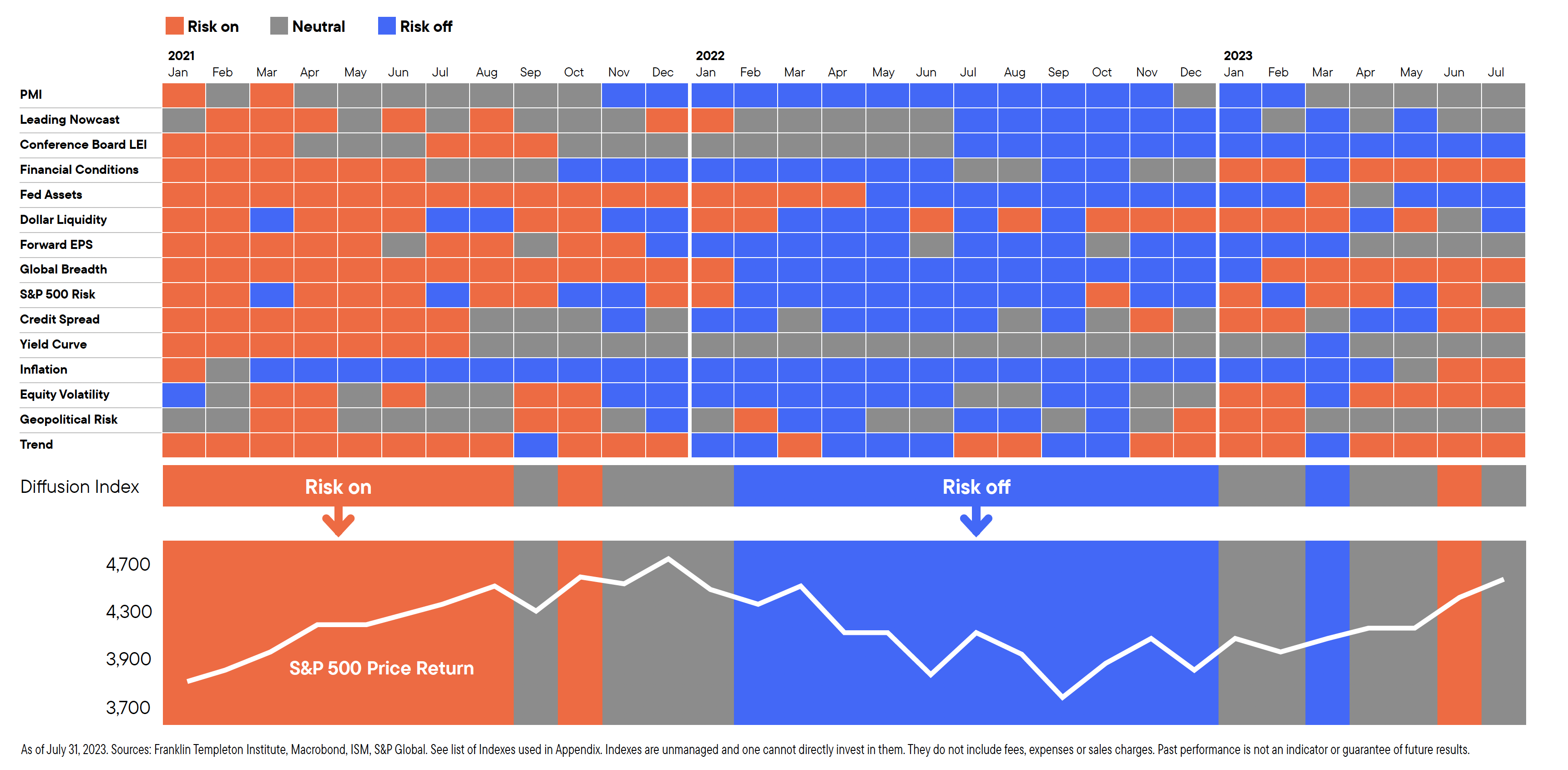

To help advisors in evaluating these mixed signals, we built a proprietary dashboard of 15 independent economic indicators, including Purchasing Managers Index (PMI), Leading Economic Indicators (LEI), forward earnings-per-share (EPS), credit spreads, inflation and geopolitical risks, among others. We determine whether the majority of the indicators are positive, negative or neutral. We treat each indicator as being equally relevant.

Using regime-based analysis

We are not suggesting trying to time the market—but rather illustrating the nature of asset class results across regimes. Whether or not you incorporate the regime-based model for tactical positioning, the economic indicator dashboard may be a useful tool in discussing the prevailing market conditions with clients. The regime analysis can also help you to frame discussions. Understanding how the various asset classes perform across regimes can be helpful in putting capital to work and/or conducting quarterly reviews with clients.

Note, we view alternatives as long-term investments, and would not suggest trying to be tactical with these illiquid assets. Advisors may choose to be tactical with their liquid investments—traditional stocks and bonds. To learn more about regime-based analysis, and the valuable role that alternatives can play in client portfolios, please visit our site or follow me on LinkedIn.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Equity securities are subject to price fluctuation and possible loss of principal. Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Alternative strategies may be exposed to potentially significant fluctuations in value.

Privately held companies present certain challenges and involve incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.