Across the United States, the number of projects involving real assets is increasing. Recent legislation is fostering increased US production capacity for batteries and semiconductors, greening the economy and bringing high-speed internet to rural America. Commodities, metals, industrial equipment and other natural resources are in heavier demand. As a result, the surge in spending on real assets may benefit machinery makers and miners and create new investment opportunities in value-oriented industries.

Legislation supports real asset investment

The Inflation Reduction Act (IRA), Infrastructure Investment and Jobs Act (IIJA) and CHIPS and Science Act are boosting US manufacturing and infrastructure projects. As such, companies are building new US facilities for semiconductors and electronics, clean energy, biomanufacturing and heavy industry. This spending is driving demand for materials such as copper, steel and other metals, rebar, concrete and asphalt, in addition to heavy machinery and other construction site rentals. Generally, value-oriented companies produce these products, and we expect large amounts of spending on new and ongoing projects to support demand.

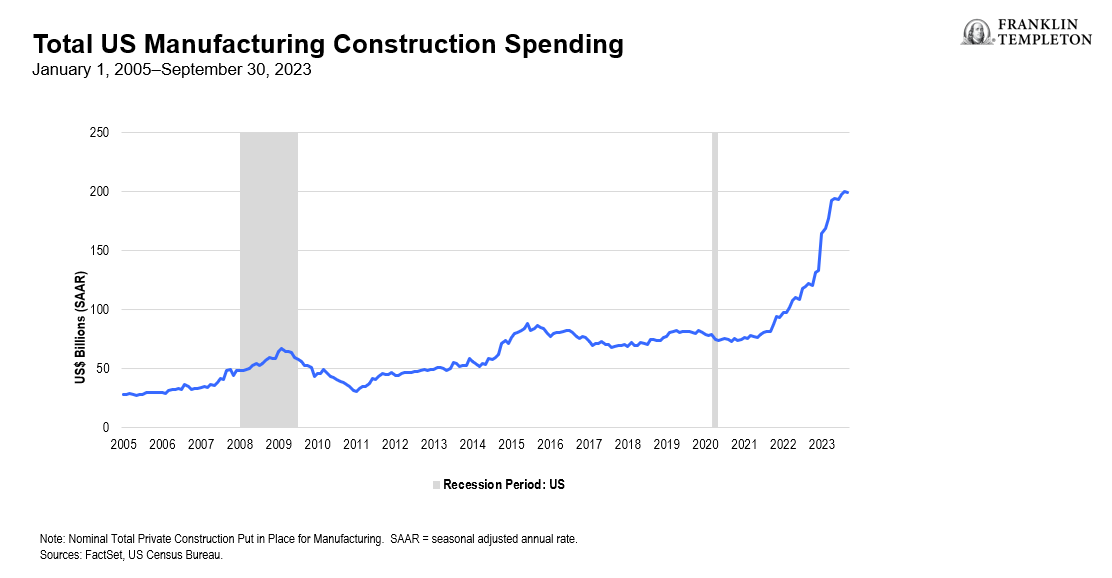

The Biden administration’s fiscal year 2024 budget proposal sets aside US$70.2 billion for transportation-related infrastructure projects.1 Estimates from the White House propose that spending from the IRA, IIJA and CHIPS and Science Act could total US$3.5 trillion over the next decade.2 We expect these Acts to lead to increased public and private investment in the nation’s infrastructure and manufacturing capacity, and according to the US Census Bureau, US manufacturing investment has grown significantly since the IRA, IIJA, CHIPS and Science Act were passed.

(right click on chart to enlarge)

Real assets can be green

Like heavy machinery and manufacturing, steel mills and concrete plants generally aren’t associated with the green economy. However, these materials create electric vehicle infrastructure, build wind turbines, and start other green projects. Electric vehicles use about 175 pounds of copper per car, nearly four times the amount used in a traditional vehicle, and it’s estimated that electric vehicle battery manufacturing accounted for two-thirds of global copper demand growth in 2022.3 In addition, demand for batteries keeps growing. Electric vehicle and battery manufacturing accounted for US$210 billion in investments as of late 2022, up from US$51 billion at the end of 2020.4 While manufacturers are working to design batteries requiring less metal, demand should likely remain strong as the transition to electric vehicles accelerates.

Growing demand for metals used in batteries could help support mining companies’ stock prices. In addition, many car manufacturers, traditionally viewed as value companies, are revving up their electric vehicle production. We think increased electric vehicle market participation may lead to stronger sales and market share. We also expect relocation of battery and vehicle manufacturing to reduce costs over time for vehicle makers.

A wind turbine also represents green energy, despite being composed mostly of steel5 and requiring tons of concrete and more steel to anchor it.6 As the United States generates more electricity from wind farms, we expect demand for these real assets to be supported as an increasing number of turbines are constructed. In addition, wind-, solar- and water-generated electricity depend on the environment to generate power and need oil- and natural-gas-generated energy as backup. Even with the green transition, we think demand for these traditional energy assets will remain.

Real assets and the internet

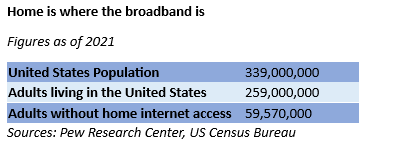

American households love their internet access. According to a 2023 survey, people access the internet 144 times per day via their smartphones.7 After phone usage, home internet access is the most popular way to get online. However, it’s estimated that only 77% of US adults have home internet access, and that number falls to 72% when focusing exclusively on rural areas.8 President Biden’s IIJA attempts to remedy this, earmarking US$42 billion to bury miles of fiber optic cable9 to expand US household high-speed internet access. More cables—made of glass and steel fibers—will be needed, and workers will need heavy equipment to lay the cable,10 which can lead to real productive growth for companies engaging in these projects. As more people gain access to high-speed internet, faster subscriber growth rates could cause communications company shares to rerate over time, while generating faster growth for companies that produce fiber optic cable components and manufacture the cable.

Home is where the broadband is

We think the manufacturing and green energy expansions, along with the broadbandification of rural America, will support demand for products and services provided by companies operating in value-oriented sectors. A construction boom requiring metals, building materials, heavy machinery and labor is underway. The push toward a green energy future may not be the death knell for high-polluting industries such as mining, cement and oil that many have anticipated. More high-speed internet for more people means more cable, people to bury the cable, and subscribers for communications companies. All of these are hard asset intensive; all of these present new opportunities for value investors.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

To the extent a strategy invests in companies in a specific country or region, it may experience greater volatility than a strategy that is more broadly diversified geographically.

Investment strategies which incorporate the identification of thematic investment opportunities, and their performance, may be negatively impacted if the investment manager does not correctly identify such opportunities or if the theme develops in an unexpected manner.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Value securities may not increase in price as anticipated or may decline further in value. The investment style may become out of favor, which may have a negative impact on performance.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

____________________________

1. Source: “Infrastructure Still a Theme of Biden FY 2024 Budget Proposal.” Engineering News Record. March 9, 2023.

2. Source: “Remarks on Executing a Modern American Industrial Strategy by NEC Director Brian Deese.” Whitehouse.gov. October 13, 2022.

3. Source: “Innovation in EVs seen denting copper demand growth potential.” Reuters. July 9, 2023.

4. Source: “Will the auto workers’ strike jeopardise Joe Biden’s manufacturing boom?” The Economist. September 24, 2023.

5. Source: “What materials are used to make wind turbines?” US Geological Survey.

6. Source: “How do you anchor a giant wind turbine? With a giant suction cup, of course.” World Economic Forum. September 12, 2016.

7, Source: “Americans Check Their Phones an Alarming Number of Times Per Day.” PCMag. May 19, 2023.

8. Source: “Demographics of Internet and Home Broadband Usage in the United States.” Pew Research Center.

9. Source: “Rural states likely to benefit the most from funds to improve broadband access.” NPR. June 28, 2023.

10. Source: “How Fiber Optic Cables are Made.” OFS Optics Company.