I recently had the pleasure of interviewing Jackie Klaber, Head of Alternative Investments at Rockefeller Capital Management. We explored the process for evaluating and allocating to alternative investments, discussing a range of issues including advisor adoption, product evolution, due diligence, and the need to demystify alternatives with investors.

The industry often uses jargon that is confusing to investors, pushing clients away from the types of investments they should be embracing. Jackie shared Rockefeller’s approach to simplifying the conversation about alternatives.

“There’s so much jargon out there. A lot of complexity, perceived complexity. We really try to unpack the strategies and make it very transparent on a fundamental basis. What are our clients going to be owning? What can they expect in terms of their portfolio? How much volatility or fluctuation in monthly values? How much enhanced return potential? What is this going to look like both at the individual strategy level and then at the portfolio level where it really matters, where everything comes together?”

Similar to our approach at Franklin Templeton, Jackie suggested advisors focus on the role each investment plays in client portfolios, and how they may help in achieving specific goals. “There are two main buckets that we tend to use when categorizing our offerings. One is equity upside opportunities, capital appreciation opportunities, and the second is volatility dampening or absolute return-oriented strategies. We apply those two categories across every offering, and you could think about those two buckets as aligning to the traditional 60/40 model, so really boiling it down to those basics.”

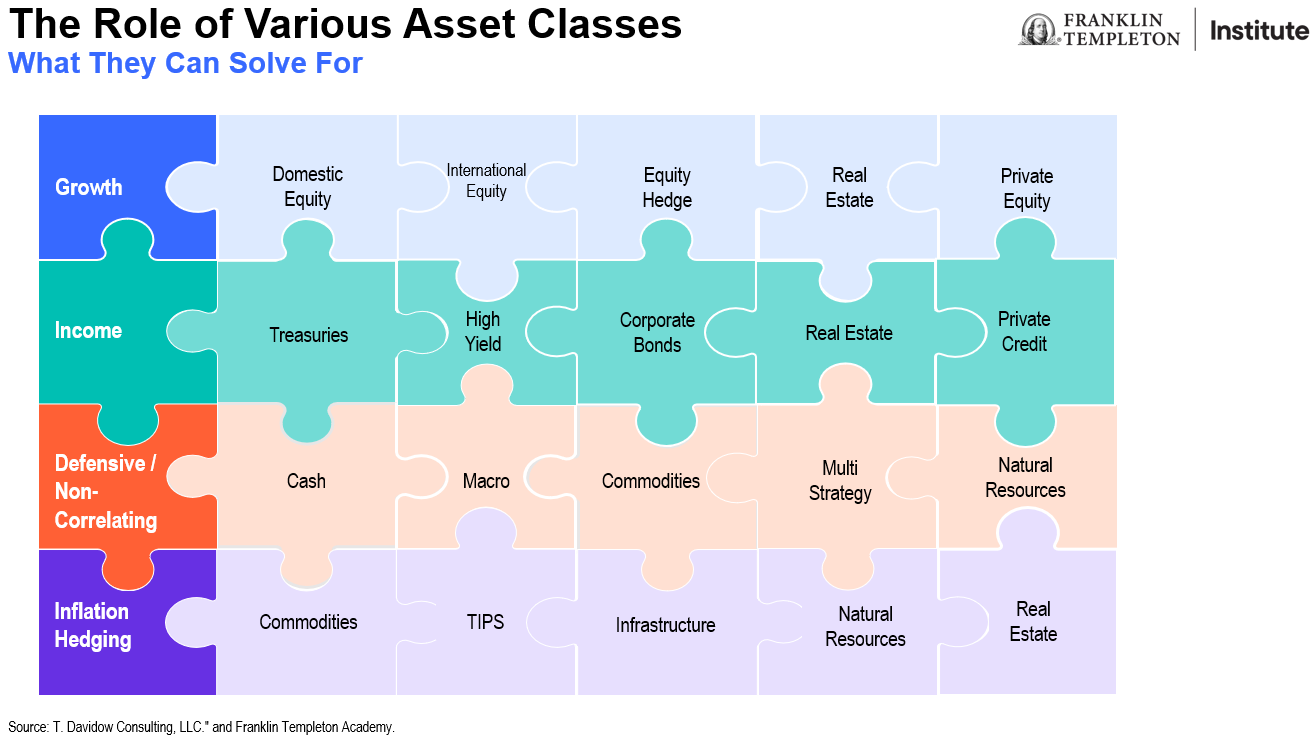

We distill this into the following framework which focuses on the four primary roles of investments—growth, income, defense, and inflation hedging.

This simplified approach helps advisors communicate why we are adding alternatives, and what role they play in client portfolios. It can also be used to illustrate how to allocate to alternatives—sourcing capital based on the role that they play. For example, private equity should be sourced from the growth bucket, private credit from income, macro from defense, and real estate from inflation hedging. Certain alternatives, like real estate, can play multiple roles in portfolios.

This approach also helps move the discussion with clients beyond “did each investment outperform some arbitrary benchmark.” Instead, each investment should be evaluated based on their role within the portfolio. Did the private equity manager provide incremental growth? Did the private credit manager provide income? Did my macro manager dampen portfolio volatility? Did my real estate manager hedge the impact of inflation?

Make sure you don’t miss an episode of our Alternatives podcasts by subscribing to Alternative Allocations on Apple, Spotify or wherever you get your podcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Investments in many alternative investment strategies are complex and speculative, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative strategies may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity. Diversification does not guarantee a profit or protect against a loss.

Risks of investing in real estate investments include but are not limited to fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by local, state, national or international economic conditions. Such conditions may be impacted by the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, and environmental laws. Furthermore, investments in real estate are also impacted by market disruptions caused by regional concerns, political upheaval, sovereign debt crises, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars). Investments in real estate related securities, such as asset-backed or mortgage-backed securities are subject to prepayment and extension risks.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

An investment in private securities (such as private equity or private credit) or vehicles which invest in them, should be viewed as illiquid and may require a long-term commitment with no certainty of return. The value of and return on such investments will vary due to, among other things, changes in market rates of interest, general economic conditions, economic conditions in particular industries, the condition of financial markets and the financial condition of the issuers of the investments. There also can be no assurance that companies will list their securities on a securities exchange, as such, the lack of an established, liquid secondary market for some investments may have an adverse effect on the market value of those investments and on an investor’s ability to dispose of them at a favorable time or price. Past performance does not guarantee future results.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.