The call to the post for the US manufacturing renaissance happened earlier than most realize. While it’s true that recent stimulus efforts are bolstering reshoring efforts, legislation isn’t the entire reason for the revival. The growth of artificial intelligence (AI) and its role in automation, semiconductor chip foundry and data center construction, energy grid electrification, and increases in green energy generation, are all changing the US industrial landscape. As reshoring efforts mount, manufacturing increases, and investors recognize the compounding value, we think fundamental research and prudent stock picking will be crucial for identifying the pacesetters of a coming rerating horserace.

The lost decade of industrials

For much of the early 2000s, North America underinvested in its industrial base. Starved for growth, US-based capital goods companies focused on productivity and margin improvement, moving supply chains to cheaper locations. Globalization and outsourcing were the trends. Former President Donald Trump’s tariffs on Chinese goods further complicated supply-chain logistics in 2016. These new policies made supply-chain security an issue for boardrooms, kindling discussions about reshoring.

In 2020, the pandemic broke supply chains and accelerated reshoring efforts. By 2022, a US capital expenditure renaissance was underway, with companies prioritizing supply-chain security while simultaneously preparing for a growth cycle ahead. Companies have and continue to commit significant capital to these projects after years of only modest spending, as exhibited by the data on private fixed investment in manufacturing (see Exhibit 1) from the US Census Bureau.

Exhibit 1: US Infrastructure Spending Booms

Poised for a breakaway

Four horses are carrying the United States out of the lost decade and into a period of robust capital investment, all of which are influenced by increases in AI capability and utilization. First, factory automation has long been a focus of industrial capital spending because it enhances productivity. To reduce costs, companies invested heavily in automation during the years when organic growth was low. Recently, breakthroughs in AI have increased automation’s breadth and complexity, shifting the nature of manufacturing jobs to more technical, computer-savvy positions, and thereby reducing the need for factory-floor labor. As a result, we expect demand for automation equipment and services to rise over the coming years.

Next, chip foundries and data centers are some of the major construction projects fueling demand for building materials, construction equipment, labor and other manufacturing components. In addition to the added supply-chain security that onshoring brings, these businesses are bringing manufacturing home because AI innovation is increasing the volume and complexity of chips US companies need. More data centers are crucial to providing adequate computing power.

Meanwhile, energy grid electrification has been an important focus. More data centers need support from a robust electrical grid. Other electrification initiatives, such as electric vehicles (EVs), also require the buildout of their own charging infrastructure and higher volume battery production, requiring more building materials and expanded manufacturing efforts.

To satisfy the need for more electricity, a US green energy transition has been underway. Green energy includes any project that produces cleaner energy, such as increased utilization of renewables or improvements in the ways we heat and cool our homes, offices and data centers. Individuals and companies are participating, supporting demand for copper wire, steel and concrete to make wind turbines, equipment used to manufacture heat pumps and environmentally friendlier industrial-size cooling systems, and other industrial components.

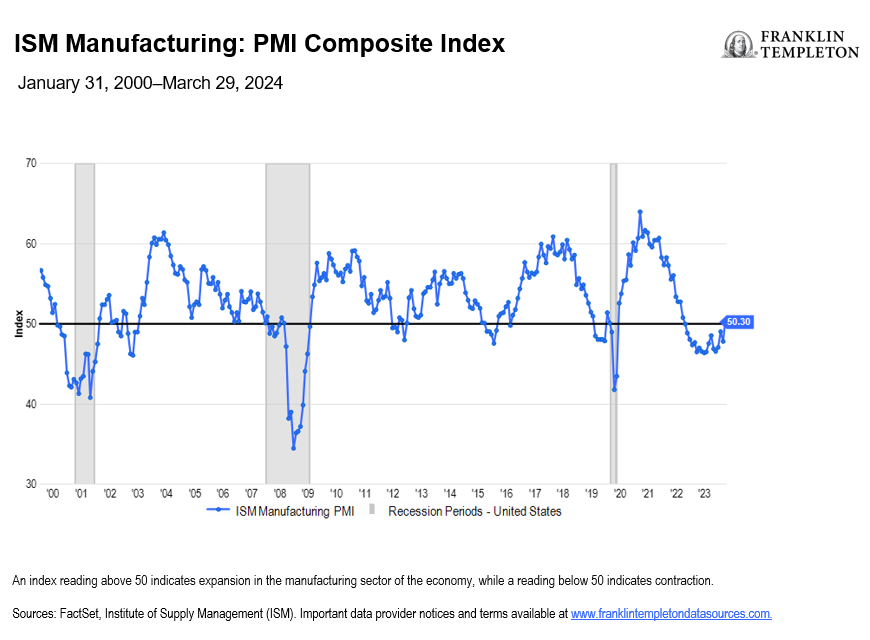

In addition to these secular themes, we think a better economy may also drive stock price appreciation. The Institute for Supply Management manufacturing Purchasing Manager’s Index (PMI) has contracted for 16 months, a length of time that has historically signaled a coming revival (see Exhibit 2). In our opinion, a transition to expansion could be an additional catalyst helping these industrial companies rerate.

Exhibit 2: ISM Manufacturing: PMI Composite Index

Identifying the pacesetters

It can be hard to tell which horse should pull away on the home stretch. Some stocks may initially benefit from early trends and rally, only to see their outperformance fizzle midway through the race. Some companies may lag in the early going as investors are unclear as to how these secular themes may increase demand for their products. However, once it becomes clear that these companies do benefit from one or more of these four secular themes, they may catch up and even surpass the early leaders. As of right now, we think there are several companies that fit this latter category and that an opportunity for additional future rerating could exist for some of these organizations if management decides to educate investors on how their company benefits from current trends.

We also believe investors should look for companies that have the capacity for future organic growth, such as the ability to convert a significant portion of their existing customer base to new products or build a more competitive moat. How organic growth leads to earnings growth over the three-to-five-year time horizon is crucial as it helps investors determine if growth expectations are already baked into the price, or if the horse has room left to run.

The United States is investing in its industrial base to reinforce supply lines, boosting manufacturing in areas related to automation, semiconductor chip foundry and data center construction, power grid electrification and increased green energy generation. Many organizations stand to benefit. The challenge is to find companies trading at a discount to their future fair value and avoid the frothy ones. We believe a deep understanding of US capital goods companies can help identify strong participants in this rerating horserace.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal. Active management does not ensure gains or protect against market declines.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.