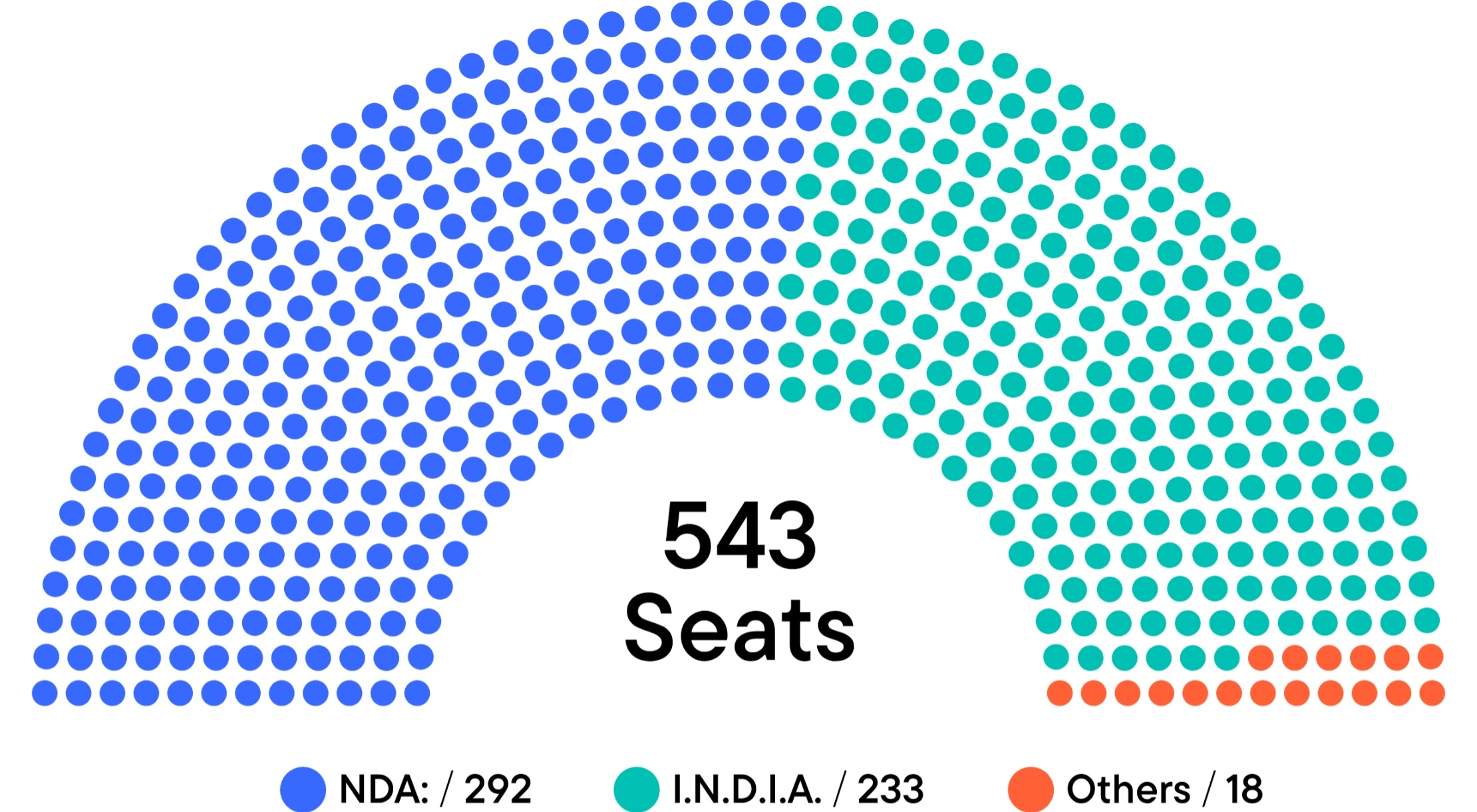

The 2024 India election result saw Narendra Modi’s Bharatiya Janata Party (BJP) win the largest number of seats, albeit a smaller number compared to the 2019 election. While disappointing and with potentially negative consequences for selected market sectors, we don’t believe it will change the policy direction of the BJP-led National Democratic Alliance (NDA). The focus will remain on developing the manufacturing base via the Production Led Incentives (PLI) scheme, the transition of growth in infrastructure from the public to the private sector, emphasis on areas. including renewable energy and stimulating consumption, and with potentially renewed attention on rural incomes.

Exhibit 1: Lok Sabha Political Groups

Source: National Portal of India. Data correct as at 15:00 GMT, June 4, 2024.

On manufacturing

The BJP will likely push ahead with developing India’s manufacturing base during its third term. It has had significant success in attracting major Taiwanese contract manufacturers to assemble consumer electronics for leading global brands. This has created significant employment opportunities.

The PLI scheme has been a success, particularly in the semiconductor sector, which accounts for US$20 billion in grants and subsidies in the 2020-2025 period.1 NVIDIA2 and Micron3 are establishing engineering centers of excellence in India, with plans to employ up to 10,000 workers. These investments by industry leaders are significant as they expand the high skilled employment base beyond India’s traditional strength in global capability centers and technology solutions consulting.

One of the focus areas for Prime Minister Modi in his third term will be to leverage India’s position in the diversification of global supply chains. India is already having significant success in capturing investments by multinational companies searching for an additional manufacturing base outside China. One of the key attractions for these companies is the huge pool of skilled workers with wage levels below those prevailing in China.

On infrastructure

The pace of public sector infrastructure spending in India is expected to slow. Relative to growth of 20%+ over the past three years, it is expected to decelerate to 12% in FY2025.4 However, as public sector spending slows, private sector infrastructure spending is expected to accelerate. The pickup in private sector spending will be facilitated by the significant improvement in cash flow amongst the top 150 companies in India. Pre-COVID, these companies were generating US$10 billion in free cash flow annually, this has accelerated to US$40 billion in FY24 as faster top line growth has contributed to an improving cash position.5

Public sector investment should continue to focus on transportation infrastructure, with the private sector likely to drive investments complementing the development of the manufacturing sector. This includes investment in factories, dormitories and renewable power.

On consumption

Analysis of the voting patterns in the recent election indicate the BJP did worse than expected in its share of the rural vote. This indicates there may be renewed focus on rural voters in Prime Minister Modi’s third term. Improved tax collection and expectations of a better FY25 fiscal position gives the government greater flexibility to increase spending in rural areas, including a focus on increase fiscal transfers. This is likely to benefit consumer discretionary and staples sector, which is a focus of our investments in India.

There is also the possibility of loan forgiveness for farmers, but given the fiscally conservative focus of the government, this is not expected to feature prominently. Nevertheless, public sector banks have come under selling pressure as investors fret over a potential increase in nonperforming assets. Our portfolio managers prefer private sector banks in India to mitigate against this risk.

The India election outcome is clearly a disappointment for investors relative to earlier expectations. Nevertheless, it is important to focus on the long term, and we do not anticipate significant policy changes in Modi’s likely third term. The drivers of India’s growth will remain centered on manufacturing, infrastructure and consumption.

Our on-the-ground presence with 15 investment professionals across three cities in India gives our local team clear insights into emerging trends. This is complemented by our global emerging market presence, comprised of 70+ investment professionals across 14 countries.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

__________

1. Source: “PLI CAPEX deployment expected to surge from FY24 for more than 80% of the projected investments.” ICRA, November 23, 2022.

2. Source: “Tata Partners with NVIDIA to Build Large-Scale AI Infrastructure.” NVIDIA. September 8, 2023.

3. Source: “Micron Announces New Semiconductor Assembly and Test Facility in India.” Micron. June 22, 2023

4. Source: Government of India. There is no assurance that any estimate, forecast or projection will be realized.

5. Source: FactSet. See www.franklintempletondatasources.com for additional data provider information.