Key points:

- As equity markets near all-time highs, a tension between momentum and contrarian indicators naturally arises. We find it important to examine these indicators to sharpen our tactical views.

- As equity overbought signals emerge, our optimism may be subdued, at least temporarily.

- We have reduced our equity preference and now have a neutral view between stocks and bonds. Our macro outlook remains constructive, and we would view a price correction in equities as an opportunity to become more bullish.

Equities near all-time highs

Equities are near cyclical highs once again. Is this a good thing or a bad thing for asset allocators? With stocks near cyclical highs, momentum is clearly supportive of risky assets, in our opinion. However, it feels as if a lot of the good news may be priced in, and contrarian indicators are suggesting allocators should be more cautious. Which perspective is better?

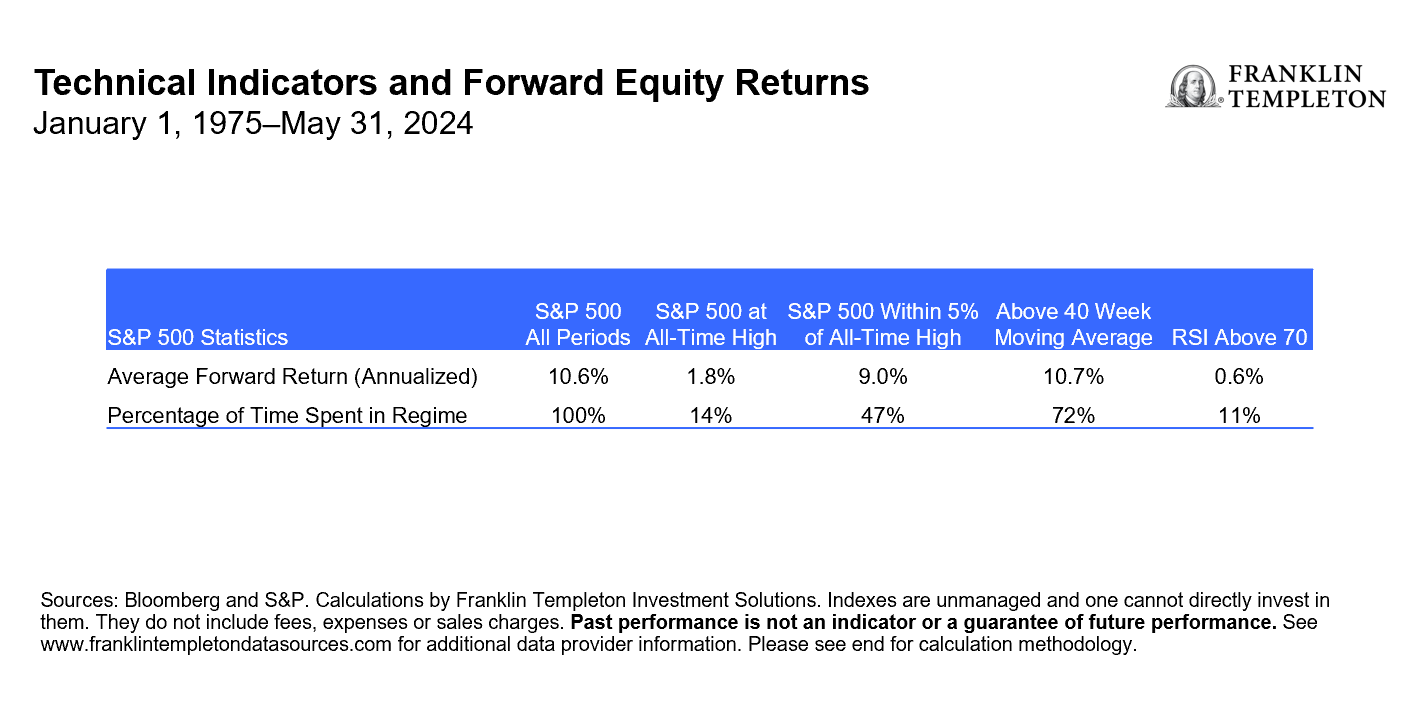

As usual, we turn to the data as our starting point in answering the above question. For starters, equities being at or near cyclical highs is not as rare of an occurrence as it may seem. Since 1973, equities have been at all-time highs 14% of the time.1 Additionally, they have been within 5% of all-time highs 46% of the time (see Exhibit 1).2

Although these parameters chart equities at similar points in time, we observe a significantly different path forward for returns. When equities are at all-time highs, we tend to see weaker forward equity returns. However, if we broaden the sample to consider all periods when equities are within 5% of all-time highs, then we see forward equity returns that are in line with the historical average.

We see similar results when examining technical indicators that measure investor sentiment. When the relative strength index (RSI) is above 70, that is commonly considered as signaling overbought conditions; weaker forward equity returns follow on average. However, if we zoom out and include all periods when equities remain above their 40-week moving average, then equity returns tend to be slightly better than historical averages (analogous to our previous example when equities are near, but not at, all-time highs).

Exhibit 1: Technical Indicators and Forward Equity Returns

How do we make sense of these mixed outcomes? In general, these results support the classic saying, “the trend is your friend.” As equities march higher, we want to acknowledge that the positive momentum has generally been a supportive factor for risk-taking. However, it also seems apparent that equities can get briefly overextended during bull markets, and we believe it can be advantageous to tactically reduce exposure when this happens.

As stocks recently approached all-time highs, we adjusted our risk-on stance; we now have a neutral preference between stocks and bonds. We remain constructive on the backdrop for equities, with a generally benign macro outlook and positive momentum in corporate fundamentals. However, sentiment metrics suggest equities may have limited upside in the near term. It can be smart to favor a more balanced (neutral) outlook between stocks and bonds when this occurs, looking to re-establish risky preferences should equities pull back, even moderately.

Exhibit 1 methodology

The statistics for this exhibit are calculated using weekly data, measuring the S&P 500 Price Index. Returns are calculated on a forward basis, measuring the forward weekly returns and annualizing the data for each regime.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Sources: Sources: Bloomberg and S&P. Calculations by Franklin Templeton Investment Solutions. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information..

2. Ibid.