Originally published in Stephen Dover’s LinkedIn Newsletter, Global Market Perspectives. Follow Stephen Dover on LinkedIn where he posts his thoughts and comments as well as his Global Market Perspectives newsletter.

Key takeaways

- Today, the more likely outcome of the November 2024 election appears to be divided government in Washington, DC, with no single party controlling the White House, the Senate and the House of Representatives.

- A divided government has been the norm for the past five decades, and one markets typically welcome, because gridlock decreases the scope for sweeping legislative change. However, divided government could increase US sovereign default risk if one branch of Congress refuses to lift the debt ceiling.

- Broad market returns will not depend on who becomes president, but the outcome will be significant for specific sectors such as energy or pharmaceuticals.

Here we go

With less than two months until US election day, we are in the final stretch of the race.

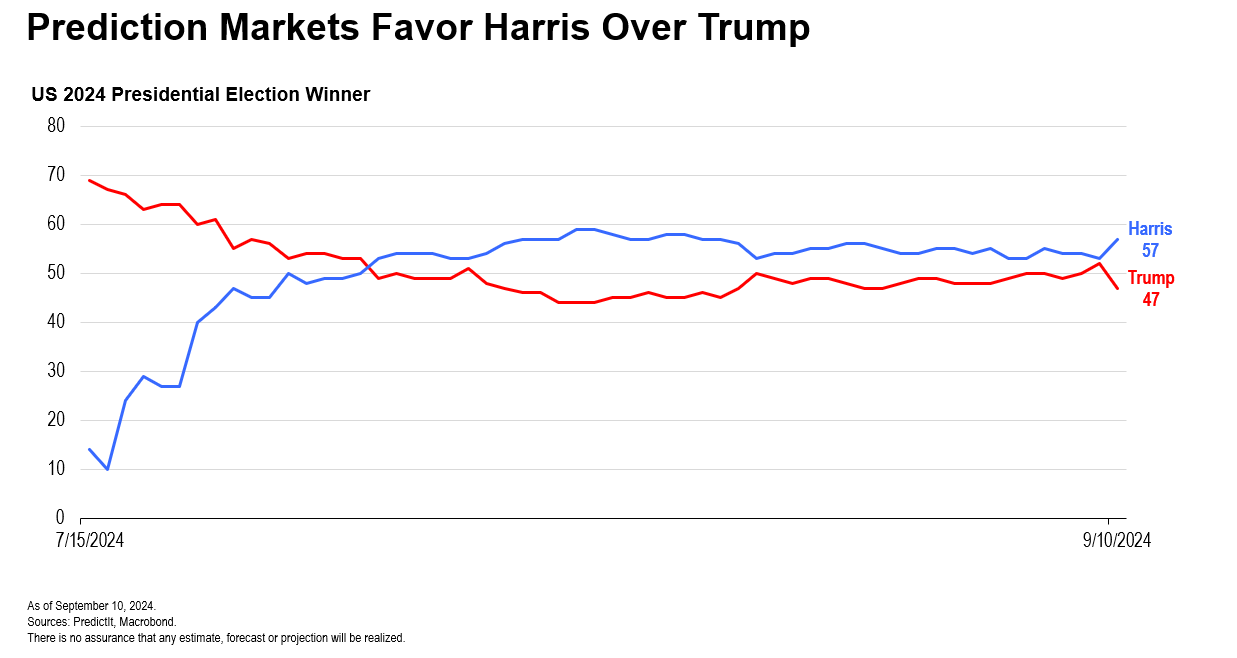

Over the past two months, the US presidential election dynamics, as well as the outcomes for control of the US Senate and House of Representatives, have shifted significantly. The July 21 decision by President Joe Biden to withdraw his candidacy in favor of Vice President Kamala Harris changed the trajectory of the presidential race. Polls have indicated tighter races across all levels of elected government. Initial polling and moves in political futures markets indicate that Vice President Harris “won” the September 10 debate against former President Trump, but it remains premature to know whether the result was enough to firmly entrench her as the frontrunner.

For investors and market returns, however, politics can be overrated. Despite shifts in polls and other indicators, our primary investment conclusion remains unchanged. Investors should stay focused on long-term objectives and not overreact to US politics and election outcomes. As we have noted in earlier research, markets have thrived, paused, corrected and rebounded under both Republican and Democratic presidencies, as well as under various constellations of power in Congress. The broad contours of the stock, bond and even currency returns are typically dictated by fundamentals determined outside the sphere of politics.

That does not mean, however, that specific sectors, such as energy or pharmaceuticals, won’t be impacted by the outcome of the election. In that regard, some portfolio implications are worth considering, as we detail below.

The odds have shifted

Across almost every metric—national polls, “battleground state” polls, political futures markets, and spread-betting—the data tell a consistent story of an election up for grabs. That is in marked contrast to just a few months ago, when most indicators showed former President Trump with a clear lead, and with Republicans enjoying the inside track for control of both houses of Congress. In June, therefore, we explored the implications for investors of a Republican clean sweep.

Today, that outcome seems far less likely. National and key swing state polls show the presidential race a dead statistical heat, with Vice President Harris enjoying small leads in most swing states and nationally. Majority outcomes in the Senate and House of Representatives are also tougher to predict, with Republicans enjoying a slight advantage in the Senate, while the Democrats have better chances of having a majority in the House.1

The probabilities have therefore shifted toward divided government in Washington, where one party controls the White House and the other has a majority in one or both chambers of Congress.

Divided government is not novel in recent US history, including recent US history. Since 1968, for example, a form of divided government has existed in 38 of 56 years (68% of the time).2

Broad market implications

The sharp shift in the polls over the past two months is a reminder that a lot can still change. Relatively few voters may remain undecided, but US elections—at all levels—are often decided by swings in relatively few votes in just a few states. For example, the outcomes of the 2016 and 2020 presidential elections hinged on less than a million votes cast in six key swing states, out of a total of about 150 million total votes cast nationwide. US politics has been, and remains, closely divided. It is therefore still too soon to draw firm conclusions regarding the outcome in political or market terms.

Nevertheless, it is worth briefly considering what divided government might mean for investment risk and returns.

Investors often welcome a divided government because, perhaps perversely, it diminishes uncertainty. The scope for sweeping legislative changes to tax laws or regulatory policy is constrained by the need for compromise. The status quo persists, allowing firms and investors to make decisions without having to consider major fiscal or regulatory policy shifts.

Divided government can even permit deficit reduction, as occurred from 1994-2000 and again from 2010-2016. Bond investors, therefore, may have grounds for welcoming it as an avenue to reduce deficit and debt burdens.

The one area of potential concern under divided government, however, resides in political default risk. Government shutdowns and the potential for the Treasury to miss interest payments on the national debt have been a concern when impasses led to an inability to increase the US debt ceiling. In all such cases since the mid-1990s, those near misses (but including US debt downgrades by ratings agencies) have occurred with a Democrat in the White House and a Republican majority in the House of Representatives. Democrats, thus far, have not engaged in similar political negotiating tactics under circumstances where they controlled the House of Representatives under a Republican president. The implication is that default risk would be higher in divided government with Harris as president.

Market implications of a divided government

The primary driver of returns in US Treasuries and the overall direction of interest rates will be determined by the business cycle (growth and inflation) and corresponding Federal Reserve (Fed) policy, not by fiscal policy or sovereign risk premiums. No matter the legitimacy of long-term concerns about US government deficit and debt trajectories, there is no evidence that the current size of the debt or even its projected growth is or will soon have significant near- or medium-term impacts on the level or directional moves of the US Treasury market.

For equities, valuations and profits determine returns. Raising the corporate income-tax rate (Harris favors raising it from 21% to 28%) would lower after-tax corporate profits, but as president she may struggle to enact any increase if Republicans control the Senate.

The more important consideration for equity investors is regulatory action, which resides chiefly with the president. Harris and the Democrats are apt to push for greater regulation of fossil fuel energy and the pharmaceutical industry (e.g., further caps on prescription drug pricing), while promoting alternative energy. The opposite would be true in a Trump presidency. Accordingly, we think those sectors are likely to react more to the presidential outcome than the broader market.

In foreign exchange markets, the dollar will adjust to changes in interest differentials and expected equity return differentials between the United States and other countries. With US growth showing signs of slowing and the Fed indicating significant easing over the next 12 months, the dollar is apt to depreciate somewhat against other major currencies. But in our view, dollar weakness is likely to be contained by weak growth and relatively poor returns in fixed income and equity markets in Europe and Asia, as economies in those regions remain hamstrung by weak global growth, tepid world trade growth, and other factors, such as political risk or heavy debt burdens (e.g., China).

The wildcard for the dollar and capital markets would be a Trump victory followed by the imposition of large, across-the-board tariffs. If countered by other countries, the risk of trade wars could push up risk premiums, leading to sharp falls in equity markets and a surge into traditional safe-haven currencies (Swiss franc, Japanese yen), or gold and cryptocurrencies.

Finally, anti-trust policy is worth watching. The Biden Administration has taken a tougher stance against large capitalization technology companies, led by Federal Trade Commission Chairperson Lina Khan. A Harris administration could also pursue that approach. On the other side, Republican Vice-Presidential candidate JD Vance is an advocate of anti-trust with respect to the technology sector. In both cases, anti-trust captures populist sentiment that ordinary Americans are concerned about the growing power of large firms.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Focusing investments in the health care, information technology (IT) and/or technology-related industries carries much greater risks of adverse developments and price movements in such industries than a strategy that invests in a wider variety of industries. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principle investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Trust Management Co., Ltd., 3rd fl., CCMM Building, 12 Youido-Dong, Youngdungpo-Gu, Seoul, Korea 150-968. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

__________________

1. According to the University of Iowa political futures markets, for example, Republicans have a 65% chance of regaining majority control of the US Senate, while Democrats have a 70% chance of wresting majority control of the House of Representatives. For details, see: https://apps.biz.uiowa.edu/IEMOffice/chart/market/House24

2. Source: Amercianacorner.com. There is no assurance that any estimate, forecast or projection will be realized.