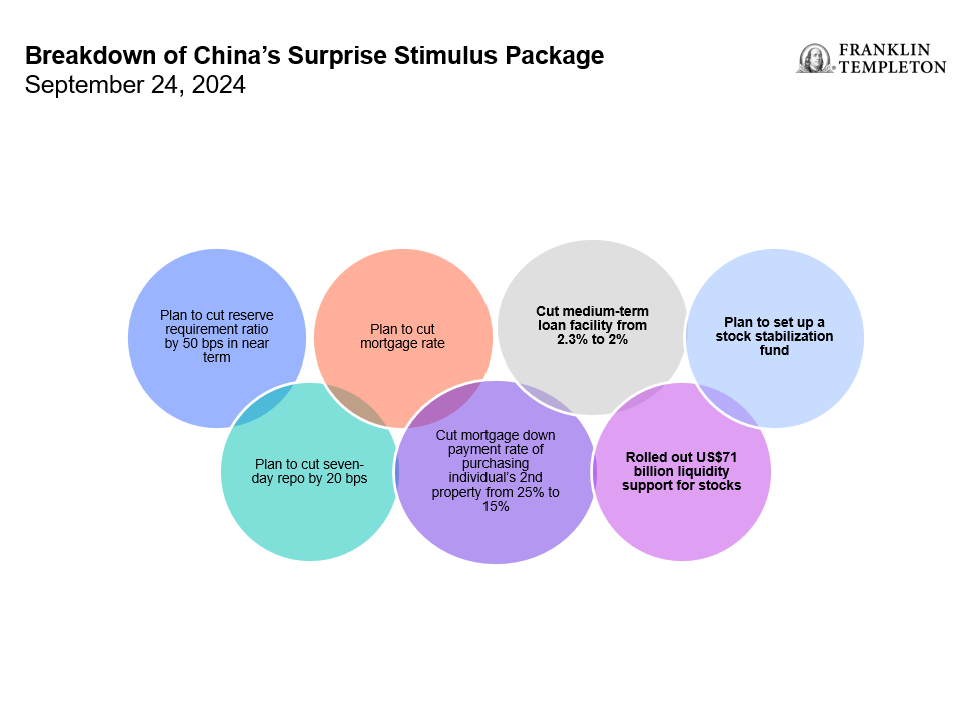

China’s broader-than-expected stimulus package has provided a large jolt, buoying investor confidence in its battered economy. The recently announced measures, including new tools for China’s central bank to help firms buy back shares via refinanced bank loans, prompted investors to rush into China stocks on the last Friday of September. Shares on the Shanghai Stock Exchange soared with turnover reaching US$101 billion in the first hour of trading.1 The exchange was initially plagued with glitches in processing orders and delays ahead of the last day of September when China stocks eventually rose to see their best day in 16 years.2

With China’s new policy-rate cuts, we now see the world’s second-largest economy potentially embarking on a more focused path of economic revival. Renewed efforts in China aim to help securities companies, insurers and other institutional investors raise funds by enhancing their balance sheets. We view the immediate market response to such moves as a strong indicator, not only of investor appetite for value, but also a “fear of missing out” sentiment that we believe may drive the market rally higher. Short covering3 likely also played a role. Traders that suffered heavy losses may not be willing or able to bet against the government again any time soon, which could add stability to the latest rally, in our opinion. Even so, given that China’s weak domestic consumption, troubled housing sector and other structural issues may continue to weigh on the economy, quick fixes seem unrealistic. However, the signal these measures have sent to the market appears stronger than at any time in at least three years and have planted the seeds for an improving perception of China’s equity market.

Exhibit 1: Breakdown of the Surprise Package

External geopolitical risks continue to pose prevailing uncertainty, especially as we count down to the US presidential election. Also, chatter over the potential for a US-China trade war endures. Analysts continue to debate the implications of a Kamala Harris presidency versus a second Donald Trump term in the White House. Current US election polls still reveal a tight race across many levels of elected government. Investors may be able to take some comfort from the likelihood that the United States may continue to experience a divided Congress—the norm for the past several decades—as this can minimize sweeping legislative change.

All this is not to say that we aren’t encouraged by the recent grit displayed by China’s leaders in their urgency to stabilize markets. In fact, the moves have already led emerging market stocks to rise to highs not seen in more than two years.4 Equity markets of Brazil and South Korea, which both hit year-to-date lows in August, have since been lifted higher.5 The same is true for Mexico’s market, which saw its stocks advance after slumping in early September.6

However, this may serve as a reminder of the case for long-term global market opportunities.

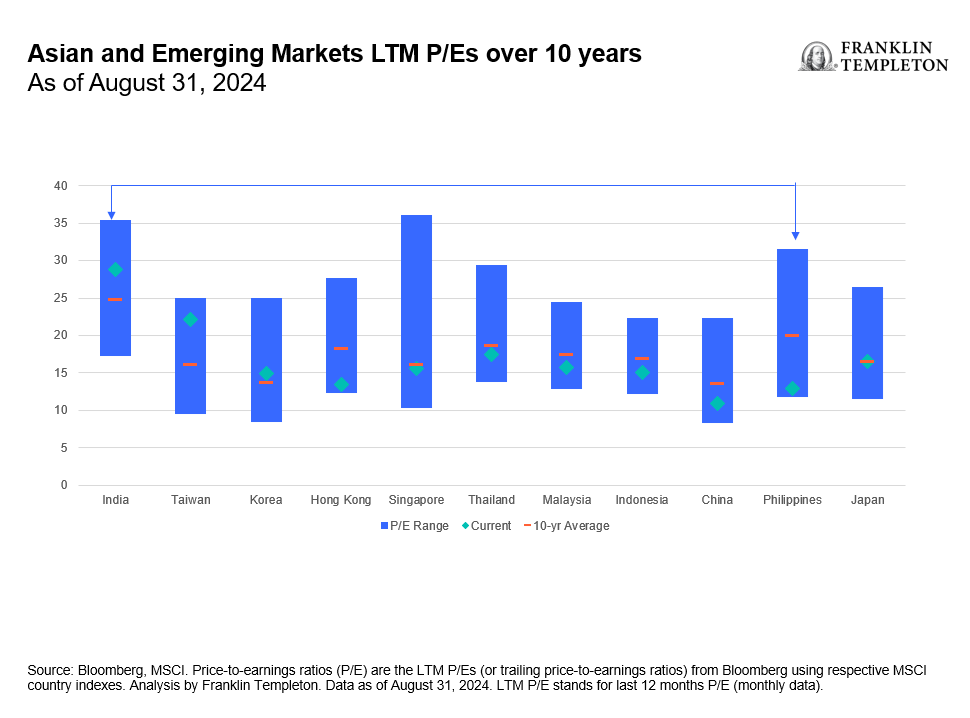

Exhibit 2: Asian and Emerging Markets: A Diverse Bunch

While the market’s focus this week may be on China—and the long-term case for an allocation in Chinese equities has likely improved with the latest announcements—we cannot stress enough the importance of diversification. Asian and emerging markets have increasingly shown bifurcation, and we expect this trend to continue. The global interest-rate cycle, the US election and geopolitical fragmentation are all questions that add layers of complexity. We think investors should prioritize flexibility and nimbleness in this economic climate. Low-cost exchange-traded funds can be a good vehicle with a growing lineup of single-country and regional strategies available.

South Korea

In our view, South Korean valuations coupled with improving corporate governance and a push for shareholder value make for a strong foundation and could potentially offer a risk cushion. The AI business ecosystem, including semiconductors, certainly remains as a key growth driver. In 2023, the AI market in South Korea was valued at US$2.4 billion, and is projected to grow to US$28.2 billion by 2032.7 Although the country lags slightly behind Taiwan in the manufacturing of cutting-edge chips—and the consumer electronics focus has been a drag compared to Taiwan’s more pure-play approach—this should now be largely reflected in valuations, in our analysis. If global growth holds up, we think South Korea could become a compelling turnaround story.

Japan

The forward price-to-earnings multiple for Japan’s market currently sits at about the same level as its 10-year average of 16x.8 However, structural changes are firmly underway, including corporate reforms and more government incentives driving money into Japanese stocks.

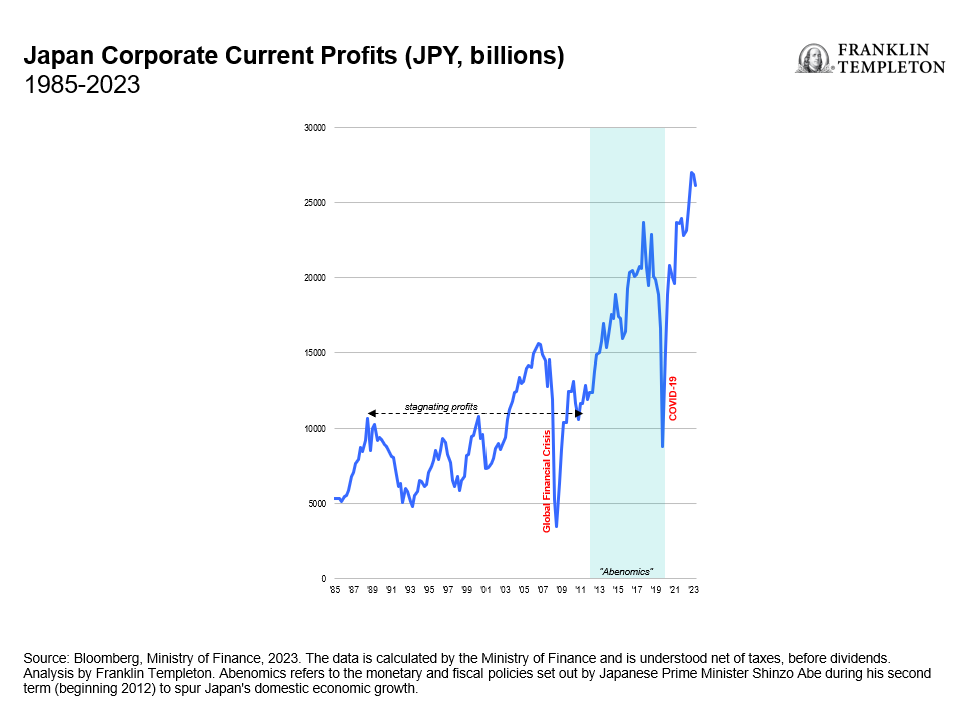

Exhibit 3: Japan Corporate Current Profits

In 2023, the Tokyo Stock Exchange initiated measures that require listed companies to focus on their price-to-book ratios. Rising corporate profits—helped by higher, but still moderate inflation—may allow for large share buyback programs and more attractive dividend policies. We expect that 2024 should see a record in share buybacks, already up 60% at mid-year.9 International activist investors have begun to take notice and are increasing their exposure to the country. This should put further pressure on companies to improve shareholder value.

Conclusion

We think China’s concerted comeback efforts in global markets is a positive signal for the country and the wider region. In our opinion, long-term trends like technological leadership, attractive valuations and the leveling up of manufacturing capabilities offer ample opportunities for investors along the risk spectrum. The path forward will not be smooth sailing, but we believe the biggest risk for investors could indeed be to sideline these markets in their allocation decisions.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

There are special risks associated with investments in China, Hong Kong and Taiwan, including less liquidity, expropriation, confiscatory taxation, international trade tensions, nationalization, and exchange control regulations and rapid inflation, all of which can negatively impact the fund. Investments in Hong Kong and Taiwan could be adversely affected by its political and economic relationship with China.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Trust Management Co., Ltd., 3rd fl., CCMM Building, 12 Youido-Dong, Youngdungpo-Gu, Seoul, Korea 150-968. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: Bloomberg, September 27, 2024.

2. Source: Bloomberg, September 30, 2024. The Shanghai Stock Exchange Composite Index, also known as the SSE Index, is a stock market index of all stocks that are traded at the Shanghai Stock Exchange. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

3. Short covering refers to buying back borrowed securities in order to close out an open short position at a profit or loss.

4. Source: Bloomberg, September 25, 2024. The FTSE Emerging Index is an international equity index, which tracks stocks from emerging markets worldwide. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

5. Ibid.

6. Ibid.

7. Source: IMARC Group.

8. Source: Bloomberg, MSCI, analysis by Franklin Templeton, as of August 2024.

9. Source: “Japan stock buybacks hit $57bn, speeding toward annual record.” NikkeiAsia. June 12, 2024.