For many people, Brazil’s Rio de Janeiro evokes images of sunny beaches and colorful celebrations. But the city’s biggest international event of this year (in fact, the largest since the 2016 Olympic Games) will likely involve more suits than bikinis. Next month, for the first time, Brazil will take center stage on the world’s preeminent platform for global economic cooperation as host of the G20 (Group of 20) Summit in Rio.

The coalition, which includes the United States, China, India, the European Union, and most recently, the African Union, represents the world’s major economies—accounting for roughly 80% of global gross domestic product (GDP), 75% of global trade and two-thirds of the global population.1

Since taking office early last year for his third non-consecutive term, Brazilian President Luiz Inácio Lula da Silva’s (Lula) has spent much time abroad trying to raise his country’s global standing. His efforts may be paying off. A recent Pew Research survey found that most Brazilian adults are optimistic about their country’s status as an international power.2

Beyond the G20, Brazil is also slated to play host for other high-profile events, such as the UN Climate Change Conference (COP30) and the BRICS (Brazil, Russia, India, China and South Africa) summit in 2025, while concurrently pursuing membership in the Organisation for Economic Co-operation and Development (OECD).

In the nearly three years since Brazil began its formal accession process for OECD membership, it has reached many milestones toward this goal. If it succeeds in being admitted, Brazil would be in a unique position to influence increasing geopolitical and economic competition between developed and developing countries as the only nation to simultaneously straddle BRICS, the G20 and the OECD.

As the world’s eighth-largest economy and the biggest one in Latin America, Brazil could be a strong link in global discourse over key issues for the Global South:3 fighting hunger, poverty and inequality; sustainable development; and global governance reform. If Brazil can galvanize political and financial commitments toward advancements for priorities, such as digital infrastructure, that could be a boon toward not only raising Brazil’s GDP but also reducing its economic, urban-rural and gender divides. Consider that the implementation of a relatively new central bank-led instant payment platform, known as Pix, has already bolstered financial inclusion, raising access to banking services from around 70% to more than 84%.4

We believe an OECD stamp of approval would also encourage global investors who seek the assurance of the coalition’s high standards for ease of doing business. Having a seat at the table would give Brazil a stronger voice in shaping best practices and global frameworks over quickly evolving technology standards. The country’s artificial intelligence and fintech firms are already among the largest in South America.

Resource-rich Brazil is a leader in the energy sector as the largest oil5 producer for Latin America, and one of the world’s top 10 producers (at the end of 2023, it comprised 4% of total world oil production).6 But its largest sector, with more than a 36% weighting, is financials.7

Areas of concern and opportunity

High government expenditures remain an area of key concern, but we believe any restraints on that would bring optimism to its capital markets. Brazil is also an outlier in the global trend of easing rates as its central bank raised interest rates in September in a bid to contain inflationary pressures. The Brazilian real is expected to remain stable or strengthen somewhat over the near term, owing in part to declining US interest rates, and we see this as a potential benefit to foreign investors to Brazil.

We are encouraged by recent progress in Brazil’s long-awaited value-added tax (VAT) reform, which could provide a tailwind to the private sector as efficiency gains from a simpler tax system could favor investment.

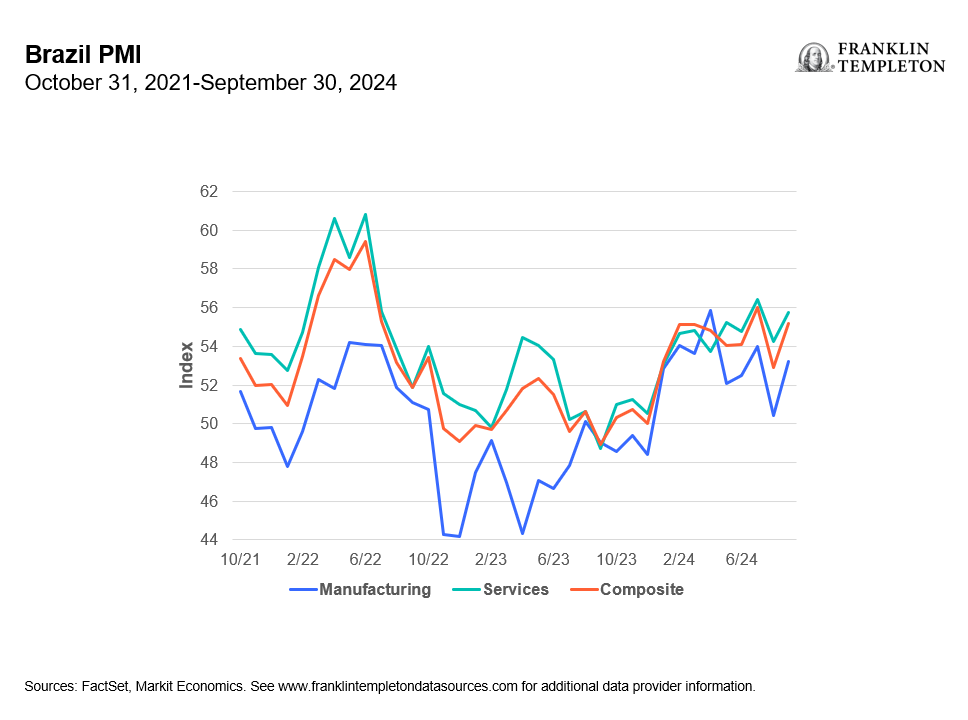

Brazil’s manufacturing and services expansion increased faster in September with output up for both, indicating strong growth in business activity. In addition, its market currently trades at what we consider to be discounted valuations. Improved manufacturing conditions in Brazil were driven by a renewed increase in production, stronger job creation and a pickup in sales growth, according to S&P Global.8 Outpaced by only India at the end of September, Brazil’s Manufacturing PMI increased to 53.2 (from 50.4 in August; readings above 50 indicate expansion).

Exhibit 1: Brazil’s Purchasing Managers’ Index

Expectations are also high for Brazil to receive an economic boost in 2027 given its historic winning bid to host the FIFA Women’s World Cup, a first not only for Brazil, but for all of South America. And at which point, Rio should expect fewer suits and more face paint as a host city.

Over the near term, we believe investors should stay attuned to the opportunities in Brazil and may find what we consider an attractive entry point into this large and diverse market.

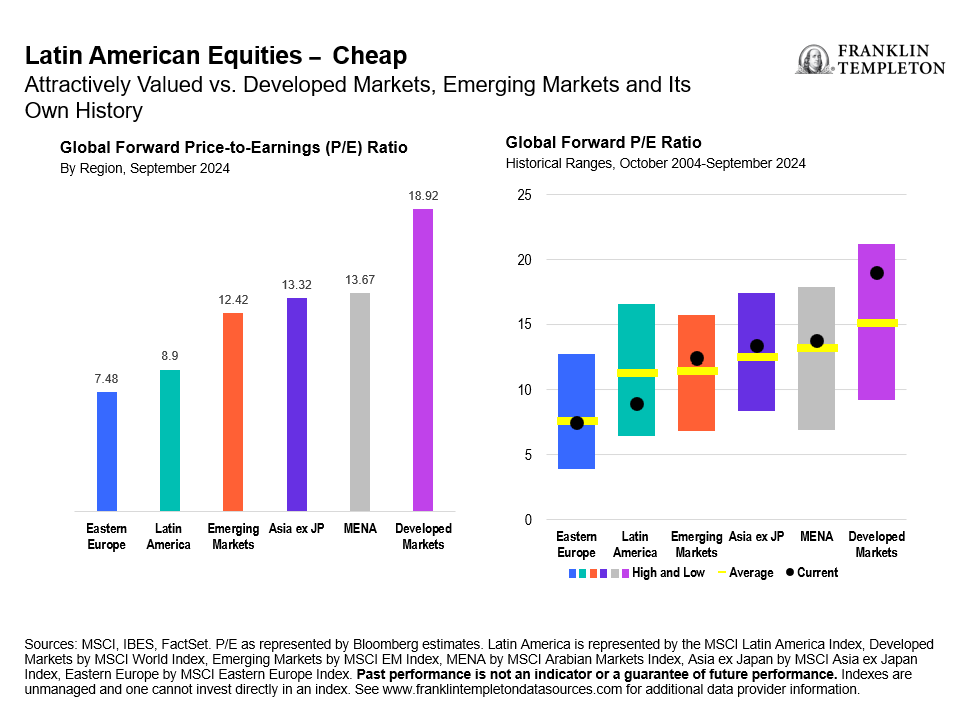

Exhibit 2: Latin American Equities Look Cheap

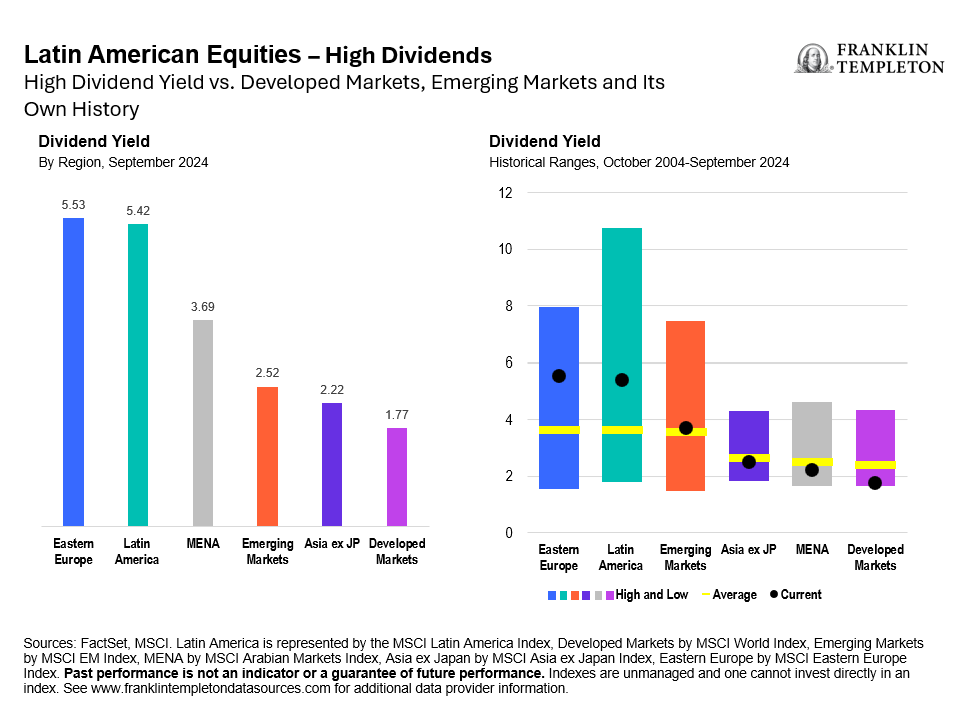

Exhibit 3: Latin American Equities Offer High Dividends

Index definitions

The MSCI AC Asia ex Japan Index captures large- and mid-cap representation across two of three developed market (DM) countries (excluding Japan) and eight emerging market (EM) countries in Asia. With 1,070 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Arabian Markets Index captures large- and mid-cap representation across 11 Arab Markets countries. With 132 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Eastern Europe Index captures large- and mid-cap representation across three EM countries in Eastern Europe. With 20 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 EM countries. With 1,277 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Latin America Index captures large- and mid-cap representation across five EM countries in Latin America. With 94 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI World Index captures large- and mid-cap representation across 23 DM countries. With 1,410 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Equity securities are subject to price fluctuation and possible loss of principal. Dividends may fluctuate and are not guaranteed, and a company may reduce or eliminate its dividend at any time.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

To the extent the portfolio invests in a concentration of certain securities, regions or industries, it is subject to increased volatility. Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Trust Management Co., Ltd., 3rd fl., CCMM Building, 12 Youido-Dong, Youngdungpo-Gu, Seoul, Korea 150-968. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1.Source: “OECD and G20.” OECD.

2. Source: “Brazilians Mostly Optimistic About Country’s Global Standing Ahead of G20 Summit.” Pew Research Center. September 23, 2024.

3. According to UN Trade and Development, the Global South broadly comprises Africa, Latin America and the Caribbean, Asia excluding Israel, Japan, and South Korea, and Oceania excluding Australia and New Zealand

4. Source: “Brazil’s Bridges to the Future: How the Country Is Building Digital Infrastructure.” Carnegie Endowment for International Peace. November 15, 2023.

5. Oil includes crude oil, all other petroleum liquids, and biofuels.

6. Source: U.S. Energy Information Administration, International Energy Statistics, total oil (petroleum and other liquids) production, as of April 11, 2024. Production includes domestic production of crude oil, all other petroleum liquids, and biofuels and refinery processing gain.

7. Source: MSCI Brazil Index (USD). As of September 30, 2024.

8. Source: “S&P Global Brazil Manufacturing PMI.” S&P Global. October 1, 2024.