Key takeaways

Today’s investors would be wise to consider the role dividends can play in their portfolio, including:

- Significant contribution to total return

- Potential to lower volatility

- Correlation to high-quality businesses

- A broader opportunity set of dividend-paying stocks

Why consider dividends?

As an equity income portfolio manager, I am stalwart in my belief that investing in high- quality companies with the potential to grow over time while generating income can be an excellent source of total return and even more attractive risk-adjusted returns. Today’s environment presents investors with considerable economic uncertainty and meaningful geopolitical tensions around the globe. And with rates on fixed income alternatives heading lower, the value proposition of dividend income looks especially compelling for four key reasons.

1. Dividends play a significant role in total return

Many investors underestimate the impact of dividends on total returns. Since 1926, dividends have contributed nearly one-third of total equity return for US stocks.1 From 1980 to 2019, a period characterized by a significant decline in interest rates, 75% of the returns of the S&P 500 Index came from dividends.2

Dividends can be particularly important in a declining interest-rate environment, providing a reliable source of cash flow when other fixed income options are less lucrative. Companies rarely stop paying dividends once they initiate them, and most tend to increase the amount of their dividends over time. Paying a dividend can also make a stock more attractive to investors, potentially increasing its value.

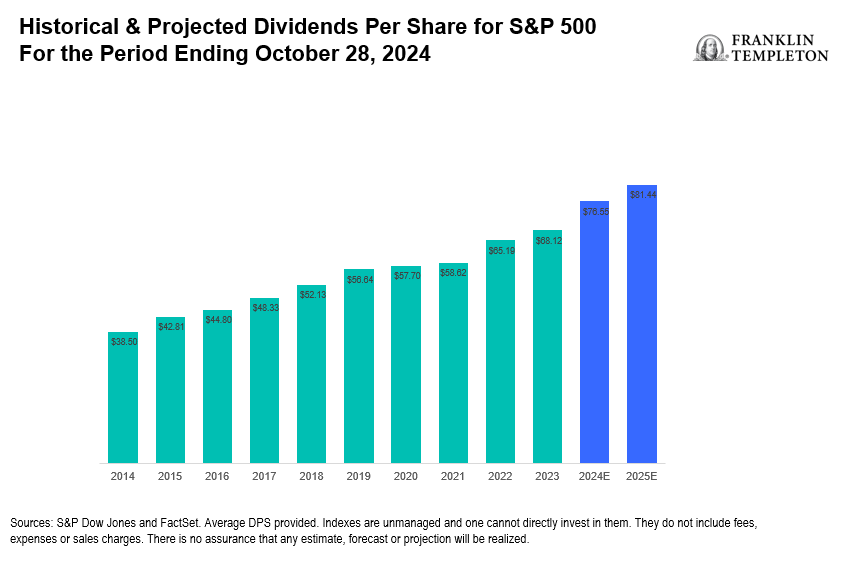

Over the past 10 years, dividends for the S&P 500 Index have grown each year and at an average compound rate of just over 7% annually.3 In strong markets, dividends have added to total return. In years when returns were low or negative, like in 2020 and 2022, dividends comprised a larger contribution of total return and helped provide portfolio resilience.

Exhibit 1: Dividends Are Growing

2. Dividends can reduce volatility

Dividends can play a significant role in reducing overall portfolio volatility and can potentially help mitigate losses from a decline in stock price. Studies have also shown that historically, dividend-paying stocks often outperform non-dividend-paying stocks during bear market periods, including the bursting of the tech bubble in the early 2000s and during the global financial crisis.4This may be in part because dividend-payers tend to be larger, more established and profitable companies than represented by the broader market, and these businesses are often more resilient.

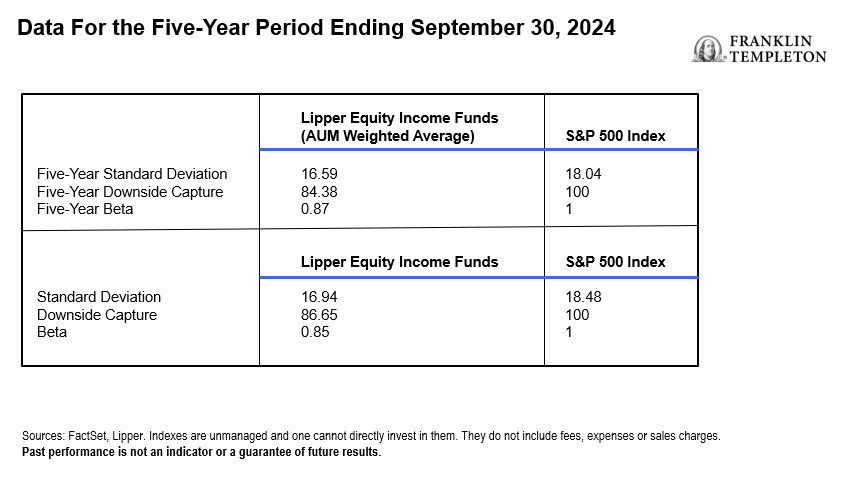

Over the five years ending September 30,2024, a period that saw wide swings in overall total performance of the S&P 500, equity income funds were less volatile and had lower downside capture than the broader market.5

Exhibit 2: Equity Income Strategies Can Be Less Volatile

3. Dividends correlate to high-quality businesses

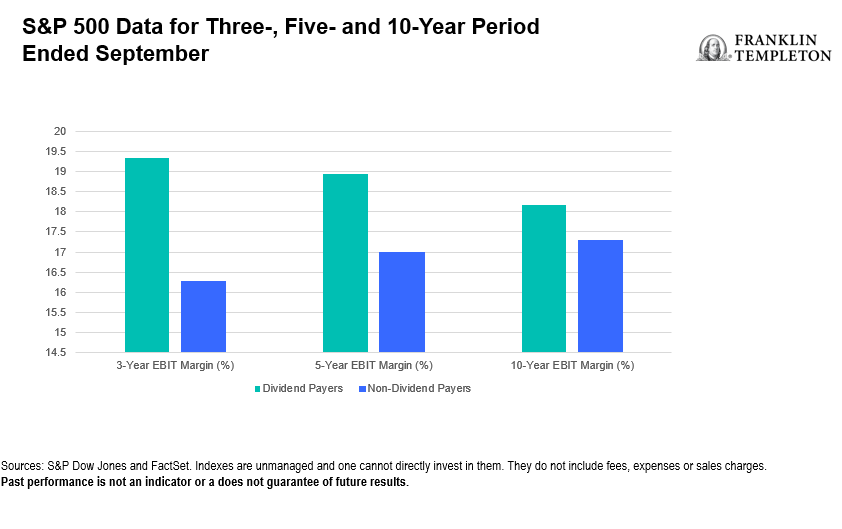

Since investors typically consider dividends an ongoing commitment, dividend payments require a level of profitability, returns and consistency of cash flow generation. This makes them a meaningful metric to assess business quality. Companies that consistently increase their dividend payments over time demonstrate that their business is steadily generating profits and may be more resilient during market or economic downturns. The chart below shows that dividend-payers within the S&P 500 Index have historically been more profitable than their non-dividend paying peers.6

Exhibit 3: Dividend-Payers Can Be More Profitable than Non-Dividend Paying Peers

4. More “growth” stocks are paying dividends

As of September 30, 2024, about 80% of companies in the S&P 500 Index paid a dividend, a number reasonably consistent with the same metric a decade earlier.7 However, in 2024, nearly 24% of those companies were in the technology sector—up from 13% a decade ago.8 Innovative sectors like health care and industrials also saw meaningful increases among dividend-payers.

Broader payment of dividends has expanded the investable universe, providing equity income investors greater access to higher-growth, dynamic and innovative companies. For example, in recent periods, market-leading companies such as Alphabet, Salesforce and Meta Platforms have all initiated a dividend.9 Other established IT leaders, such as Microsoft, Oracle and Broadcom, have shown that paying a dividend does not hinder innovation and reinvestment into new product opportunities. Companies can do both.

Conclusion

An equity income strategy may be an attractive investment vehicle for those seeking a potentially less risky and less volatile way to invest in equities while generating income. The margin and return profiles of many dividend paying stocks are attractive, and we believe that strategies that focus on investing in innovative companies that effectively allocate capital to fund future growth while paying a growing dividend offer investors a compelling opportunity.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Diversification does not guarantee a profit or protect against a loss.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested.

Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the US, this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. US: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg – Tel: +352-46 66 67-1, Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorized Financial Services Provider. Tel: +27 (21) 831 7400, Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100, Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Trust Management Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The views and opinions expressed are not necessarily those of the broker/dealer; or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent any broker/dealer policies, procedures, rules, and guidelines.

Copyright © 2024 Franklin Templeton. All rights reserved.

__________________

1. Source: Standard and Poor’s. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results.

2. Source: Standard and Poor’s.

3. Source: Standard and Poor’s, Dow Jones and FactSet.

4. Source: FactSet and Lipper.

5. Source: Lipper and FactSet.

6. Source: Standard and Poor’s.

7. Ibid.

8. Ibid.

9. Source: Bloomberg.