As China braces for renewed friction over President-elect Donald Trump’s tariff threats, investor flows may be following similar currents as those of regional supply chain shifts—that is to say, diversifying from China and toward opportunities in markets such as India and Japan.

After the People’s Bank of China revealed the most aggressive stimulus package it’s rolled out since the COVID-19 pandemic, China stock markets saw a short-lived rally at the end of September. A lack of detailed measures targeting consumption seems to have disappointed investors and led the bullish sentiment to deflate.

Adding to the country’s economic woes are societal changes like falling birthrates and a rapidly ageing population. Estimates by China’s National Health Commission suggest the country’s elderly population will grow to over 400 million by about 2035. To better cope with this crisis, China’s statutory retirement age will be extended, starting in January 2025, for the first time since the 1950s.

India investors, meanwhile, are finding the subcontinent—which has already overtaken China as the world’s most populous nation—appealing for its relative immunity to global risks, given its domestic-driven economy. Its younger labor force has also attracted a market pivot to this prime alternative to China manufacturing. For the 12-month period prior to China’s September 2024 stimulus announcement, US-listed India equity exchange traded funds (ETFs) garnered US$7.5 billion in flows—a sharp contrast to the US$6 billion in outflows experienced by China ETFs over the same period.1

Judging by India’s impressive initial public offering (IPO) environment, businesses there are feeling the optimism. The country’s 258 IPOs accounted for 30% of the global total by number by the end of September and 12% by the amount of money raised, in an economy that makes up just over 3% of global GDP.2

And investors in India are taking note. Aided by the improving digitalization of finance and increased internet access, India’s middle class is also an expanding retail investor class. By one measure, nationwide stock trading accounts nearly tripled from 2019 to 2023 to roughly 140 million.3

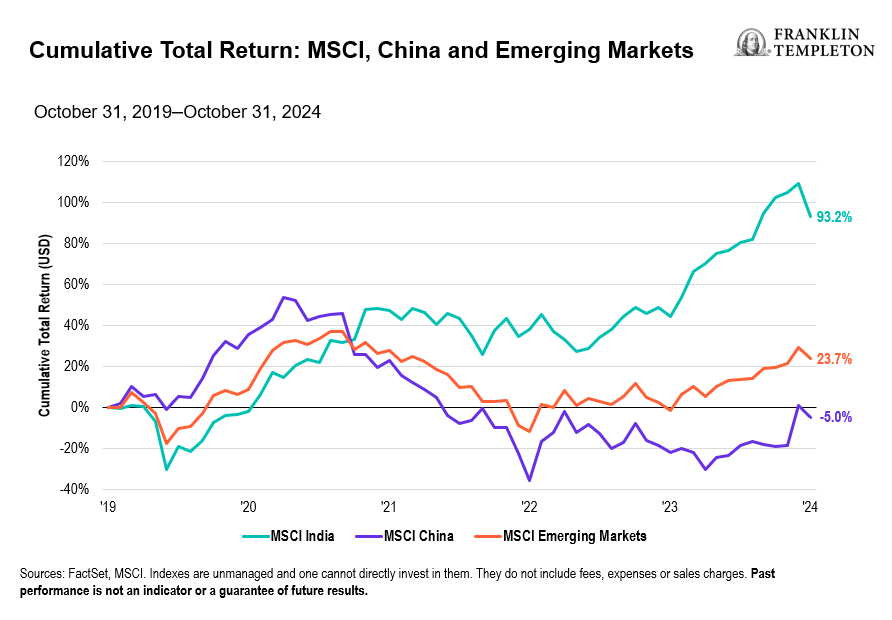

In dollar terms, total returns for Indian stocks have risen by 93% over the past five years, compared with about a 24% rise overall for emerging markets and drop of 5% for China stocks over the same period.4

Many investors seeking to better diversify emerging market exposure or layer in targeted broad country allocation can tap single-country exchange-traded strategies.

Emerging markets in the Asia region are not the only beneficiaries of a potential US-China trade war. Earlier this year, investors were already driving up flows into Japan ETFs. Market watchers consider Japanese stocks to be indirect beneficiaries of Trump’s reflationary economic policy—which may keep interest rates high, thereby boosting the dollar and weakening the yen to the advantage of Japanese exporters.

The MSCI Japan Index is up nearly 21% in US dollar terms in the one-year period ending October 31, 2024. Consumer discretionary, financials and industrials holdings led gains during this time.

An element of uncertainty around the policies of a second Trump term, however, are still causing jitters around Asia, especially given the president-elect’s transactional approach to international relations.

Fortunately, Japan is seeing a renaissance in its semiconductor industry for which Tokyo is investing heavily (more than US$25 billion through 2025) and has established strong multilateral trade partnerships.

Japan has already elevated its role in global supply chain reorganization in recent years, and seeks to take advantage of its clout in joint free trade initiatives, such as the US’s Indo-Pacific Economic Framework for Prosperity to strengthen its regional supply-chain leadership.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

There are special risks associated with investments in China, Hong Kong and Taiwan, including less liquidity, expropriation, confiscatory taxation, international trade tensions, nationalization, and exchange control regulations and rapid inflation, all of which can negatively impact an investment. Investments in Hong Kong and Taiwan could be adversely affected by its political and economic relationship with China.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, http://www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

___________________

1. Source: Morningstar Direct. This figure excludes funds from Hong Kong and

2. Source: “India is undergoing an astonishing stock market revolution.” The Economist. November 7, 2024.

3. Source: “Why are so many Indians piling into stocks.” The Economist. March 7, 2024.

4. Sources: FactSet, MSCI. As of October 31, 2024. The MSCI India Index is designed to measure the performance of the large- and mid-cap segments of the Indian market. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging markets (EM) countries. The MSCI China Index captures large- and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs). Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.