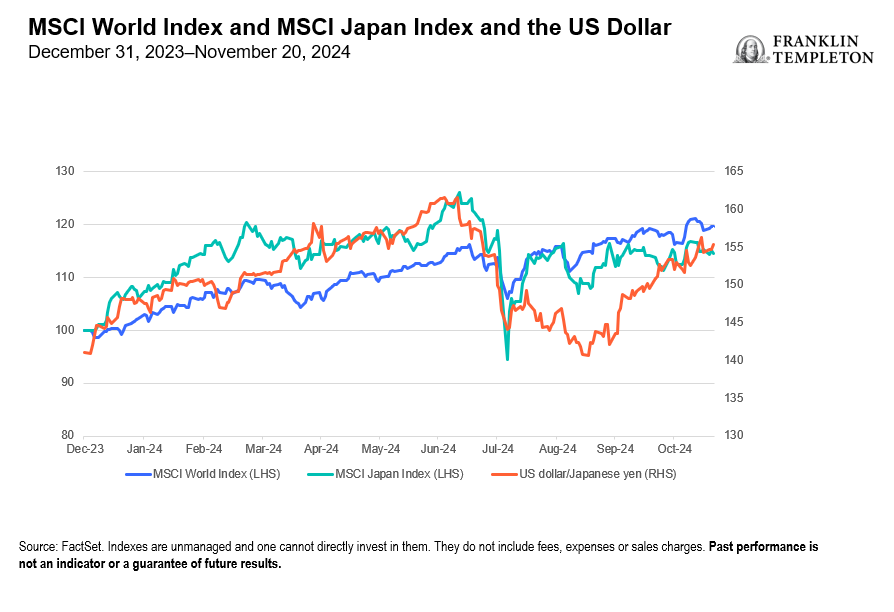

After outperforming in the first half of 2024, Japanese stocks have had a few volatile months. First, growing worries in July about a global economic slowdown pressured Japanese stocks. A “shock” market event followed in which the “yen carry trade”—when one borrows in yen at low interest rates to fund investments in a higher interest rate currency—abruptly unwound, sending Japanese stocks cratering overnight. Stocks rebounded quickly only to see another round of uncertainty creep in as a change in Japan’s political leadership led to questions about the country’s fiscal and monetary policy. The snap parliamentary elections and the losses for the ruling Liberal Democratic Party (LDP) party in late October introduced new potential worries. (See Exhibit 1.)

While short-term moves like these can be unnerving, over the longer term, we continue to believe there is value to uncover across the Japanese stock market as inflation returns, real wages inflect and rise, and corporate governance reforms progress, driven by the Tokyo Stock Exchange’s (TSE’s) push for companies to get their book values above one.

Exhibit 1: MSCI Japan Outperformance Has Faltered

Changing political leadership

After Shigera Ishiba became LDP leader in late September and prime minister at the start of October, a snap election in late October cost the LDP its parliamentary majority for the first time since 2009. Despite the loss of its majority, the LDP will remain in power, continuing Japan’s recent economic progress and corporate reforms.

As a result, Abenomics, the policies implemented by late Prime Minster Shinzo Abe which have been seen as helping Japan finally reverse years of stagnation, should largely continue. These policies have called for loose monetary policy, fiscal spending and structural economic reforms. Although rates are rising, and we expect continuing interest-rate normalization over time, monetary policy remains relatively loose when compared to other developed markets.

However, we may see modest changes in priority given the changing politics. Ishiba has favored higher corporate and capital gains taxes, efforts to revitalize rural Japan, a higher minimum wage and spending to cushion the impact of higher prices. As attention turns to upper house elections next year, Japanese policy could veer toward greater fiscal spending in the short term to bolster the economy.

Japanese economic fundamentals strengthening

Improving Japanese economic growth remains a necessary priority for any new government. We see few signs that either the United States or global economies are tipping into recession this autumn, but some indicators have shown slowing. The US Federal Reserve’s 50 basis point interest rate cut in September and 25 basis point cut in November may give the US economy, and therefore the global economy, some support.

The International Monetary Fund (IMF) anticipates 3.2% global gross domestic product growth this year and next.1 US expansion may slow in 2025, according to the IMF, but Europe and Japan should see a pickup.

With the prospects remote for a major global recession, we believe fundamentals in the Japanese economy and stock market remain encouraging for value investing.

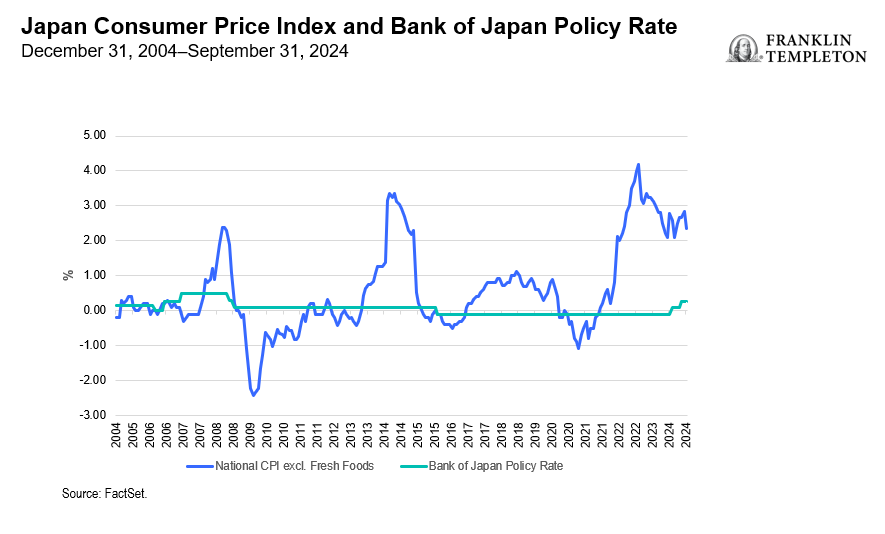

The Japanese economy appears to us to be emerging from years of stagnation. A rebound in goods and wage inflation should help the country boost economic dynamism and spark a period of hotter and more sustained growth. (Exhibit 2) Furthermore, Japan’s largest labor union group is seeking another 5% wage increase for members in 2025 after a sizable raise in 2024, reinforcing the positive economic outlook. Overall, the pace of wage gains across Japan have been increasing, rising at a 2.6% year-on-year pace in September after a 2.4% pace in August, according to the Japanese Ministry of Health, Labor and Welfare.

Exhibit 2: Japanese Consumer Prices Have Increased Year-over-Year

Additionally, we believe that the Bank of Japan will continue to gradually normalize monetary policy over the next couple of years, regardless of the political environment, as higher wages help end falling prices and stagnant incomes.

Companies embracing change

Corporate Japan is beginning to adopt change at the same time the economy moves to stronger growth and modest inflation. The Tokyo Stock Exchange (TSE) is encouraging companies to improve their returns and reduce their cost of capital as part of a push to make the country more investable. The Japanese market is rife with companies trading at book values below one, with the average price-to-book ratio on the Prime Tokyo Stock Exchange at 1.2 times and on the standard market at 0.8 times as of October 2024, according to data from the TSE.2 This compares with a price-to-book ratio of nearly 4.5 times for companies in the S&P 1500, according to data from S&P.3

The TSE is also pushing companies to reduce their cross-shareholdings, which are widely seen as a barrier to market efficiency and transparency, as well as a barrier to mergers and acquisitions.

We have begun to see several big companies, like Toyota Motors, begin to unwind holdings in related firms. Those companies with clear plans to improve returns and reduce their cost of capital, and that are willing to buy back stock trading below book value following the unwinding of cross shareholdings, are particularly appealing for more intense analysis, in our opinion.

Focus on valuation and catalysts

In our view, sifting through the Japanese market can uncover stocks trading at attractive valuations and that are willing to embrace structural changes. Greater certainty around economic, fiscal and monetary policy following the recent election can further help unlock value. We believe that an improving economy and faster wage growth may create long-term value opportunities particularly in domestically focused companies and that the Japanese market continues to have long-term appeal for stock picking.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Value securities may not increase in price as anticipated or may decline further in value. Growth or value as an investment style may become out of favor, which may have a negative impact on performance.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorized Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

_________________

1. International Monetary Fund, World Economic Outlook Update. October 2024. There is no assurance that any estimate, forecast or projection will be realized.

2. Source: Tokyo Stock Exchange. As of October 2024.

3. Source: S&P Dow Jones Indices. As of October 31, 2024.