Value stocks were strong in late 2024, and we think this strength has staying power. Economic growth looks likely to remain solid, inflation has retreated and central banks are cutting interest rates, while booming spending on artificial intelligence and infrastructure continues. But we also see risk and uncertainty rising with a shifting global political and policy landscape, possible trade conflicts and the ongoing fog of war in Europe and the Middle East.

As value investors, we believe that, given the still robust macroeconomic environment, any market dislocations this uncertainty produces can create opportunities for patient stock- pickers focused on valuation.

Finding value in growth and risk

With mainstream focus on a handful of high-flying US technology and communication services stocks over the past few years, our research tells us that equity market valuations appear rich. To us, this warrants a deeper focus on valuation and business fundamentals against a supportive global backdrop for economic growth.

In the United States, signs point to a healthy economy, strong labor market, moderating inflation and the resulting potential for further interest rate cuts. In its World Economic Outlook, the International Monetary Fund sees US economic growth of 2.2% next year.1 We expect this steady rate of growth, supported by consumer and business spending, to create a solid foundation for economically sensitive value stock performance.

Better value opportunities may be present outside the United States, however. International value stock valuations have trailed those in the United States. (See Exhibit 1.) While some may argue this discrepancy is a result of more sluggish economies, we believe anything that makes non-US markets more appealing for investment can narrow this yawning gap.

Exhibit 1: Mind the Gap: International Stock Valuations Trail Their US Counterparts

Europe could get a shot in the arm over the next few years should policymakers embrace the changes former European Central Bank President Mario Draghi laid out in his plan to improve European competitiveness and growth potential. Furthermore, we think structural changes to streamline the fragmented, overcapitalized eurozone banking system may further boost economic activity as banks strive to regain profitability.

In Japan, the situation is different. Both price and wage inflation have finally returned, and the Bank of Japan is positioned to slowly lift interest rates over the next few years as improving wages lead to greater spending and more robust economic activity.

This supportive global economic backdrop coexists with a layer of uncertainty. The incoming US administration has raised the prospect of levying tariffs on all its trading partners. US inflation, which has fallen from its peak, may rise again, as companies attempt to pass along higher import costs to consumers already coping with more expensive goods.

The ongoing conflicts in Ukraine and the Middle East also come with risks to energy markets and shipping channels, which may affect supply chains and potentially reignite inflationary pressures. Meanwhile, tensions between China and Taiwan also continue to simmer.

Embracing corporate change that delivers shareholder value

Structural corporate changes in Europe and Japan can also further lift value stocks. European companies are buying back their shares more aggressively. And when coupled with the larger more stable dividends, they pay out much more than their US counterparts.

Japanese companies, too, are slowly embracing change. The Tokyo Stock Exchange is encouraging companies to improve their book values and reduce their costs of capital to make the country more investable. Companies are also unwinding cross-shareholdings— if they use the proceeds to buy back shares, it can help make them more appealing to overseas value investors.

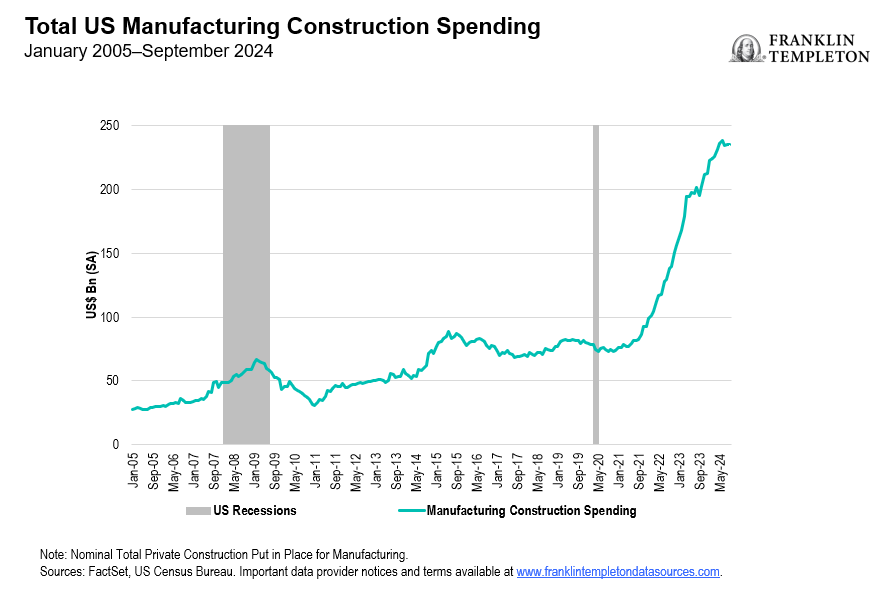

Meanwhile, corporate and government spending on facilities to support growth in artificial intelligence and on building out infrastructure continues. In the United States, we have seen a marked increase in manufacturing construction spending, as shown in Exhibit 2, over the past couple of years. Value companies are instrumental to this spending. They are crucial to the construction of chip foundries and data centers and to the electrical grid fortification and necessary HVAC systems to power, heat and cool them. And they build and upgrade the roads and bridges that tie regional transport together.

Exhibit 2: A Surge in US Infrastructure Spending

Smaller companies offer big potential

We think small-cap value stocks in the United States also have room to run. In general, the fortunes of smaller companies tend to be more closely tied to the domestic economy than their larger counterparts. And with more debt, lower rates may improve their balance sheets and provide more flexibility.

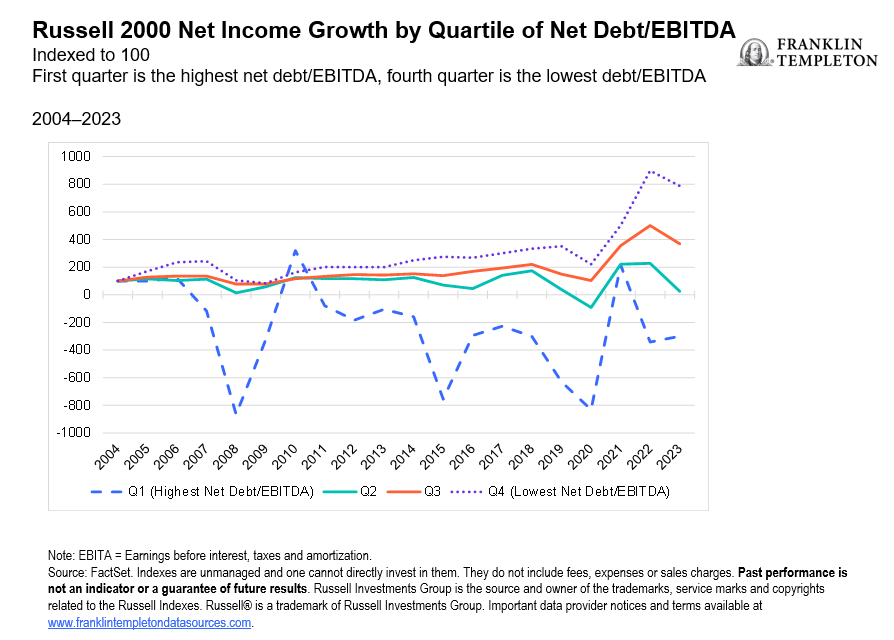

That said, we believe active stock selection will be key among smaller-capitalization stocks. Based on our analysis, companies with the least debt tend to have faster earnings growth, meaning higher quality companies can create value for shareholders more quickly than their lower quality counterparts, as shown in Exhibit 3. With small-cap valuations lower than those of large and mega-cap companies, investors can find attractively valued, quality small-cap companies with good earnings growth potential.

Exhibit 3: Lower Debt Can Support Faster Value Creation in Small Caps

Channeling duality to uncover value

We see ample opportunities for successful value investing in 2025. Both the positive impulse from global economic growth and corporate changes in Europe and Japan and potential disruptions geopolitics may cause can create openings to find mispriced stocks around the world and across the market cap spectrum. Success will hinge on careful stock selection and understanding the catalysts that can unlock value for investors. Embrace the market’s duality to uncover value.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Value securities may not increase in price as anticipated or may decline further in value. Growth or value as an investment style may become out of favor, which may have a negative impact on performance.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorized Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website

______________

1, As of October 25, 2024. There is no assurance that any estimate, forecast or projection will be realized.