English

English 简体中文

简体中文

Summary

Despite projections of a soft landing, the US economy remained resilient in 2024, driven by a strong consumer base, supportive fiscal policies, and business investments in areas such as artificial intelligence. While the US economy proved more resilient and exceeded economists’ expectations, there are potential downside risks to future growth.

Looking ahead to 2025:

- Favorable economic outlook, but potential downside risks exist: While we maintain a positive outlook on the US economy, significant policy uncertainty exists around tariffs, immigration, taxes, and government spending. Risks to economic growth include further weakening in the labor market, inflation staying elevated, and increased interest rates.

- Select opportunities in equities: We expect earnings and dividend growth to be key drivers to equity markets in the year ahead. Excluding a small number of large-cap growth stocks that have led the narrow rally, equity market valuations look reasonable to us overall.

- Fixed income sector diversification: Within fixed income, we maintain a focus on current income and managing duration exposures around what may be a wide range for long-term interest rates. In contrast to corporate bonds, we are seeing opportunities within agency mortgage-backed securities (MBS) where spreads remain compelling relative to historical levels.

Franklin Income strategies strives to maintain a well-diversified portfolio, while having ample liquidity to take advantage of potential market dislocations. We remain focused on staying nimble to take advantage of potential increases in market volatility and the investment opportunities that may arise as a result.

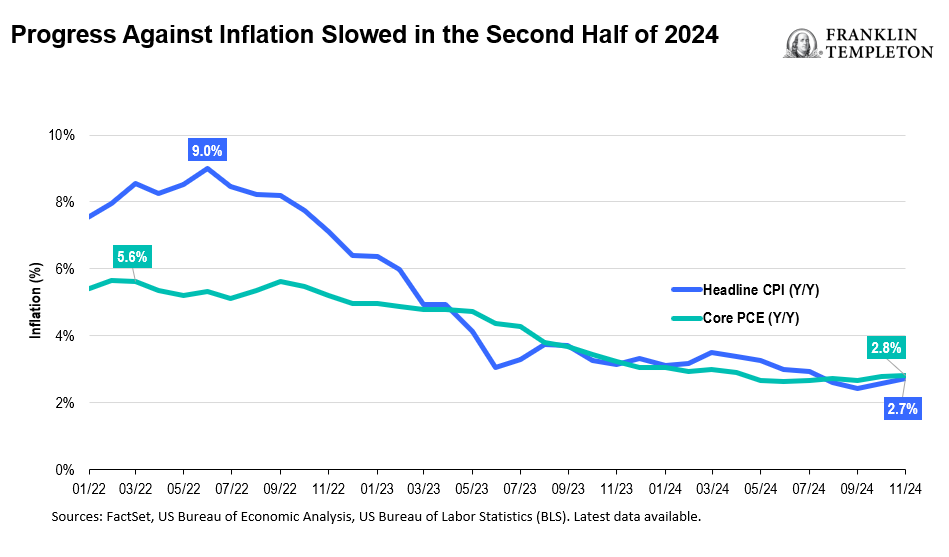

The US economy remained resilient in 2024, but progress against inflation stalled somewhat

While there were some projections of a soft landing in 2024, the US economy continued to prove resilient driven by several factors including strong consumer spending, supportive fiscal policies, and business investments in artificial intelligence (AI). US consumers have benefited from solid growth in their disposable income and by a surge in household net worth, which reached a record US$169 trillion in the third quarter.1 To this point, it appears that higher borrowing costs have had a muted effect on consumer finances overall as many consumers had locked in low rates from the prior years.

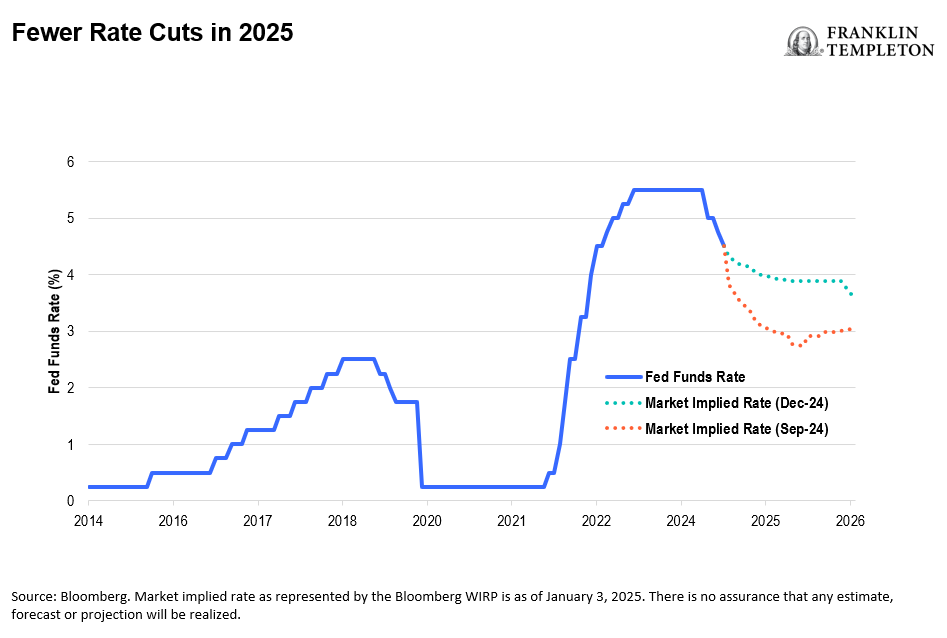

As was the case in 2023, disinflation in the United States continued in the first half of 2024. However, this momentum stalled somewhat in the second half with the latest core personal consumption expenditures (PCE) reading of 2.8%, well above the Federal Reserve’s (Fed’s) 2% target. By the middle of the year, the Fed’s secondary mandate to achieve maximum employment came into greater focus as concerns rose around growing weakness in the labor market. After a prolonged pause, the Fed cut interest rates by a full percentage point from September through December, reducing the fed funds rates to a range of 4.25%-4.5%. While we think that the Fed is likely to pursue further cuts in the year ahead, its approach will be cautious and data-dependent given the recent uptick in inflation and continued resilience of the US economy.

Navigating an uncertain environment ahead

As we look ahead, there are some potential downside risks that require careful monitoring. Risks include further weakness in the labor market, inflation staying elevated, and a higher-for-longer interest-rate environment. We expect some deceleration in the US economy with gross domestic product trending down toward its long-term growth rate of 1.5%-2%.

One of the bigger variables heading into 2025 is related to the second Trump Presidency and the impact of its potential policy initiatives. While policies that eventually get passed tend to be different than those proposed during the election campaigns, there is still significant uncertainty around tariffs, immigration policy, and fiscal deficits. Markets generally struggle with prolonged policy uncertainty, but efforts to reduce regulatory burdens have the potential to provide a tailwind to company earnings going forward.

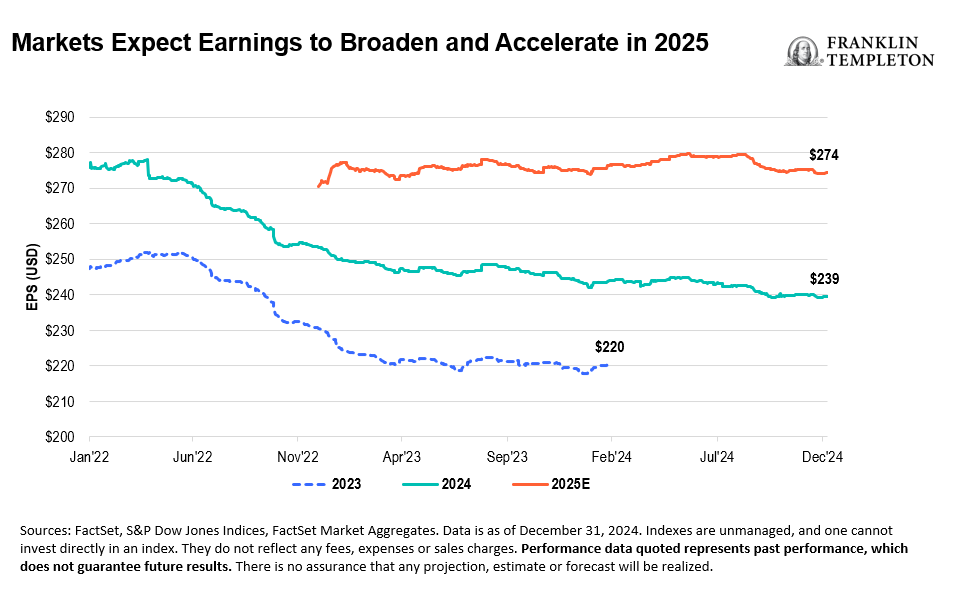

Earnings and dividend growth to be key drivers of equity markets

We expect dividends and earnings growth to be the key drivers of equity markets in the year ahead as the opportunity for further multiple expansion may be limited. While the broader S&P 500 Index has delivered substantial gains over the past two years, the performance has been concentrated in a relatively small number of growth stocks that have an outsized weighting in the index. This is most clearly seen in the outperformance of the market-cap weighted S&P 500 Index versus the equal weighted S&P 500 Index, which returned 57.9% and 28.7% (cumulative), respectively. Over the same time period, the MSCI USA High Dividend Yield Index returned 19.3%.2 After excluding a small number of mega-cap growth companies, equity market valuations appear reasonable to us overall as indicated by forward price-earnings (P/E) ratio of 16.5x for the equal-weighted S&P 500 Index.

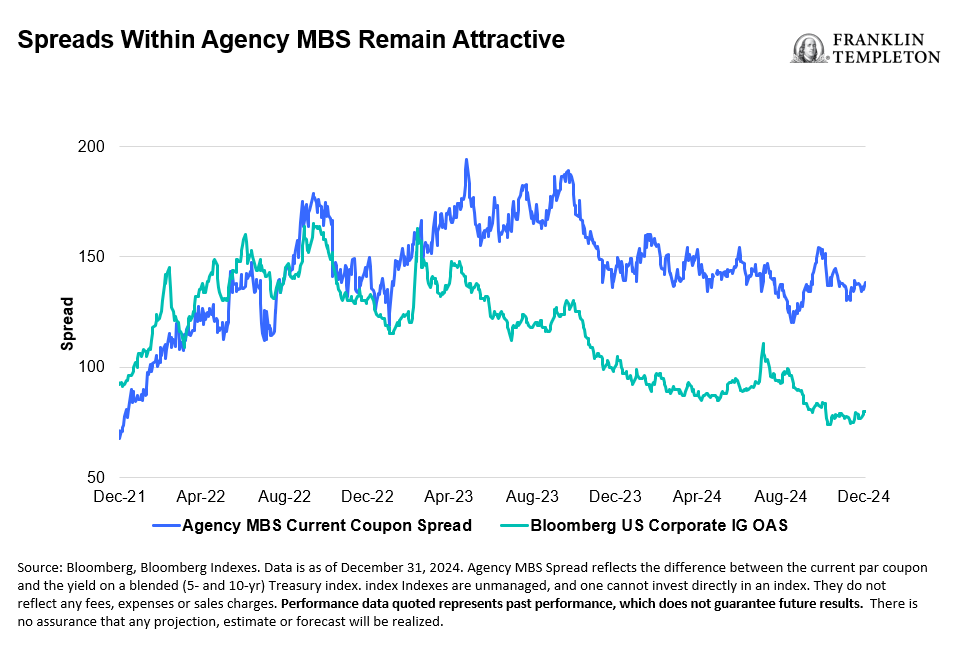

Shifting fixed income landscape, focus on sector diversification

Within fixed income, we are focused on current income and managing duration exposures around what may be a wide range for long-term interest rates. We may extend duration when the benchmark 10-year Treasury yield reaches around 4.75% and trim on rate rallies that push yields back toward 4%.

Credit spreads in both investment-grade and high-yield corporate bonds have tightened toward historical lows, leaving little room for further spread compression to contribute to total returns. In contrast, we find spreads in agency MBS still compelling compared to historical levels. This is a segment where we anticipate broadening our holdings to achieve fixed income sector diversification.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

Equity securities are subject to price fluctuation and possible loss of principal. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Diversification does not guarantee a profit or protect against a loss.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, http://www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

_________

1. Source: Federal Reserve. Financial Accounts of the United States. As of December 12, 2024.

2. Source: Bloomberg, MSCI. As of December 31, 2024. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.