While at times overlooked, dividends have played a substantial role in investor returns over the past several decades. From 1960 through the end of last year, roughly 85% of the S&P 500 Index’s cumulative total return can be attributed to reinvested dividends and the power of compounding. Dividend-focused strategies provide the potential for better stability, consistent income, and a hedge against economic uncertainty for all-weather portfolios.

As a new environment of tariff turmoil in the United States continues to prompt market volatility, investors are increasingly turning to dividend-focused strategies to boost portfolio resilience. Following an era dominated by growth stocks, dividend investing has seen something of a revival. US-listed, dividend-focused exchange-traded funds (ETFs) saw average monthly net inflows of nearly US$3.3 billion for the six months ending January 31, 2025, compared to US$107 million for the same period last year.1

The current murky global outlook understandably has investors seeking refuge in more stable components for a balanced portfolio. Dividend stocks—especially those with high-quality characteristics—can offer steadier and more predictable cash flows. And since such cash flows are key to many equity valuation models, estimating the intrinsic or fundamental value of dividend-paying stocks tends to involve less ambiguity than attempting to pinpoint fair valuations for growth stocks. Therefore, we believe dividend stocks can serve as a buffer in a diversified portfolio.

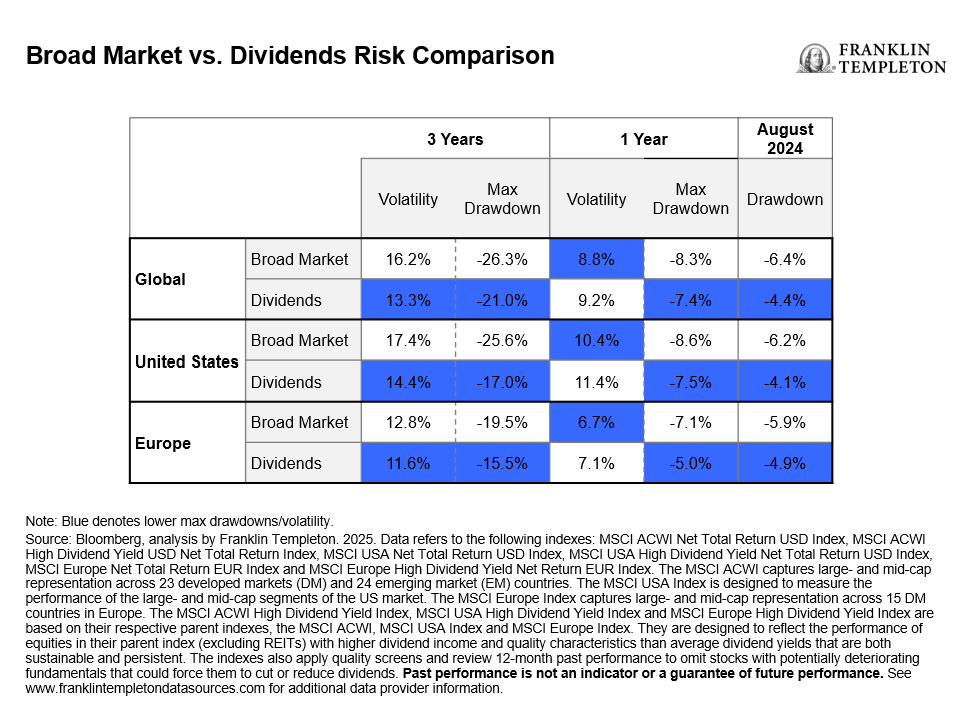

In our opinion, the appeal lies in their ability to moderate volatility during market drawdowns, while still offering significant upside potential. Dividend strategies have consistently demonstrated defensive properties across regions and varying timeframes. For the three-year period ending December 31, 2024, both volatility and maximum drawdowns for dividend payers were lower compared to the broad market across global, US and European exposures.2 When inflation and interest-rate fears reignited last August, dividend stocks held up comparatively well.3

Perhaps as a testament to the value investors place on the dividends in their portfolios, we have seen strong asset gathering in US-listed dividend ETFs even when fixed income ETFs are paying attractive yields. Dividend ETFs that target US exposures continue to dominate market share of U.S-domiciled ETFs, holding US$360 billion in assets (76% of all dividend ETF assets), with US$17.5 billion in new assets over the past year.4

International developed market dividend ETFs—which still comprise just a fraction of the US market—have also grown in popularity and attracted nearly US$3 billion in net inflows last year, representing 13% of total dividend ETF inflows.5

There are various approaches to dividend investing across this large pool of assets. For example, we’ve seen income-hungry investors making core allocations to rules-based, or multifactor, dividend strategies that incorporate active risk awareness by aiming to maximize yield per unit of tracking error relative to the broad market.

Other compelling strategies also employ custom indexes aimed at delivering excess or multiplied dividend yield relative to the broader market. These approaches present the potential for enhanced long-only equity income, underpinned by robust proprietary optimization methods that can more holistically consider how dividend stocks behave together. As enhanced versions of the first generation of rules-based portfolios, we believe these strategies may allow portfolios to be more responsive to shifting market environments, while incrementally increasing yield.

Looking ahead, we believe dividend strategies should continue to play a vital role in portfolios. Valuations in market-cap indexes, especially in the United States, remain ambitious given the potential disruptions that loom over global trade. In this environment, we believe dividend stocks of firms with proven business models and solid profitability will tend to be sought after and present a compelling alternative to more growth-oriented exposures. With sentiment for growth stocks now at a tipping point, we believe a favorable backdrop for dividend strategies has emerged.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal. Large-capitalization companies may fall out of favor with investors based on market and economic conditions.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Distributions are not guaranteed and are subject to change. Yields may be affected by changes in interest rates and changes in credit ratings.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Diversification does not guarantee a profit or protect against a loss.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2025 Franklin Templeton. All rights reserved.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: Morningstar Direct, as of February 2025.

2. Source: Bloomberg, Franklin Templeton 2025.

3. Ibid.

4. Source: Morningstar Direct, as of January 31, 2025.

5. Ibid.