After decades of relying on the US defense umbrella, Europe now must take a more active lead in its own security. Not only will the region need to replenish the stocks of munitions it sent to Ukraine, but it must spend on new military hardware and plan its own nuclear deterrence strategy. At the same time, Germany is realizing the roads and rails to move equipment and people around—as well as key energy, education and digital infrastructure—need major upgrades.

As more money is spent on both defense and infrastructure, we believe European industrials should benefit. Earnings growth should pick up for the large European defense names and more unified spending may force consolidation among smaller players. If this spending remains in place, corresponding infrastructure investment can further boost many old-economy, value industries and lead to faster regional economic growth. This structural tailwind could persist for years, in our view.

Offensive posture

European defense spending has climbed the past few years as Europe has had to replenish the equipment and munitions it sent to Ukraine. European NATO members spent about a fifth more in 2024 than 2023, according to preliminary NATO defense spending data. Despite this increase, Europe has underinvested for decades, and we believe the Continent is in the early stages of a multi-year expansion. Recent rhetoric from the United States about potentially cutting support has focused European leaders on the need to better plan for their own security.

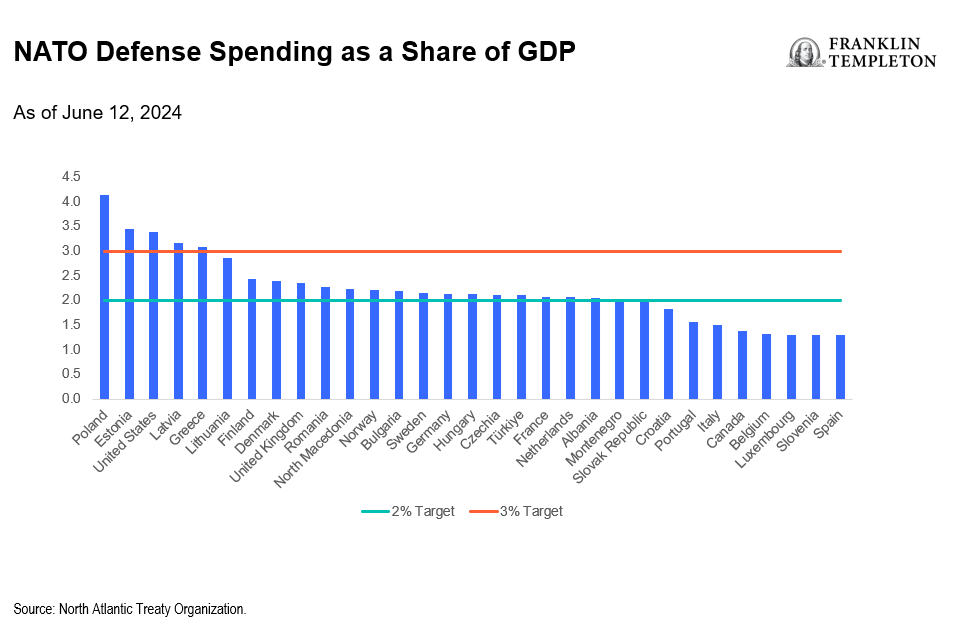

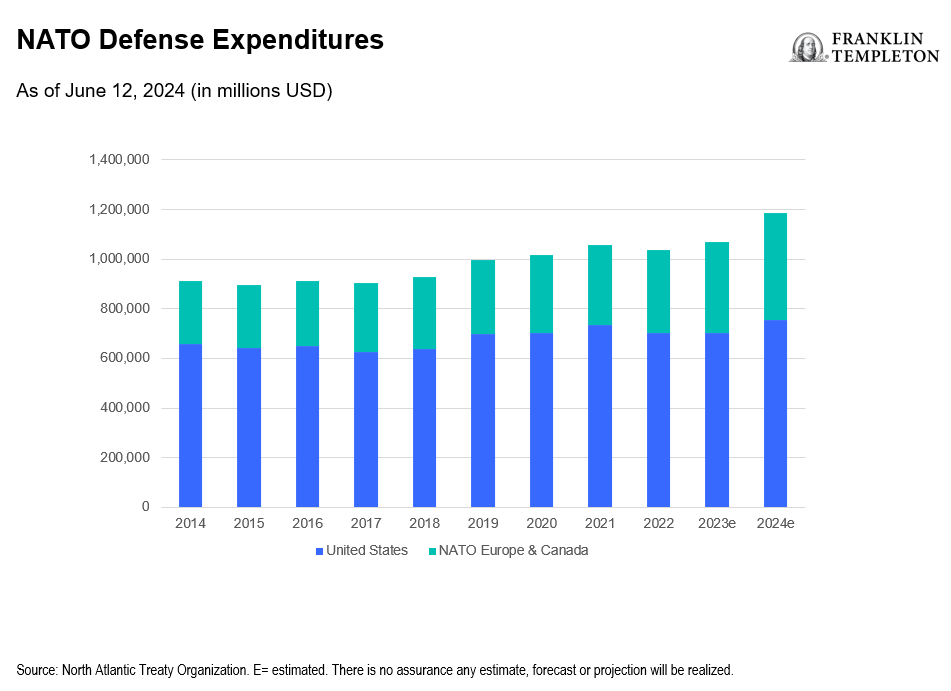

Europe has much to do, in our view. Several European NATO members still do not spend the minimum 2% of their gross domestic product (GDP) on defense (See Exhibit 1), and Europe overall makes up only a third of total NATO defense spending (See Exhibit 2).

Exhibit 1: European Defense Spending Has Room to Rise

A recent report from research institute Bruegel and the Kiel Institute for the World Economy estimates Europe will need €250 billion more in defense spending and another 300,000 troops just to deter Russian aggression in the short term. And several European leaders have called for countries to spend as much as 3% of GDP to modernize and expand their defense capabilities.

Exhibit 2: The US Spends the Most on Defense in NATO

We also believe Europe must determine what regional nuclear deterrence should look like, with France recently proposing to open its limited nuclear umbrella over the Continent. Unlike the United States, which has the Nuclear Triad, encompassing nuclear ground, sea and air capabilities, Europe has no clear nuclear strategy, and only France and the United Kingdom are nuclear powers.

To fund all this spending, the EU is looking at extending €150 billion in loans and allowing members to spend an additional €800 billion over the next four years without triggering the bloc’s budgetary rules. The incoming German chancellor also won legislative approval for a €500 billion defense spending facility in mid-March.

Freeing up more funds is only a first step, in our view. EU defense spending tends to be uncoordinated, and the European defense industry is highly fragmented. For instance, Europe has 19 different battle tank systems in place compared to just one for the United States, and 27 different destroyers and frigates versus the United States’s four. Aggregating spending and harmonizing equipment specifications, as the European Commission recently proposed, could better boost economies of scale and capacity use.

Combat-ready

Despite the recent enthusiasm for defense stocks, the European defense industry may not currently have the full range of capabilities to meet all the region’s security needs. Nearly two-thirds of EU funds are used to purchase gear from the United States and to lesser extent South Korea, not European defense contractors. While some of this spending is on gear and systems only the United States currently produces, we believe European alternatives may exist.

Additionally, as warfare increasingly relies on drones and digital technologies, there are opportunities for domestic sectors to develop. Meanwhile, beyond the big regional defense companies, the mid-cap defense groups may need to merge to improve operations and better meet Europe’s defense needs, another potential catalyst.

We think South Korean defense companies have done an impressive job of supplying gear like tanks, rocket launch systems and armored vehicles to Eastern European and Scandinavian markets. They too may have the opportunity for additional growth as Europe spends more overall.

Infrastructure support

Regional governments have announced plans to increase investment in the region’s creaking infrastructure to go alongside more defense spending. Sweden, which recently joined NATO, is putting money into improving roads and railway lines to support the transport of troops and military hardware.

To go with the €500 billion in defense spending, Even though the incoming German Chancellor’s term is only four years, he also won backing for €500 billion over the next 12 years to fund infrastructure investments. Other countries may find it necessary to follow suit, despite already high debt levels, as Germany loosens its fiscal constraints to spend more across the economy. As a result, this European defense investment cycle may also turn into a broader European infrastructure investment cycle over time.

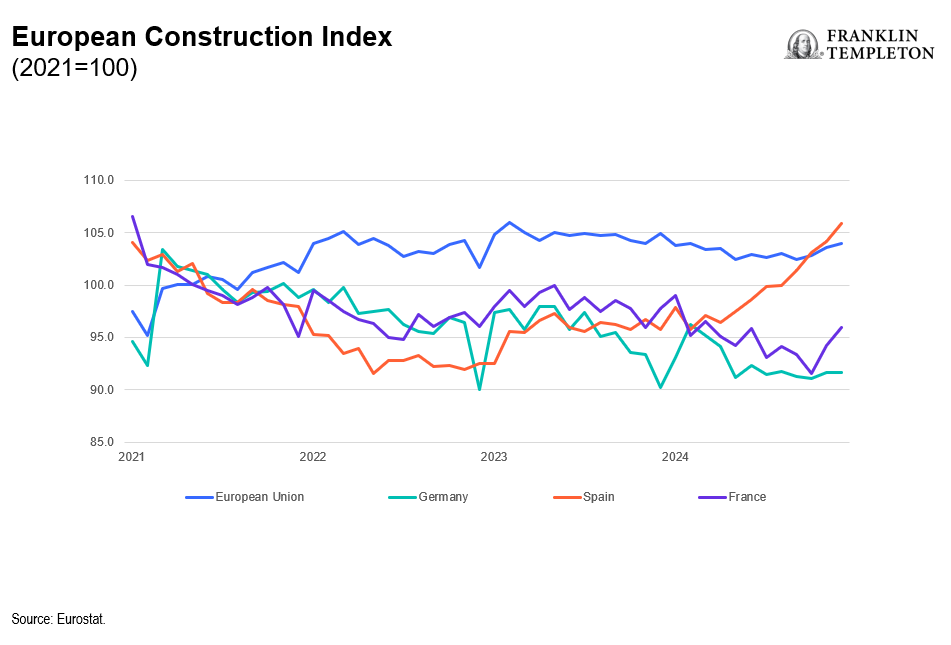

The construction sector, for one, has been particularly weak in major European countries like Germany and France in recent years (see Exhibit 3). A greater focus on improving public transportation, schooling, housing and energy supply can drive greater economic activity over time and lead to better long-term economic growth.

Exhibit 3: European Construction Activity Has Been Sluggish but May See an Upturn

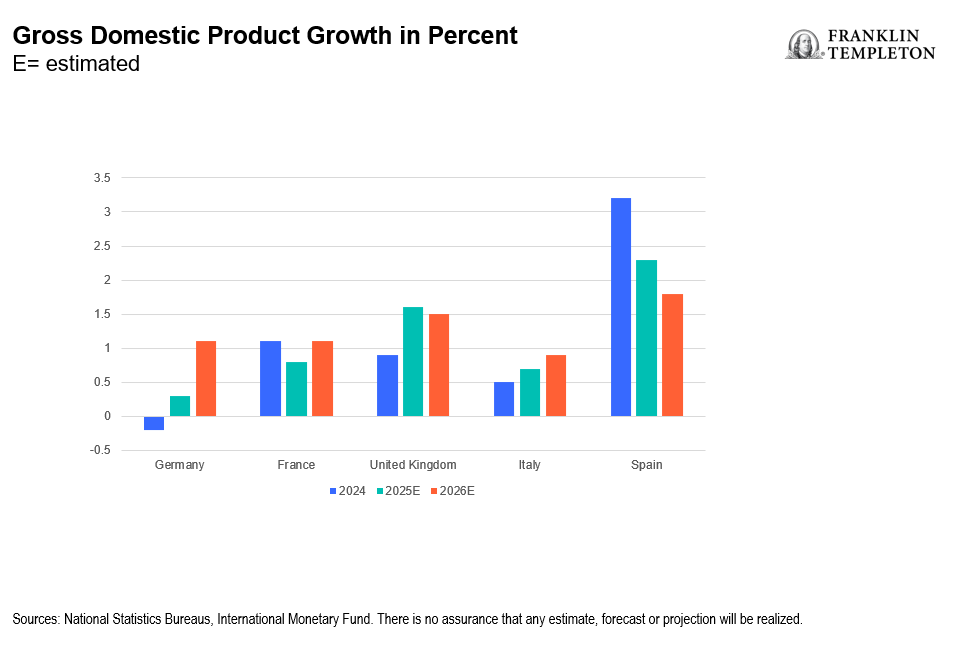

Value industries, from cement and asphalt firms to rail and rail equipment companies, as well as power equipment, construction and commercial vehicle companies, could all benefit, and we could see a positive spillover to the broader economy which may help ignite regional economic growth after years of sluggishness (see Exhibit 4).

Exhibit 4: Slower European Economic Growth May Get a Boost

Faster growth in Europe’s largest economy would be positive for the region overall and for equity markets, in our view, as it would reinforce the efforts taking place at the European Union (EU) level to foster a more competitive continent and further boost economic activity.

The EU has been considering a report from former European Central Bank (ECB) Chief Mario Draghi that it needs to spend more on infrastructure, electrification and research and development to improve competitiveness. Much of this additional spending, and resulting industrial production and job creation, may come outside the normal European budgetary constraints and can boost the economic benefit to the region over time.

In all, the renewed focus on defense is likely to lead to a bigger focus on domestic investment. While the European defense sector has rallied in anticipation of greater profits, the knock-on effects are still being felt. It may be a couple of years before the earnings growth at defense and infrastructure companies start to really come through. After years of neglect, we believe global investors should pay more attention to the European equity markets as Europe goes on the economic offensive.

For more on Mutual Series’ outlook on Europe please read: European stock valuations are knocking—answer | Franklin Templeton

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Investing in companies in a specific country or region, may result in greater volatility than more broadly diversified geographically.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2025 Franklin Templeton. All rights reserved.