Executive summary

We believe the US economy remains strong, with gross domestic product (GDP) growth above trend despite recent pullbacks in retail sales and consumer confidence. Concerns over US President Donald Trump’s tariff policies may be overstated, but persistent fiscal deficits will likely have a longer-term impact. The EU’s economy is weaker, with anemic growth, which has led the European Central Bank (ECB) to cut rates. Trump’s trade policy has created market uncertainty, potentially delaying disinflation and impacting economic growth. Market expectations of the Fed’s rate-cut path have fluctuated, reflecting concerns over economic policies. Fixed income spreads have widened again in 2025, due to uncertainty around tariff and fiscal policies. Our portfolio strategy focuses on balancing duration,1 dversification and adjusting international exposures to mitigate risks.

Fixed income dashboard

Outlooks for fixed income sectors are based on our analysis of macroeconomic themes and the technical conditions, fundamentals, and valuations for each asset class. We rate each sector from bearish to bullish to express our projections for relative returns over the next 6-12 months.

Second quarter 2025 market backdrop

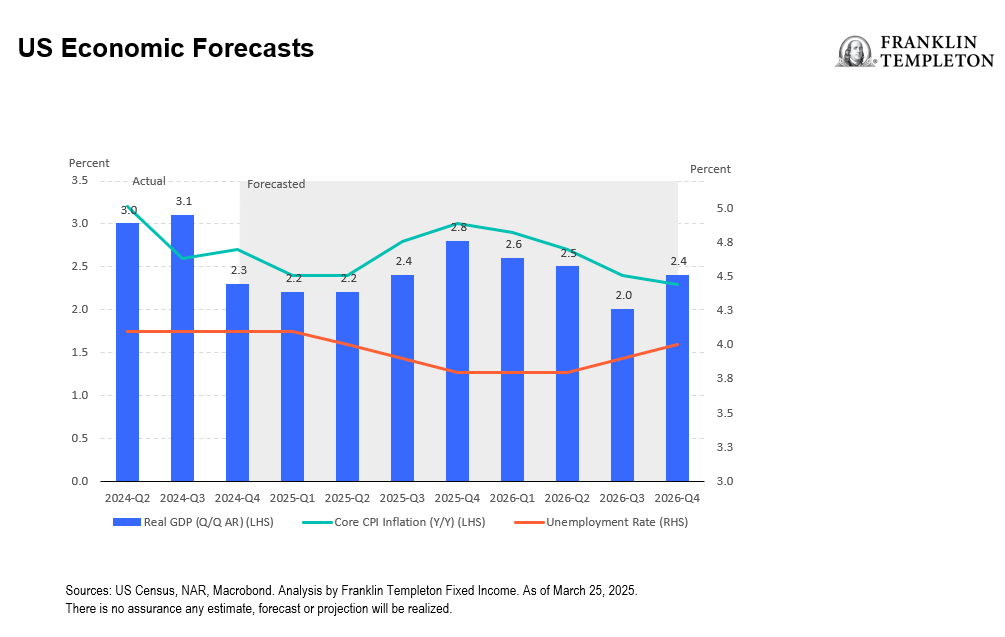

We feel that the underlying US economy is in good shape. GDP growth has remained strong, and we see it continuing above trend for the rest of the year. There has been a pullback in retail sales over the past few months and consumer confidence has waned. Measures of current business sentiment have also seen a downturn, but longer-term expectations remain upbeat. In our view, concerns over the impact of Trump’s tariff policies are warranted but may be overstated, as the US remains mostly a closed economy. We consider the US fiscal deficit policy will have a longer-term impact on the US economic growth picture and US Treasury (UST) issuance. We believe that deep cuts in spending and/or tax increases will be necessary to maintain a manageable fiscal deficit and limit debt interest payments going forward.

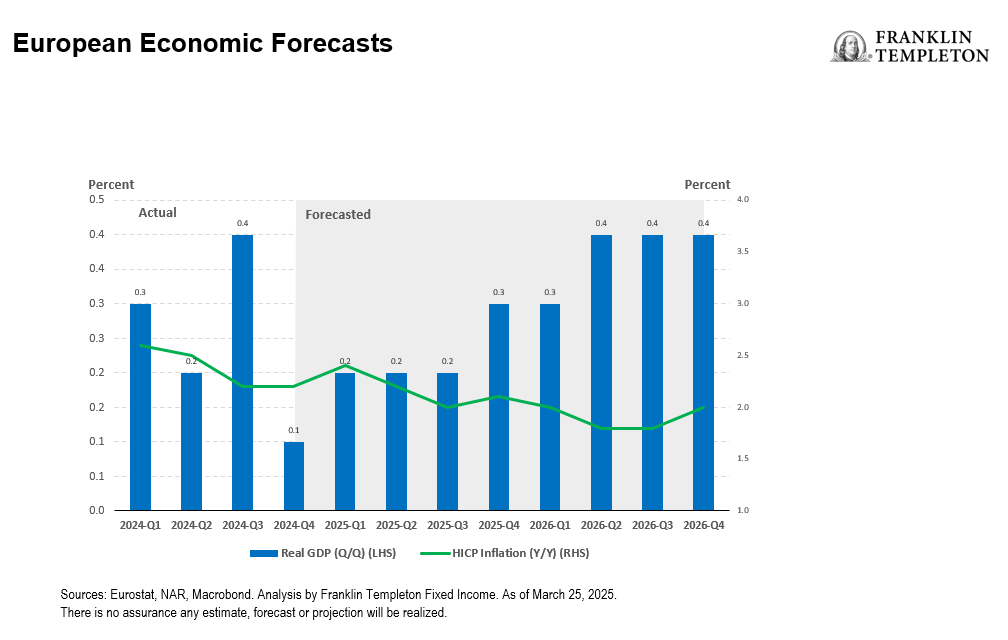

The EU’s economy does not enjoy the same strength as the United States. Growth continues to be anemic with little signs of improvement. The ECB has had to cut rates in an attempt to stave off a full-blown recession. Any increase in tariffs on EU imports into the United States will have significant ramifications on growth for the economy. In addition to this, the US decision to pull back its commitments to support the region has led the German government to announce a large program of both defense and infrastructure spending. This will ultimately lower the region’s dependence on the United States and bolster its economy, but this will likely take several years for it to be fully felt.

The Fed finds itself in the same boat with the broader investment industry. US President Trump’s on-again, off-again trade policy has led to a significant amount of market uncertainty. This has the potential to delay disinflation and negatively impact growth prospects. There are also risks associated with uncertainty leading to slower growth leading to increased uncertainty. If this process becomes recursive, it runs the risk of having a severe impact on the economy and GDP growth falling below trend.

It has become more difficult for market participants and the Fed to look through the day-to-day headlines caused by the administration as the endgame is still unknown. We can see some of the current uncertainty in the market in several ways.

- Path of fed funds: There has been significant volatility in the market’s expectations of rate cuts by the Fed. In late 2024, there were strong market expectations that the Fed would be pushed into a quick and deep rate-cutting scenario to combat the potential of a recession. This led the market to price in a total of four to five rate cuts in 2025. After signs that the Fed had indeed set the table for a soft landing, the market pulled back on its expectations for the number of rate cuts to just one, which was consistent with the Fed’s December 2024 Summary of Economic Projections. Concerns over the impact of Trump’s economic policies and their implications for growth have led the market to upsize its rate cut expectations to three 25-basis point (bp) cuts by the end of 2025.

- Market spreads: December 2024 saw multi-decade low spreads across a number of fixed income sectors, particularly in corporate credit markets. Investors were willing to overlook full valuations as locking in attractive all-in yields became more important. A strong economic backdrop also bolstered corporate fundamentals. Spreads in 2025 have widened significantly, as there was a greater appreciation of the uncertainty surrounding how US tariff and fiscal policies will impact different sectors and issuers.

- Technical conditions: There had been a wash of money coming into several fixed income sectors that created a tailwind for spreads. New issues across corporate bond and securitized sectors were met with overwhelming demand. This was partially due to cash sitting on portfolio balance sheets that needed to be invested and limited net new issuance. Historically, we have seen that these types of conditions can turn on the market, leading spreads on new issuance and in the secondary market to widen putting downward pressure on valuations.

Second quarter 2025 portfolio themes

With these challenges in mind, we take a holistic approach to our portfolio construction process, evaluating each variable and related sector correlations. Additionally, we use our dedicated research analysts to identify the potential impact on specific sectors and issuers to make sound risk/return decisions across our portfolios. Specifically, here are some of the themes we are considering in our investment process.

- Duration balancing: In the past several sector views publications, we had advocated for remaining on the shorter end of the yield curve to limit the impact of rising yields across maturities. This view has not changed. In our view, UST yields remain below our base-case projection of fair value. Given the current state of the markets and heightened levels of uncertainty, we still feel that the Fed has limited room to maneuver and has one to two cuts left in this series before reaching a steady state of around 4%. We continue to adjust our duration positioning to take advantage of changing yields in the market.

- Diversification: We believe it is prudent to spread exposure across a number of fixed income sectors. Given the uncertain times that we are in, we think it is even more important. In any scenario of tariffs and fiscal spending increases, there will be winners and losers. Within our portfolio construction and optimization process, we not only look at the correlations of sectors against themselves but also use duration exposures to hedge out macroeconomic risks such as a slowing economy or an increase in inflation. Diversified positioning can provide a substantial base to use risk mitigation tools to improve outcomes.

- International impacts: With a broadly closed US economy, we feel that the impact of increased tariffs will have a limited impact on growth and inflation. That might not be the case for many of our trading partners. Economies in Canada, Mexico and the EU have more skin in the tariff game, which gives them less leverage to negotiate a beneficial outcome. Emerging market economies may have even higher exposure to US trade policy. We are adjusting our country and currency exposures to take into account various US tariff changes and reciprocal trade levies and their impact on fixed income returns.

Any period has had some level of uncertainty, but we all can agree that current uncertainty is high. It is important to keep abreast of day-to-day changes to policy and rhetoric, but it is equally if not more important to look through the short-term news and focus on longer-term impacts. We continue to use all our tools and expertise to construct our portfolios with the aim of providing improved outcomes for our clients.

Overall risk outlook

Neutral

We have left our overall risk outlook at neutral, as we see strong economic fundamentals being offset by increased uncertainty regarding Trump’s economic policies. The on-again, off-again tariff news has caused some trepidation within the market, since no one has much insight into the endgame. Trump himself as stated that the US economy would feel some pain as it adjusts to the new reality. With this backdrop, we have seen spreads across most fixed income sectors widened from what had been 20-year lows. Technical conditions continue to be strong across sectors, but we feel this could change relatively quickly if volatility remains high. Changes to US tariffs will have a stronger effect on internationally focused sectors including European credit and emerging market debt. In our view, spreads have not widened enough, on the whole, to warrant us changing our neutral stance. We have been using volatility in relative spreads to rebalance our holdings, taking advantage of sectoral spread moves.

Key sector viewpoints

Moderately bullish

Municipal (muni) bonds: We remain moderately bullish on muni bonds. The taxable segment continues to benefit from a favorable technical backdrop that is driven by restricted new supply and solid demand. Meanwhile, the tax-exempt market is witnessing robust new issuance that is being met with healthy fund inflows. We believe that the still-elevated yields—which can be particularly appealing on a tax-adjusted basis—should continue to draw investor interest. Overall, credit fundamentals remain stable across most parts of the market. While inflation is cooling, a trend which is translating into slower revenue growth, revenues in general are still outpacing costs. The new US administration’s proposed policies and reforms add a level of uncertainty to our outlook. However, municipalities are in a strong position to be able to deal with potential challenges, in our view. That is why we continue to expect stability in this sector over the medium term and see investment opportunities across maturities as well as across the credit spectrum.

Neutral

Emerging markets (EM): Despite an unpredictable US policy environment, we believe that EM fixed income will remain supported, given noticeable fundamental improvements since the COVID-19 pandemic, validated by recent rating agency upgrades. Liquidity risks have eased due to generous multilateral and bilateral support, and we do not expect a sovereign default in 2025. Investment decisions are made on a case-by-case basis given that we are likely to see greater performance dispersion, while we are also mindful of risks such as a turn in global growth and the curtailment of international aid to EM countries. We favor EM hard-currency bonds versus local-currency bonds, retaining a preference for lower-quality US dollar-denominated names with idiosyncratic performance drivers. A strong US dollar, higher-for-longer US rates and a slowdown in disinflation have seen EM central banks turn more cautious, delaying further rate cuts. Consequently, within local-currency bonds, we prefer higher-yielding frontier market countries that have their own unique drivers of foreign exchange and local rates.

Neutral with reason for concern

Euro credit: Given current tight European high-yield (EHY) spreads and increasing political animosity at the international level, we believe a cautious stance is warranted. However, we also believe that the decline in prevailing funding costs will be a major tailwind for companies that were not able to afford last year’s prevailing yields. We are expecting EHY default losses to come down compared to last year. Increasing German spending should support much needed economic growth in stagnant European cyclical sectors. European investment-grade (IG) credit fundamentals have remained in good shape. Although earnings have been overall resilient, tariff threats and rising geopolitical risks are creating uncertainties. Against this backdrop, we expect a slight deterioration in European IG fundamentals over the 6-12 months, although strong credit metrics and solid liquidity profiles should provide financial flexibility for management teams to navigate these challenges.

Moderately bearish

US Treasuries (USTs): We have downgraded our outlook on USTs to moderately bearish, primarily due to the increase in volatility. From our last publication, benchmark 10-year UST yields have traded from 4.79% mid-January to 4.16% in early March with single day changes of up to 14 bps. Our outlook must be seen through the lens of this volatility. We have not seen economic data that would lead us to believe that we are looking at a substantial weakening of underlying fundamentals. This should keep the Fed on its current trajectory moving thoughtfully as they lower rates. Although UST yields had moved more into the range we projected earlier, before retreating along a bumpy road. We see no reason to change our view that 10-year yields will migrate us toward 5% by the end of this year. Daily news stemming from the new presidential administration’s economic policies continue to cause day-to-day volatility in markets. We feel a more tactical approach to duration positioning is warranted, with lightening up as yields move toward the bottom of the current range.

Sector settings overview

Moderately bullish

Municipal bonds: Stable credit fundamentals, healthy investor demand and relatively attractive yields lead us to remain moderately bullish on the muni-bond sector.

US Treasury-inflation protected securities (TIPS): TIPS returns have been based on changing break-even inflation changes. Moving into the second quarter, positive inflation accruals tend to move higher, supporting valuations.

Neutral with reason for optimism

Floating-rate loans: We remain generally constructive amid an overall positive macroeconomic environment and a low maturity wall, although bifurcation between industries and issuers may be enhanced in the coming months.

Mortgage-backed securities: MBS valuations continue to look attractive relative to IG corporates, and prepayment risk remains minimal, in our view.

US high-yield (HY) corporates: While fundamentals and technical conditions remain supportive, valuation is less compelling as spreads are at historic tights.

Neutral

Asset-backed securities (ABS): Although the year started with healthy ABS supply, tight spreads and relatively stable consumer credit, there is a potential for increased volatility as the new administration implements its policy agenda.

Collateralized loan obligations (CLO): Although CLO credit fundamentals have improved since last year, a slower economy and higher interest rates continue to pressure lower-rated loan issuers’ ability to refinance.

Commercial mortgage-backed securities: While commercial real estate (CRE) is showing signs of improvement, higher interest rates, increased rate volatility and tighter credit conditions could weigh on the sector.

EM corporates: The overall fundamental strength of the asset class remains intact. However, we are cautious about US trade policy and regard diversification as a vital discipline.

EM sovereign debt: Credit fundamentals and a stable near-term financing outlook remain supportive in our view, although investments will be made on a case-by-case basis amid greater US policy volatility.

European government bonds: The ECB continues to address the weakness in European macro-economic conditions through a series of rate cuts. We are closely watching US tariff policy and implications to euro-area economies.

European high yield corporates: We feel a neutral stance is warranted with increased uncertainty due to heightened political risks from US tariff policy, but this is mostly offset by fundamental issuer strength.

Global sukuk: With geopolitical and economic events fueling volatility, we favor an increase in defensive allocations to higher-quality fixed income sectors—such as global Sukuk.

Non-agency residential mortgage-backed securities: Given rich valuation and modest home price growth expectations, we are neutral on the sector and favor opportunities near the top of the capital stack amid a flat credit curve.

Neutral with reason for concern

Euro IG corporates: Euro IG credit remains resilient, supported by solid fundamentals and ECB rate cuts, but tight spreads and rising risks have led us to revise our outlook one notch lower—to neutral with reasons for concern.

US IG corporates: Strong demand and solid fundamentals support US IG bonds, but tight spreads and rising geopolitical risks lead us to favor high-quality issuers, short maturities and lower dollar-priced bonds.

Moderately bearish

UST: We have downgraded our view based on uncertainty in the UST market from federal government policies and additional issuance putting upward pressure on yields.

Bearish

Japanese government bonds (JGBs): Market focus will likely be on what the Bank of Japan thinks is the terminal policy rate. We believe yields on JGBs will continue to trend higher.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default. Floating-rate loans and debt securities are typically rated below investment grade and are subject to greater risk of default, which could result in a loss of principal. Asset-backed, mortgage-backed or mortgage-related securities are subject to prepayment and extension risks. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Leverage increases the volatility of investment returns and subjects investments to magnified losses and a decline in value.

Diversification does not guarantee a profit or protect against a loss.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Brazil: Issued by Franklin Templeton Investimentos (Brasil) Ltda., authorized to render investment management services by CVM per Declaratory Act n. 6.534, issued on October 1, 2001. Canada: Issued by Franklin Templeton Investments Corp., 200 King Street West, Suite 1500 Toronto, ON, M5H3T4, Fax: (416) 364-1163, (800) 387-0830, http://www.franklintempleton.ca. Offshore Americas: In the U.S., this publication is made available by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906. Tel: (800) 239-3894 (USA Toll-Free), (877) 389-0076 (Canada Toll-Free), and Fax: (727) 299-8736. U.S.: Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Issued in Europe by: Franklin Templeton International Services S.à r.l. – Supervised by the Commission de Surveillance du Secteur Financier – 8A, rue Albert Borschette, L-1246 Luxembourg. Tel: +352-46 66 67-1 Fax: +352-46 66 76. Poland: Issued by Templeton Asset Management (Poland) TFI S.A.; Rondo ONZ 1; 00-124 Warsaw. Saudi Arabia: Franklin Templeton Financial Company, Unit 209, Rubeen Plaza, Northern Ring Rd, Hittin District 13512, Riyadh, Saudi Arabia. Regulated by CMA. License no. 23265-22. Tel: +966-112542570. All investments entail risks including loss of principal investment amount. South Africa: Issued by Franklin Templeton Investments SA (PTY) Ltd, which is an authorised Financial Services Provider. Tel: +27 (21) 831 7400 Fax: +27 (21) 831 7422. Switzerland: Issued by Franklin Templeton Switzerland Ltd, Stockerstrasse 38, CH-8002 Zurich. United Arab Emirates: Issued by Franklin Templeton Investments (ME) Limited, authorized and regulated by the Dubai Financial Services Authority. Dubai office: Franklin Templeton, The Gate, East Wing, Level 2, Dubai International Financial Centre, P.O. Box 506613, Dubai, U.A.E. Tel: +9714-4284100 Fax: +9714-4284140. UK: Issued by Franklin Templeton Investment Management Limited (FTIML), registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. Tel: +44 (0)20 7073 8500. Authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Australia: Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849) (Australian Financial Services License Holder No. 240827), Level 47, 120 Collins Street, Melbourne, Victoria 3000. Hong Kong: Issued by Franklin Templeton Investments (Asia) Limited, 62/F, Two IFC, 8 Finance Street, Central, Hong Kong. Japan: Issued by Franklin Templeton Investments Japan Limited. Korea: Issued by Franklin Templeton Investment Advisors Korea Co., Ltd., 3rd fl., CCMM Building, 101 Yeouigongwon-ro, Yeongdeungpo-gu, Seoul, Korea 07241. Malaysia: Issued by Franklin Templeton Asset Management (Malaysia) Sdn. Bhd. & Franklin Templeton GSC Asset Management Sdn. Bhd. This document has not been reviewed by Securities Commission Malaysia. Singapore: Issued by Templeton Asset Management Ltd. Registration No. (UEN) 199205211E, 7 Temasek Boulevard, #38-03 Suntec Tower One, 038987, Singapore.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

______________________

1. Duration measures the sensitivity of price (the value of principal) of a fixed-income investment to a change in interest rates. The higher the duration number, the more sensitive a fixed-income investment will be to interest rate changes.