English

EnglishInflation, energy prices, interest rates, wage pressure, supply chains, COVID-19 third wave—there are a number of issues weighing on investor sentiment in the United Kingdom. However, we believe there are several positive indicators that counter these headwinds, such as a well-capitalised consumer with pent-up household savings, a sharp rise in initial public offerings (IPOs) and merger & acquisition (M&A) activity, and attractive valuations compared to the rest of the world.

As we move past what is likely the most acute stage of the COVID-19 pandemic, the second-order effects of this recovery are beginning to cause concern for investors.

Stagflation (high levels of inflation but low economic growth) has become a potential scenario. As economies have reopened, supply-chain bottlenecks and rising commodity prices have caused pockets of severe inflation (such as used car prices rising 18.3% year on year)1 as supply has not been able to keep up with excessive demand. In the United Kingdom, rising energy prices are likely to drive inflation higher into next year.

A specific point of contention is the increase in the energy price cap in spring 2022, which could see energy prices rise by 30%-40%, adding as much as 1% to inflation. We see this, along with higher levels of taxation through national insurance contributions, as examples of how the potential exit rate of growth from the pandemic may not be fully achieved.

Labour costs are undoubtedly the greatest challenge to our view of inflation. The unemployment rate at 4.5% (as of August 2021) is testament to the effectiveness of government policy during the pandemic, but we remain vigilant as to how the employment backdrop evolves going into 2022 as the furlough scheme is wound down.

Amid firming prices, central banks globally have taken a more hawkish tone, though this may not translate into policy changes. The Bank of England (BoE) has a somewhat different policy framework than the US Federal Reserve (Fed) and European Central Bank (ECB). The Fed and ECB target an average rate of inflation of 2% over the cycle, whereas the BoE targets an explicit 2% level, making it more justifiable to raise interest rates in the United Kingdom. As of October 2021, the market-implied base rate a year forward is around 80 basis points, from a current level of just 10 basis points. With UK gross domestic product 3% below its pre-pandemic peak, and with a raft of fiscal tightening measures on the horizon, we see considerable risk that simultaneous monetary tightening may derail any further recovery.

The definition of “transitory inflation” continues to be stretched, but we believe the bulk of inflationary pressures seen in the current data is temporary, and that forecasts for inflation as high as 7% for 2022 will prove excessive. Elsewhere, we have been surprised by the increased government intervention in the United Kingdom across the private sector as the pandemic has subsided. We see this as a harbinger of risk should it continue. There is a limit to how much a government can step in to help failing companies and sectors. In our opinion, reducing competitiveness in an economy rarely results in the effective allocation of resources and beneficial outcomes over the longer run.

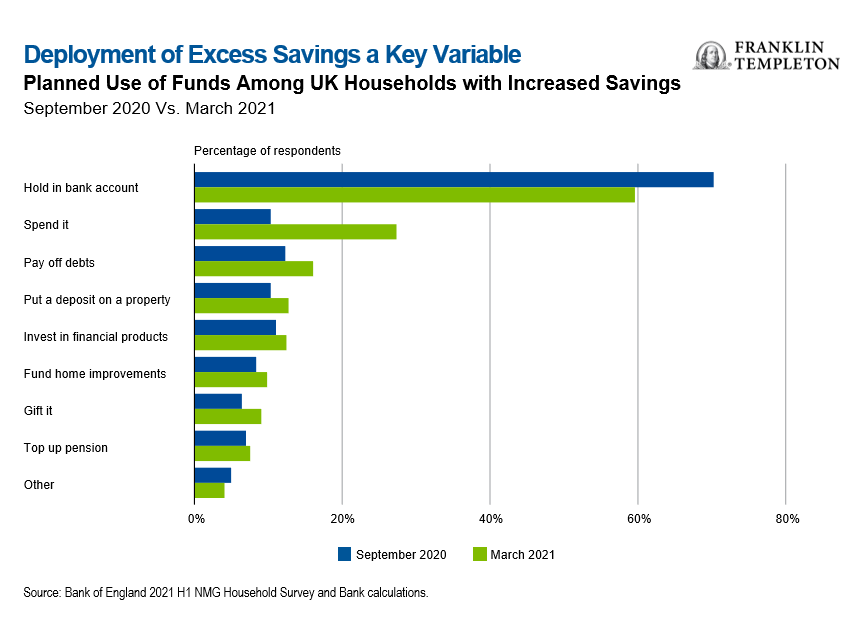

Despite these risks, we believe the UK consumer is well-capitalised to abate rising energy prices and interest rates. Through the pandemic, consumers have built up savings which are yet to be deployed. A BoE survey (see below) indicated that the majority of investors plan to continue holding onto their savings in the short term, but we expect to see this money flow back into the economy through the remainder of 2021 and into 2022.

Another positive indicator is a significant increase in market activity as we move past what is likely the most acute stage of the pandemic. By the end of the third quarter 2021, UK equity markets had seen the highest rate of IPOs since 2014, with a quarter of the year still to go.2 While this is partly due to a backlog of postponed IPOs through 2020, it indicates that risk appetite is returning for both businesses and investors. We have also witnessed an uptick in M&A activity, which is typically a strong signal for equity markets as company valuations are perceived to be cheap and ripe for acquisition.

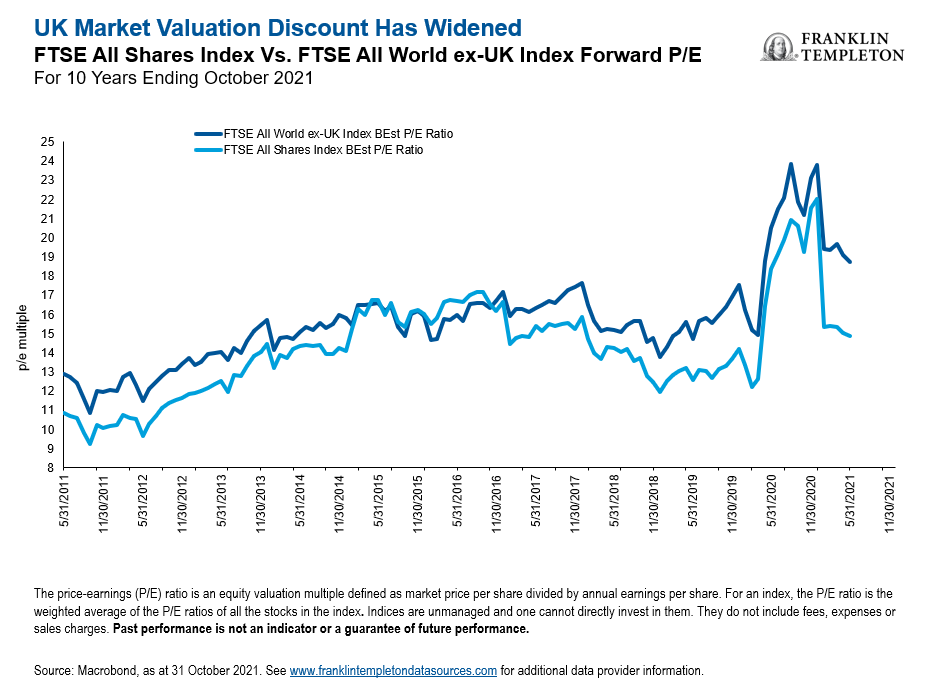

Turning our attention to valuations, we believe UK equity valuations are attractive relative to the rest of the world. Over the last few months, the valuation discount for UK equities has widened in terms of the price-to-earnings (P/E) ratio, providing an opportunity for active investors such as ourselves to initiate positions in high quality companies at discounted prices.

Looking forward, the UK Equity team remains cautiously optimistic that there are strong opportunities for investors in the UK equity space due to cheap relative valuations, and that headline risks are potentially being overplayed by the media.

What Are the Risks?

All investments involve risk, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Smaller and newer companies can be particularly sensitive to changing economic conditions. Their growth prospects are less certain than those of larger, more established companies, and they can be volatile. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

_________________________

1. Source: Financial Times, “UK inflation surges to 3.2% as food and transport costs rise,” 15 September 2021.

2. Source: Reuters, UK takeovers hit 14-year high in first seven months of 2021, 3 August 2021.