English

English 简体中文

简体中文

What is digital transformation?

Digital transformation is the process of using digital technologies to create new or modify existing business processes, products, services and customer experiences. It is not just about adopting new tools or platforms, but about fundamentally changing how a business operates and delivers value to its customers and stakeholders. We believe successful digital transformations can affect every aspect of a business, from strategy and culture to operations and innovation.

How do we research and invest in digital transformation?

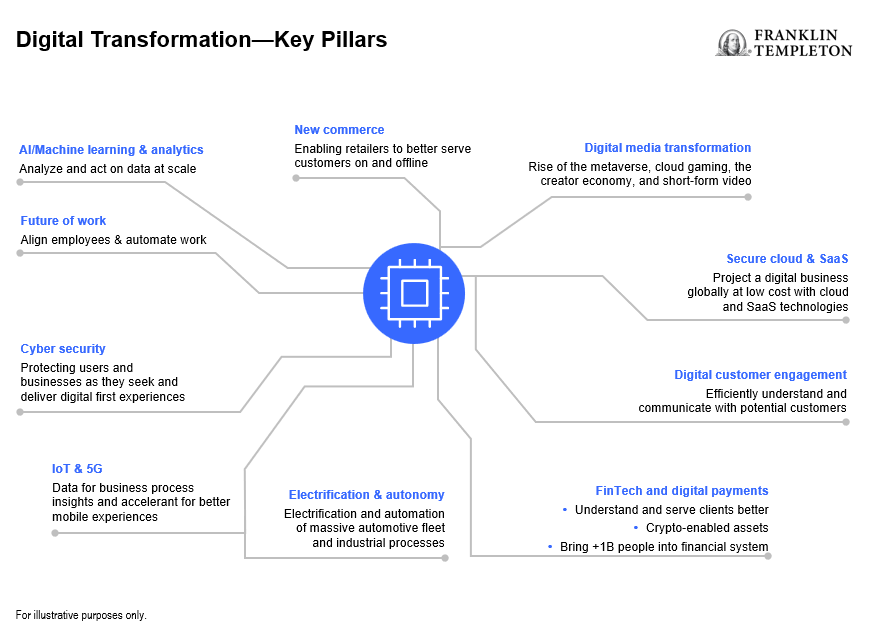

We are constantly evaluating how various themes are influencing and being influenced by new developments from both public and private companies. To gather insights, we have found significant benefits from leveraging a global network of analysts, portfolio managers, venture capitalists and industry experts. These perspectives have shaped our own views, which today focus on 10 sub-themes within the digital transformation landscape: artificial intelligence, new commerce, electrification and autonomy, digital media transformation, cloud computing, fintech, digital customer engagement, IoT/5G, cyber security and the future of work.

Why do we think generative artificial intelligence and cloud computing are misunderstood by investors?

One of the sub-themes that we are particularly excited about is generative artificial intelligence (AI), which is the ability of machines to create new and original content, such as images, text, music and videos, based on data and algorithms. We believe generative AI can disrupt and transform various industries and sectors, such as media, technology development, entertainment, education, and healthcare. For example, generative AI can be used to create realistic and personalized digital content, such as movies, games, books and art, that can cater to the diverse and evolving tastes and preferences of consumers. Generative AI can also be used to enhance and optimize the design and production of physical products, such as clothing, furniture, and cars, that can meet the specific and customized needs and demands of customers.

However, we think that many investors misunderstand generative AI. These investors tend to focus on the ethical and regulatory challenges and risks associated with it, such as privacy, security and intellectual property. While these risks are valid and must be monitored, we also believe they can be addressed and mitigated by the responsible and ethical use of generative AI and the development and adoption of appropriate standards and regulations. In our view, investors tend to underestimate the positive and beneficial impacts and opportunities that generative AI can bring to society—such as enhancing creativity, innovation, and productivity—as well as improving access, affordability, and quality of digital and physical products and services. Our work convinces us that this generative AI opportunity will be measured in trillions of dollars in the years ahead.

Another sub-theme that we are very bullish on is cloud computing, which is the delivery of computing services—such as servers, storage, databases, software and analytics—over the internet. We believe that cloud computing is the backbone and enabler of digital transformation, as it provides the scalability, flexibility, and efficiency for businesses to access and use digital technologies and solutions. Cloud computing also enables businesses to innovate and experiment with new products and services and improve their customer experience and engagement.

We also think that investors misunderstand cloud computing and generally view it as a commoditized and low-margin business with intense competition and price pressure. While we recognize and monitor these challenges, we also believe that they can be overcome and offset by the differentiation and value-addition of cloud services, such as security, reliability, and performance. It can be easy for investors to overlook the long-term and sustainable growth potential of cloud computing, as it is still in its initial stages of adoption and penetration, especially in emerging markets and industries. In addition, the recent post-COVID optimization cycle has caused investors to question the ultimate size of the market. We are not concerned, as our work convinces us that the cloud opportunity will be trillions of dollars in size one day and that the recent slowdown is cyclical—not secular.

Navigating public and private investing avenues

In today’s climate of rising interest rates, the investment landscape for digital transformation is evolving across public and private companies. Quality growth public companies offer liquidity, have strong balance sheets, and generate their own capital to fund their growth. These companies can also be sensitive to quickly evolving interest rates, which can create short-term volatility in returns. Private company investments can provide longer-term growth potential, but they also come with illiquidity risks and less short-term volatility in returns given limited repricing, even as rates rise. They also typically have weaker balance sheets and are not yet generating their own capital. We see a benefit to holding both asset classes in portfolios, as their differentiated liquidity and return profiles offer potential diversification benefits and, importantly, insights into prospects for future disruption which could alter the competitive landscape.

Conclusion

We believe that digital transformation is one of the most important and disruptive trends in the world today, and we are committed to researching and investing in the leading public and private companies that are enabling or benefiting from it. We are particularly excited about the sub-themes of generative AI and cloud computing, which we think are misunderstood by investors, and offer attractive and compelling opportunities for long-term value creation.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Active management does not ensure gains or protect against market declines.

Investment strategies which incorporate the identification of thematic investment opportunities, and their performance, may be negatively impacted if the investment manager does not correctly identify such opportunities or if the theme develops in an unexpected manner.

Focusing investments in [consumer discretionary-, health care-, technology-, information technology-] related industries, carries much greater risks of adverse developments and price movements in such industries than a strategy that invests in a wider variety of industries.

To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Digital assets are subject to risks relating to immature and rapidly developing technology, security vulnerabilities of this technology, (such as theft, loss, or destruction of cryptographic keys), conflicting intellectual property claims, credit risk of digital asset exchanges, regulatory uncertainty, high volatility in their value/price, unclear acceptance by users and global marketplaces, and manipulation or fraud. Portfolio managers, service providers to the portfolios and other market participants increasingly depend on complex information technology and communications systems to conduct business functions. These systems are subject to a number of different threats or risks that could adversely affect the portfolio and their investors, despite the efforts of the portfolio managers and service providers to adopt technologies, processes and practices intended to mitigate these risks and protect the security of their computer systems, software, networks and other technology assets, as well as the confidentiality, integrity and availability of information belonging to the portfolios and their investors.

To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.