The Federal Reserve’s (Fed) March policy meeting has generated very vocal reactions by commentators and market participants. This time I think the excitement has gone well beyond what the substance of the meeting warranted and tries to read way too much into the Fed’s new economic projections and into Chair Jerome Powell’s words, in my view. Financial markets’ reaction so far, I’m happy to say, has been slightly more muted than on previous occasions when Powell was perceived as dovish.

Let me say one thing up front: I do think this is a dovish Fed, and that Powell’s own preferences are on the dovish end of the monetary committee. But I also think this is a pragmatic Fed, which has already gotten burnt by high and stubborn inflation.

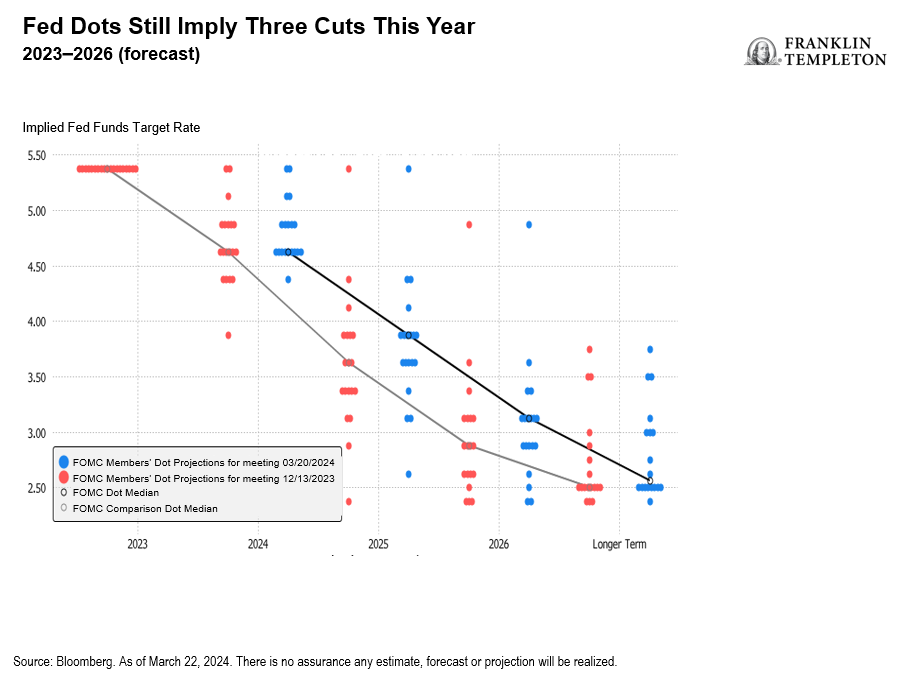

With rates expected to stay on hold, attention focused on the new economic projections. The prevailing narrative about the March meeting has emphasized the fact that the Fed’s new economic projections envision higher inflation and stronger growth, but the median rate forecast implicit in the dots still implies three rate cuts this year. Therefore, the argument goes, the Fed has given a strong signal that it is determined to cut rates and willing to tolerate higher inflation.

But this is one occasion where it’s important to look at the trees, not just the forest: Looking at the individual dots shows that, on net, five governors have reduced their projected number of cuts. Nine out of nineteen members now see two cuts or fewer versus ten who envision three or more (with only one expecting more than three). If just one more governor had lowered a dot, the median would have ticked down to only two rate cuts, and the narrative would have changed.

Next, let’s consider what Powell said during the press conference.

On financial conditions: This commentary was by far the most dovish signal. In the Q&A, Powell pointed to the tentative weakening in labor markets to argue that financial conditions were pushing in the right direction, helping the disinflation effort. This is rather a stretch: Financial conditions as measured by the Bloomberg index are currently as loose as when policy interest rates were at zero. The sustained rally in asset prices has been moving with full force against the Fed’s monetary tightening. Powell was obviously reluctant to utter words that might cause equity markets to retrace, but I think here he pushed the argument too far.

On inflation, Powell to me sounded fairly balanced and pragmatic—by his standards. He did say there are reasons to believe that the higher-than-expected inflation readings of January and February might be “bumps in the road,” partly influenced by seasonal factors. But he acknowledged that within the Federal Open Market Committee the readings certainly did not bolster anyone’s confidence that the disinflation goal is within reach, and that they validated the Fed’s decision to keep rate cuts on hold for longer. He noted that the Fed always expected the disinflation process to be bumpy; it did not get too excited when inflation readings were better than expected, and it’s not panicking after the latest readings—it wants more data to understand whether January and February were “bumps” or signs that inflation is getting entrenched above target.

On policy rates, he reiterated that the Fed sees the first rate cut as a “very consequential” step: The Fed knows there is a risk in waiting too long, but they also still see a risk of cutting too soon. Before they start cutting, they want to be confident that disinflation is sustainably on track, and the strong economy affords them the luxury to wait for more inflation data to come in.

All this sounds sensible. I also have some sympathy for a central bank that finds itself in a “damned if you do, damned if you don’t” situation with respect to the election calendar. With the presidential ballot looming in November, either a sharp downturn in growth or a resurgence in inflation would be highly consequential. And the closer we get to an election, the more likely that a rate cut will be read through a political lens.

I still believe that getting inflation all the way down to 2% will be harder and will take longer than Powell would like—and the Fed’s new projections confirm that some Governors are also getting somewhat more concerned that inflation might prove stubborn. The Fed’s estimate of the neutral policy rate, which inched up to 2.6%, remains well below my estimate of around 4%, but Powell at least acknowledged that rates are unlikely to move back to their post-pandemic lows. And the dots now show one fewer rate cut in 2025—three rate cuts, in line with my view.

So, overall, I think Powell handled the March press conference well, and much of the subsequent debate has been overblown. As I said, it is telling that the market’s reaction has been much more muted relative to previous occasions when Powell was perceived as dovish. But I also remain of the view that the last mile of disinflation will be harder and will take longer. As we get closer to June, where the market is pricing the first rate cut as most likely, this challenge will likely bring more volatility. Neither the data nor Powell’s press conference have changed my view that rate cuts will come only later, in the second half of the year.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Equity securities are subject to price fluctuation and possible loss of principal.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.