Financial markets have entered a period of head-spinning volatility. Exhibit one: the US stock market’s rollercoaster ride around the September inflation release. Exhibit two: the recent turmoil in UK financial markets.

High volatility and uncertainty create a challenging environment for investors. To develop a successful investment strategy in this environment, the first priority, in my view, should be to pin down the fundamentals. These suggest two observations: (i) to paraphrase Tolstoy, while all stable markets were alike, every troubled market or country is troubled in its own way; (ii) nonetheless, common structural forces are driving a fundamental shift in the investment environment.

Let’s start with inflation. Consumer inflation remains at record highs across major developed economies: in September it ran at 8.2% year-over-year (Y/Y) in the United States, 10% Y/Y in the eurozone and 9.9% Y/Y in the United Kingdom (in August).1 These numbers represent inflation rates not seen in half a century. This common trend begs for a common cause; indeed, the energy shock and supply chain disruptions have played an important global role. Still, the nature of inflation pressures differs substantially between the United States and Europe.

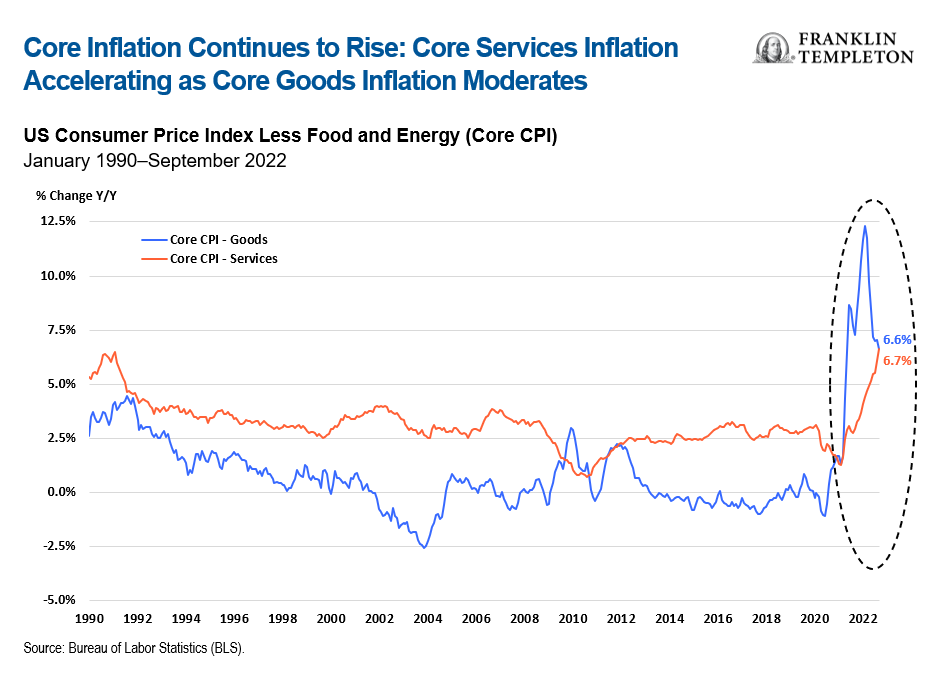

The United States experienced a massive fiscal expansion during the pandemic, and fiscal stimulus continues to flow in the form of subsidies and debt forgiveness programs. Excess demand therefore is a major inflation driver; in September, even as lower energy prices brought headline inflation down, core inflation (excluding food and energy) accelerated above expectations to 6.6%, the highest in 40 years. Core inflation has averaged 6.2% so far this year and shows no signs of coming down—to the contrary, it’s rising. The last time it sat below 2% was in March last year. Meanwhile, aggregate demand remains resilient and the labor market remains as tight as it’s ever been. Excess demand is an important inflation driver—as the Fed has belatedly recognized. So, the Fed can’t stop and won’t stop hiking rates anytime soon—I expect that the federal funds rate could easily go above 5%.

The eurozone, given its high dependence on Russian gas, has been hit much harder by the energy shock, which is the primary driver of inflation and poses an important risk to growth. The European Central Bank (ECB) does need to tighten policy, but it does not need to be as aggressive as the Fed. Arguably, the United Kingdom suffers the worst of both worlds: an energy price shock comparable to the eurozone, exacerbated by wage pressures. With a more vulnerable pension system (a heavier defined-benefit component drove more extreme yield-seeking) and housing market (greater proportion of variable rate mortgages), the United Kingdom faces greater risks on both inflation and growth.

These differences determine a striking divergence in the policy stance of major central banks—from the Fed’s very hawkish turn to the Bank of Japan’s wait-and-see attitude—which in turn feeds extra volatility in currency markets.

But behind these different challenges also lies another common factor: excessively loose global monetary policies for an excessive period of time. Supply shocks were the trigger, but loose monetary conditions have allowed inflation pressures to become broad-based.

The other important consideration for investors is that we are seeing economic and financial fundamentals reassert themselves. A world of zero interest rates, endless quantitative easing and ever-rising debt was patently unsustainable. The fantasy that it could last forever has been exposed for being just that—a fantasy. The proponents of Modern Monetary Theory have gone quiet.

The transition back to reality was always going to be hard. Hence the volatility, as yield-seeking strategies built for a “secular stagnation” environment need to be unwound. As fundamentals reassert themselves, investment strategies must center on a sober assessment of the likely policy outlook and focus more than ever on fundamental analysis. I expect inflation to remain higher for longer, and that the Fed will therefore need to maintain a tighter policy stance for an extended period of time. My most-likely scenario envisions a shallow recession accompanying a slow disinflation. I do not believe we will go back to an extremely low interest rates world—not for a long time.

This implies a very important shift in the fixed income investment environment. Higher yields will bring new income-generating opportunities and significant shifts in risk-return assessments. I believe yields are likely to rise further, but as we get closer to the peak of the cycle, investment grade bonds and US Treasuries stand to benefit first. Looking across riskier asset classes like high yield and emerging markets, over the next few quarters we believe selective security selection will allow investors to start taking advantage of yields which in many cases are now running above 10%.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at September 30, 2022, and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

The information in this document is provided by K2 Advisors. K2 Advisors is a wholly owned subsidiary of K2 Advisors Holdings, LLC, which is a majority-owned subsidiary of Franklin Templeton Institutional, LLC, which, in turn, is a wholly owned subsidiary of Franklin Resources, Inc. (NYSE: BEN). K2 operates as an investment group of Franklin Templeton Alternative Strategies, a division of Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

___________

1. Sources: Bureau of Labor Statistics (BLS), Eurostat, UK Office for National Statistics.