English

English 简体中文

简体中文

This post is also available in: Chinese (Simplified)

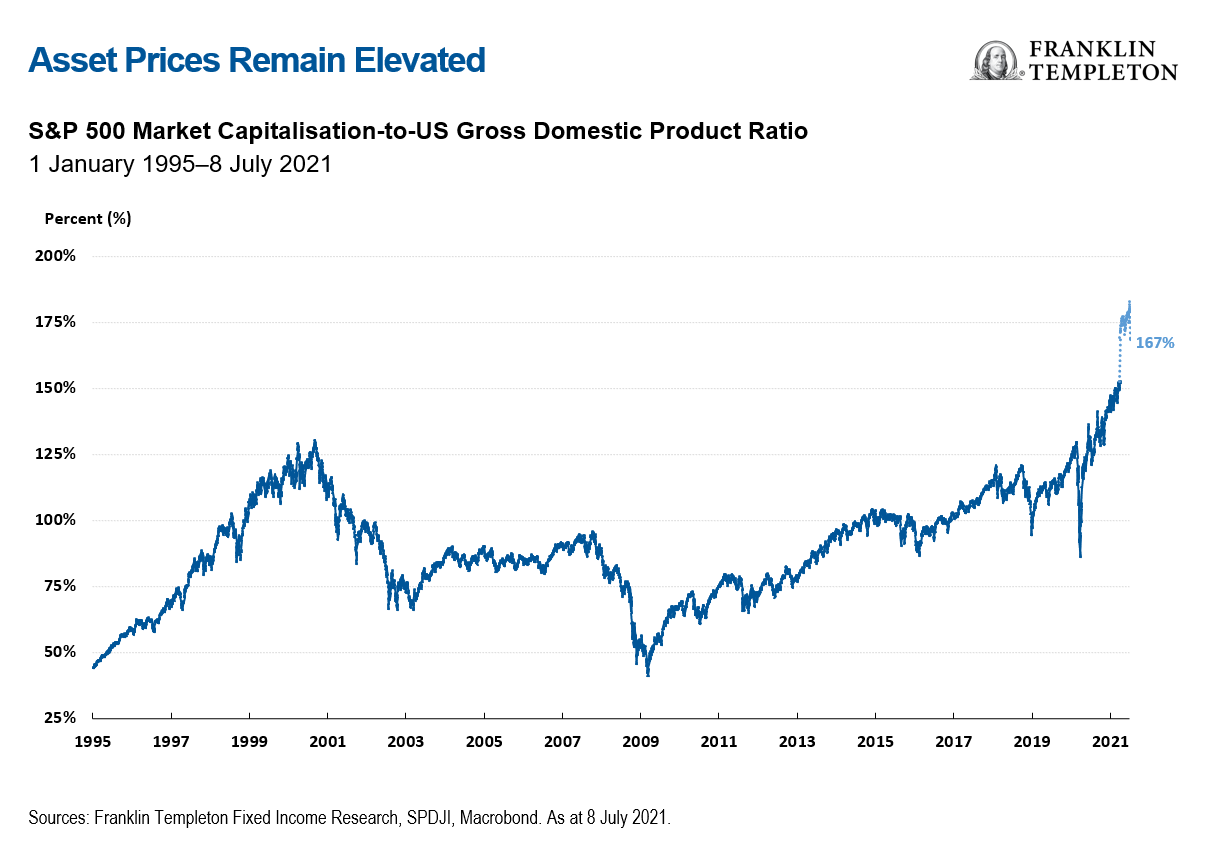

US Treasuries have rallied sharply over recent weeks with yields dropping by about 30 basis points,1 and analysts are scrambling with differing explanations. However, the growth outlook has not actually changed. I see three possible scenarios, which I discuss below. But regardless of which scenario plays out, something in the current constellation of asset prices does not add up. Over the next six months, most likely, we will find out what does.

The unusual degree of uncertainty in the current macro environment allows for a wide variety of views on how things will play out. I don’t have a crystal ball, but I would not bet on the dream constellation of strong policy-supported economic growth, low and stable inflation, loose monetary policy and ever-rising asset prices that markets seem to hope for. Something has to give. I see three main possibilities.

A first possible scenario sends us back to secular stagnation: Growth fizzles out by the end of the year. Maybe political disagreements will close the door to additional US fiscal stimulus. Or a resurgence of COVID-19 cases could trigger another round of restrictions (I could see this happening in Europe after the summer tourist season). After a strong brief rebound in growth and a sharp short-lived jump in inflation, we quickly get back to a long run of slow growth, low inflation and low interest rates. This by the way is the view implicit in the official growth forecasts of the US administration (as embodied in the budget assumptions, and consistent with those of the Congressional Budget Office).

What doesn’t add up here? Asset prices. If economic growth fizzles out, the stock market needs to reprice for modest earnings expectations. And if slow growth is as good as it gets, the Federal Reserve (Fed) will need to accept that loose monetary policy cannot boost activity and will have to unwind its massive monetary easing—which again should translate in lower asset prices. Or, the Fed could decide to maintain a very easy monetary stance anyway—but that sooner or later will result in increasing distortions in markets, leading to financial instability, or inflation, or both—again bad news for markets.

A second scenario envisions a productivity renaissance. The policy-fuelled demand surge generates a proportionate supply response: workers come back into the labour force and companies quickly ratchet up production, easing bottlenecks. Meanwhile, both governments and companies redouble their research and development efforts, accelerating innovation and infrastructure and generating a rapid pickup in the pace of productivity growth. The supply response and productivity acceleration enable fast economic growth and healthier wage gains.

What doesn’t add up here? Interest rates. The current ultra-loose monetary stance will appear unnecessary even sooner. The Fed will be under heavier pressure to bring forward its policy tightening, especially if inflation remains elevated. In principle, faster productivity growth should help cap inflation. In practice, it’s likely to take longer for greater investment to translate into faster productivity growth. Meanwhile, we’ll have an economy at full employment and firing on all cylinders; and stronger productivity growth implies a higher natural rate of interest, the infamous “r-star.” Markets will have to start pricing in higher rates. Stock markets will be supported by the tailwind of productivity on earnings, corporate bonds will benefit from a healthier profitability outlook, but long-duration “safe-haven” assets will look markedly less attractive.

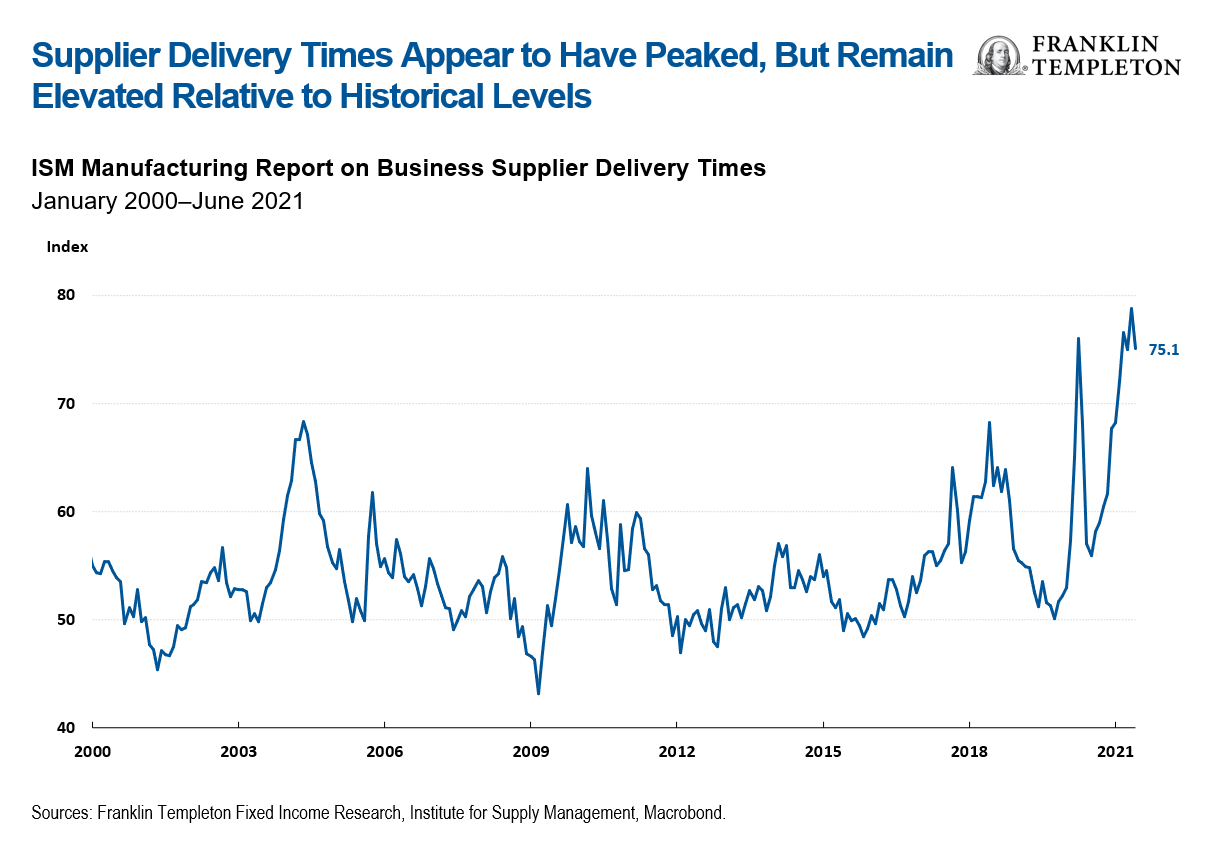

The third scenario sees a classic overheating. Demand continues to recover at a fast pace as post-pandemic life gets back to (almost) normal: supply struggles to catch up; industries need more time to work through supply chain disruptions; labour force participation remains below pre-COVID levels; past underinvestment in raw materials extraction keeps their costs elevated. In short, an extension of what the data are telling us now.

What doesn’t add up here? Inflation. In this classic overheating scenario, loose monetary and fiscal policies feed sustained inflation. Not (necessarily) a return to the 1970s, but a persistent 3%-5% that gets entrenched into wage and price setting seems quite realistic. This will put the Fed in a bind: the longer it waits to reverse course, the harsher the tightening when it finally comes. Market rates will move up faster than the Fed, punishing duration exposure in fixed income. Stock markets should be initially well supported, but then increasingly nervous as the Fed gets ready to tighten.

I don’t have a crystal ball. I have my most likely scenario, but you can pick your own. At the moment, the economic data are mostly consistent with the overheating scenario, whereas market reactions suggest something in between the secular stagnation (with the recent decline in 10-year US Treasury yields) and the dream scenario (with stock indices still at record high). Something has to give. Place your bets, and get ready for more volatility as we find out what does.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this presentation has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Investments in lower-rated bonds include higher risk of default and loss of principal. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

______________________

1. One basis point is equal to 0.01%.